This couldn’t be more wrong. Even if you feel like you’re a late bloomer when it comes to investing, you’re probably only a few years away from hitting FI—if you make the right decisions. This is the quandary that today’s guest, Nicole, finds herself in. Nicole has recently gone through a divorce and lost a good chunk of her net worth thanks to it. But, she’s poised on investing in real estate so she can hit financial independence sooner rather than later.

Mindy:

Welcome to the BiggerPockets Money Podcast Show Number 282, Finance Friday Edition, where we interview Nicole and talk about investing in real estate even if you’re getting started a little bit late.

Nicole:

That’s when I thought about that goal that was kind of for me to live comfortably and be able to take vacations and do whatever I want to do with my daughter. That 4,000 would be comfortable for me. Even though I’m living below that now, it’s for a reason, but I don’t want to continue to live that low.

Mindy:

Hello, hello, hello. My name is Mindy Jensen and with me as always is my solves the Wordle on his first try co-host, Scott Trench.

Scott:

I don’t know about that Mindy, but I did get … I’d only done one Wordle and the word was moist last week. So I know that’s favorite word of many listeners.

Mindy:

That’s such a gross word.

Scott:

Wasn’t that your first word that you guessed in Wordle each time?

Mindy:

That used to be my first start word, and then I stopped and then it was the word and I was very upset. So now I have to find a new first word and someday I will get it on the first try. But I don’t right now. Anyway, Scott and I are here to make financial independence less scary. Less just for somebody else. To introduce you to every money story, because we truly believe financial freedom is attainable for everyone, no matter when or where you’re starting.

Scott:

That’s right. Whether you want to retire early and travel the world, going to make big time investments in assets like real estate, start your own business or start over after a divorce with a fresh financial start, we’ll help you reach your financial goals and get money out of the way so you can launch yourself towards those dreams.

Mindy:

Scott, I love today’s guest because she is not financially perfect but she’s doing a lot of things right. So we give her several things to look at, very … There’s a couple of research opportunities in there as well. And I’m excited for her trajectory. I think she has a lot of potential.

Scott:

You say she’s not financially perfect, but she’s pretty close, in my opinion, relative to where her current financial position is. She’s got complete control over her budget. She ends up a little over a median income, I would say around a median income, and doesn’t have much in the way of assets. But I think is really setting a financial foundation for herself that’s likely to be really strong. I think it’s just a great perspective and someone to learn from. I think we’re going to be all admiring her progress within the next three to five years, based on the trajectory that she’s set up for herself, and we heard about today.

Mindy:

I agree. And when I said she’s not financially perfect, I meant there’s things that we can suggest and there’s room for her to explore. And we were able to give her research opportunities, which I love. Okay, before we bring in Nicole, I have to tell you that the contents of this podcast are informational in nature and are not legal or tax advice. And neither Scott, nor I, nor BiggerPockets are engaged in the provision of legal tax or any other advice. You should seek your own advice from professional advisors, including lawyers and accountants regarding the legal tax and financial implications of any financial decision you contemplate.

Nicole is a recently divorced single mom looking to get started investing in real estate. She feels like she’s getting a little bit later start in life. But at age 35, I think she’s doing really well. Her monthly spending is tight. Her debts are low and getting even lower. And she’s got a military pension and a VA loan to help her on her way. Nicole, welcome to the BiggerPockets Money Podcast.

Nicole:

Thank you for having me.

Scott:

Nicole, before we get into your numbers, could we hear a little bit about your backstory and what’s happened over the past 10, 15 years to set us up for this conversation we’re going to have today?

Nicole:

My money journey, growing up, we had very little but we made ends meet. But I wasn’t really educated on finances and saving for the future. So I really had a lack of knowledge with that. I joined the military at 17 years old. After I graduated high school, I joined the army reserves. I’ve been in for 18 years now. Went to college, did not incur any college debt. Worked two jobs to pay for everything, and came out of that degree with zero debt. I had a full-time job, started working, but wasn’t really saving. Didn’t have a good understanding of saving for the future. I could have started a lot earlier.

About seven years ago, eight years ago now, I started my current W2 job and started saving for my future with their 401(k) program. So I was saving 10% of my income with that 401(k). I’ve been divorced for about two years now. Through that divorce, I lost quite a bit of money, $30,000 out of my 401(k), $20,000 in marital debt that I did not know about that I had to pay off. So that set me back a little bit. But through that divorce, I’ve regained that financial freedom. We were living off of my income, family of four. So it was very strapping and wasn’t able to really save as much as I wanted to. I just got back on my feet, was able to buy a home. I still have a marital home that I’m trying to get rid of. But was able to buy a home for my daughter and I, and on my way to financial freedom, hopefully.

Scott:

Nicole, would it be fair to say that following the divorce here, that’s when your money story really begins or the next chapter begins?

Nicole:

Yes, definitely.

Scott:

What’s happened since then from a financial perspective? Have you started learning more? Have you been taking different actions or changing up how you invest or save? What’s been the trajectory, if any, has changed?

Nicole:

I ended up living with my mom for about a year to get back on my feet. I was able to save up enough money to buy a home for my daughter and myself, and saved up that money for closing. I had to pay a little more over the appraisal rate. I started just building up my emergency fund. And I started listening to BiggerPockets about eight months ago. And it has just opened up a whole new world for me. I had always had a budget and lived frugally. But now I read Scott’s book about two months ago and I’ve really started on that plan and process to move forward, save as much as I can, lower my spending, and on that right track.

Scott:

Awesome. So let’s go through your numbers now with that back … Thank you for sharing that backstory. And let’s start off with the income statement. How much are you bringing in and where are you spending it?

Nicole:

All right. It’s about 4,000 for my civilian job and then 500 a month for my army reserve position. My monthly expenses, my mortgage is 895. Electric/water, 200, 113 for cell phone, 500 estimated for groceries. Current car payment is 181, gas is 120 a month, auto insurance is 99, gym membership, 30, miscellaneous entertainment, 150, internet, 54. And then I do have allotted 275 for credit card payment. I have $3,300 at 0% interest so I’ll pay that off within the year. That is included in my monthly budget. I have about $1,900 left over after my monthly expenses.

Scott:

Awesome. That’s a really tight budget. So you’re doing a phenomenal job on that front, at least my opinion on that. Where’s the money going? What are your assets, liabilities, debts?

Nicole:

Currently, I have two mortgages. The mortgage I live in, the house I live in right now, I pay. My previous mortgage that is still under my VA loan. My ex-husband assumed the mortgage so it’s a wash not paying for that. That will be refinanced and out of my name, off my debt to income in the next 90 days. That’s 188,000. The home I currently live in is 155. I have 3,300 in credit card debt. So that is my liabilities right now, my debts.

Scott:

Great. Do you have any investments in cash savings?

Nicole:

I have 12,000 in cash and 80,000 in my 401(k).

Scott:

Great. Any other assets or things that we should be aware of?

Nicole:

The one thing, I do have my military pension. Like I said, I’ve done 18 years. At 20 years, I’ll get my 20-year letter and I will be guaranteed that military pension. So current value is 325,000. And then when I complete my 20 years, it’s estimated at 387,000 and that’s in current value.

Scott:

Great. And how long to the 20 years?

Nicole:

October of 2024.

Scott:

You’re two years away from realizing this $354,000 asset.

Nicole:

I cannot collect that until age 58.

Scott:

Okay, great. Well, awesome. What is the best way we can help you today based on what you’ve told us?

Nicole:

I’ve made some adjustments to how I am in investing, I guess, in saving. I have a couple questions with that. And then also I would like to really start investing in real estate. Do I use my VA loan? Do I go conventional? What is your recommendation? I can start with the how I’ve changed my investing a little bit.

Scott:

Well, let’s zoom out a little bit. What’s the goal?

Nicole:

Short term, one year, I want to save at least $20,000 for this year. Starting with your steps and $20,000 to $24,000. Three years, I would like to have $2,000 in passive income. And then in five years, I would like to have $4,000 in monthly passive income.

Scott:

That’s fantastic. Thank you for being so clear about what it is you’re looking for. I love it. I think that these goals make a lot of sense. They’re ambitious, but definitely achievable. This will be fun. So that sounds like the first question is to save 20K, which you already have 12,000. You’re not even including the 275 you’re paying towards credit card debt, which I count as savings towards that savings number. And you’re accumulating 1,900 a month in cash based on what you told us from the budget. So you should absolutely crush that goal over the next 12 months. That would be 22,800. In additional savings, in addition to paying off your credit card, in addition to the 12,000 in cash over the next 12 months. Is that right?

Nicole:

Yes.

Scott:

Awesome. I love that. It sounds like the next question really then is the real estate side of things. You’re talking about using a VA loan. My belief is that VA loan will require you to move into the property so that implies you thinking about house hacking. Is that right?

Nicole:

Yes. To reference your book, currently I have two VA loans, the mortgage I’m living in now and then my previous home, so it’s tied up my eligibility. Once that other home is refinanced out of my name, I will gain that eligibility and then the eligibility I have currently in this home. So my question is this home that I have now, if I were … I’ve lived it in a year and after a year, you’re able to … You can rent it out. So I would still have VA eligibility left to purchase something else if I wanted to within a certain number based on how much eligibility I have left. Or I can keep it or I can sell it and purchase possibly a duplex house to make additional passive income. Because this would only produce probably $200.

Scott:

Yes. Well, I think that’s the first really smart question is what do you do with the existing home? And you have to run the numbers and analyze. And I think you say, “If I was starting over, would I buy this place as a rental property today?” What’s the answer to that question in your mind?

Nicole:

I think I bought it for too high to get enough passive income out of it.

Scott:

How long have you lived in the property?

Nicole:

A year.

Scott:

How many months?

Nicole:

April, it’ll be a year. So it hasn’t been a year quite yet.

Scott:

Okay. I love the way we’re thinking about this. The reason I’m asking that is because if you live in a place for more than two years, you can sell it and you do not have to pay capital gains taxes up to a certain threshold on that. So that’d be April of 2023. That might be too long in your position relative to the … Well, how much do you think the gain would be? What’d you buy it for? And what would you be able to sell it for in April?

Nicole:

There’s probably only $15,000 worth of equity in it.

Scott:

Okay. So to me, that’s too small of an amount to necessarily disrupt your whole strategy in order to realize the $3,000, $4,000 in tax savings you might have from the sale of that home. I like the instinct to potentially sell the property, but let’s do a couple more questions on it before we do that. How much would it rent for from a short term perspective? Would it make a good short term rental?

Nicole:

The area, I really don’t see that it would be a good short term rental.

Mindy:

What about a medium term rental? Do you live near a hospital? Do you live near a large corporate facility where somebody would need to be staying longer term? Do you live near an oil refinery? Is it Louisiana that does the oil refinery stuff? He’s got a bunch of properties that he rents to the people that are working in the oil refineries because it … The contractor’s down there.

Nicole:

Unfortunately, I’m in a location that is there’s tons of rentals and there’s really not a market for that. I have explored those options and there’s really not a market. So I’m leaning towards possibly just need to get out of it.

Mindy:

Okay. You would be, if you live in there for more than a year, but less than two years, you’re looking at short term capital gains, and that is taxed at approximately 15% depending on your financial situation. I think based on your financial situation, it would be 15%. So it’s 15% of the gain, which is going to be $2,200. Not an amazing amount, not a horrible amount.

Nicole:

What if I rented it for a year and then sold …

Mindy:

Same thing.

Scott:

You got to live in it for two of the last five years.

Nicole:

Your primary residence.

Mindy:

Unless you wanted a house packet and get a roommate for a year, then it’s still your primary residence. That could be an option. I don’t know if you have enough bedrooms to do that. That could be an option while you’re looking for your next property. But like Scott said, the VA loan is an owner occupant loan. You must live in there for the first year. So you can use your VA loan up to four units. It doesn’t just have to be a duplex.

Nicole:

Four doors.

Scott:

Let’s go through absent the financing for a second. What would a good house hack or investment property look like in your area or the areas you’re considering moving to?

Nicole:

There’s not an abundance of duplexes, triplex, complex in Central Florida. So it would really be a find if I did come across one, but it probably … Price point, is that what asking or …

Scott:

What’s a good deal look like to you?

Nicole:

There’s not even that many for research-wise, but I would probably be looking at 250 for a duplex, at least, would be a decent deal.

Scott:

What are the numbers? It doesn’t have to be duplex, right? There could be a single family where you live in one part of the house and rent out the other part or whatever. This is going to be turned into the first homework assignment I would have for you is I think you need to get clear on what a good move looks like. So you have three to six months to really prep yourself for, “Okay. What am I looking for here?” And if you’re going to follow the stuff and set for life, and thank you for mentioning the book a few times here, then you’d want it to make sense as a rental after you moved out. What’s the place that would produce the most income while you live in there and then be a great long term rental for you as soon as you leave the property?

Nicole:

Definitely would have to be a duplex or a triplex. Would definitely have to be that. Something else I was considering all over the place and what to do is possibly partnering with somebody for finding a short term rental and continuing to live in my current home. Because the mortgage isn’t too high.

Scott:

Well, let’s think about the financing here next. Within a year, you’re going to accumulate a total of about $30,000 to $32,000 in cash. And you could use 5% of that, if you bought a $250,000 property, for example, like you just mentioned, 5% down would be $12,500. So you have $20,000 left over, which I think is a really solid position to be buying a property from. If you have good credit, you have $20,000 in cash left over, you’re buying a house hack, that’s a really strong position for that. And that allows you to keep your VA loan. Why that might be interesting for you is because $250,000 is probably well within your purchasing power with your current income and situation. And if you were to get a tenant to rent from you, for example, for a year for half the duplex, you’ll have that rental history on your tax return.

And when you go to buy the next property, you might find, “Hey, I’m going to buy this quadplex for $700,000,” making that up. Well now, because you’ve got the income from the rental and you got a history there. Not only will you get to add that to your income and your salary and your military income, you’ll also be able to add the rental income and the projected future income of the property that you’re considering buying. So your VA loan may balloon in purchasing power on the second purchase if you were able to, for example, swing it to put down the 5% using an alternative form of financing. I’ve heard of military folks, for example, putting down the 5% when they’re stationed in Florida and using the VA loan for the San Diego purchase, for example.

Nicole:

That definitely makes sense. I was questioning that. Do I use it or do I save it? I definitely think that’s great advice as far as possibly the first purchase, saving it, not using it, and using the money that I saved to put that 5% down.

Scott:

I think you can’t make the decision about the … I like the instinct to house hack. It’s a great starting point for someone in your situation making around a median income, starting with relatively few liquid assets and you don’t have hundreds of thousands dollars to … You’re doing great, but you don’t have hundreds of thousands dollars to invest. And that’s just a really powerful tool in the kit. It’s likely to be a big winner for you. Even if it doesn’t produce cash flow or let you live for free, it’ll likely substantially reduce your month to month living expenses. So I love that. What does the short term rental look like?

Nicole:

I was possibly thinking of something local, beach-wise, but possibly partnering with somebody. Because short term rentals here are not $250,000.

Scott:

What’s local?

Nicole:

Beaches, New Smyrna east coast or west coast on Central Florida. So either coast.

Scott:

How far are these from where you live and work?

Nicole:

New Smyrna Beach is 30 minutes. The other coast is about an hour-and-a-half.

Scott:

Would you consider living in one of those places? For example, is there a duplex or a condo with one of the doors that locks off the other unit or whatever with that for a year? Would that be an option available?

Nicole:

I was looking at one of the beaches that’s close or 30 minutes away. They do have more duplexes there, and possibly being able to use one half as a short term rental and then live in the other half. So it would be house hack times two with the short term rental.

Scott:

Would you be required to commute every day?

Nicole:

I work remote. The only limitation would be my daughter and her school zone, which I could still commute with that. It would just add extra transit time for myself. But it would definitely, profit-wise, would be worth it.

Mindy:

I’m looking on realtor.com at some of these New Smyrna Beach houses. I like the idea of a duplex on the beach where you’re living in one portion of it and renting out the other portion short term. You can do the turnover so you are not paying somebody to clean. That is the biggest pain point in short term rentals is finding somebody reliable to clean the property on your schedule. There’s ways to do this, especially when you’re doing it yourself, there’s ways to do this where you just literally bring everything back to your house and take brand new over there, have two sets of everything so that the turnover is a lot easier. Now the schooling for your daughter, is she in a special school or could she go to … Could she just transfer to the school in New Smyrna Beach? I mean, she’s pretty young. I’m assuming she’s only in the first couple of years of school.

Nicole:

She’s in kindergarten. It’s a little bit difficult. Her father lives in that school zone and that’s what we’re going off of right now. It is something that could possibly work moving her, but I would probably keep her in her current school. But the drive wouldn’t be out of the question.

Scott:

I think, if I’m looking at this now that we’re a couple minutes in the conversation, I think the biggest challenge for you is you’ve got a really strong financial base. You got really clear goals here. And real estate’s your tool that you’re likely going to use. Your market seems, from my seat, to be one that is affordable and within your reach to buy properties in, you’ve got the VA loan, all this kind of stuff. I think what I would advise you to do at the highest level is I think you need to pay what I call the entry price into real estate investing, which I think is in about 250 hours, maybe more, of just listening to podcasts, reading books, analyzing deals.

I think you’re still exploring some of these concepts at a high level. And I think you need to get clear on what good looks like and you’ve got at least 90 days before you’re really able to make the decision. Or if I were in your shoes, I’d feel comfortable buying property until that mortgage is off of my name. I think that would be a really good thing is I’m going to walk away from … Today’s February 8th when we’re recording this. I’m going to walk away from end of April and I’m going to be super confident. I know what a good deal looks like. I can articulate it in crystal clear detail about what I’m going to do.

One of several options or one particular strategy, here’s a duplex, it’s $200,000. It was built in 1950. It’s two bed, one bath on each side. Or three bed, two bath on each side. The square footage is this. It’s got a garage, it’s got a yard for the dog, whatever it is that you want to, that you’re looking for, cash flows like this. And here’s what’s going to do for me when I move in, here’s what’s going to do when I move out. There are five to 10 of them that have sold in the last 90 days or that I’ve watched sell over those last 90 days. So I know that they’re likely to come on the market.

And here are the Airbnbs in New Smyrna Beach. They’re within my price point from a VA loan because I’m qualified there. And here’s what they would produce from income. That I have to commute 180 days a year to the school zone for that or whatever it is. I think that’s what I would love for you to be able to articulate something to that effect very confidently by end of April. And I think that’s a very achievable goal over the next couple of months, in my opinion, for you.

Nicole:

Definitely. I’ve just struggled with that. And finding what I want and what looks good. So that definitely helps me. Thank you.

Scott:

Since we already plugged my book, maybe this will be the show of plugs here. Maybe we could send you your pick of 10 BiggerPockets books. Any ones that look interesting to you, we’ll send your way in your preferred format. And I think we will also give you a pro membership. so you can use the calculators to analyze as many deals as you’d like in there to help with that search. But I think it’s a self education slog to …

Nicole:

I’ve definitely tried to continuously listen and educate myself. Sometimes it can be overwhelming. Like Mindy was saying, your position is different than everybody else’s. And when you’re listening to someone that is younger and in a better position, it’s sometimes discouraging but I feel like I’m on the right track.

Mindy:

You have a great track. That is the part that I think we have … We don’t spend enough time on this show saying you’re doing great. You are 35 and you don’t have a net worth of $7 million, but you also don’t have a negative net worth. You don’t have $400,000 in student loan debt or $300,000 in credit card debt because you went nuts with the credit card every day for seven years. You’re doing really well. Your expenses are super tight. Could you cut things? Sure. Let’s put you on beans and rice every single day for the next month-and-a-half. Let’s take away your cell phone and take away entertainment and take away your gym membership. We can get your $2,600 spend down to $1,500. We can really tighten that belt and make your life totally miserable or we can continue on a path where you are having a good life and saving and you’re still doing really well. Does your budget feel tight?

Nicole:

No, I think it feels comfortable. Like you said, I could definitely tighten it up.

Mindy:

You could also definitely loosen it. You have $1,900 every month at the end. Go on a vacation every single week or buy a house once a year.

Nicole:

There you go.

Mindy:

I think that you should connect with a real estate agent. I’ve got a note here to reach out to you after we’re done recording to get a list of books and to connect you up with the pro membership. Thank you, Scott, CEO of BiggerPockets for offering that. That’s very generous of you.

Scott:

This is who they’re for, right, is you. You’re getting some information together. You’ve got a good idea of how things look, but you need to push through to that, “What does good look like so that I can actually feel confident to make that?” You need to do that over the next … You can’t take action for the next 90 days so that says time to study up. Probably, in addition to that analysis and that education, it’s probably a good time to meet a couple of lenders and agents as well and pick their brand, and local investors. If there’s a local investor meet up or anything like that, those would be really good things to start paying attention to and learning about in your area.

Take everything with a grain salt. See if you can pick out who you think knows what they’re talking about and who you think is maybe a little too aggressive or doesn’t really know what they’re doing. Once you get to that point where you feel like you actually can make that distinction, that’s when you know you’re ready from an investment perspective, to make that next purchase and make it really good decision.

Mindy:

I’m going to go one further and say, if you are a New Smyrna agent who has information about the area, please reach out to me, [email protected] and I will connect you with Nicole. I think Seth Jones is a mortgage … I know he’s a mortgage broker in Florida. I think he’s all of Florida. So I will introduce you to Seth after the show as well.

Scott:

And we have no financial affiliation with Seth Jones or any of these other folks, right?

Mindy:

Correct. No, we don’t have any financial … I’m just a matchmaker …

Scott:

Members of the community.

Mindy:

… to members of the community. I love to connect people. It doesn’t do me any good to just hold Seth Jones to myself. He’s the not going to write me a mortgage, because I don’t invest in Florida right now. But just talk to an agent and see what’s out there. There are zero quadplexes in all of New Smyrna Beach. Okay, that’s good to know. Or there are 17,000 or they’re building new ones. I don’t know anything about New Smyrna Beach. I don’t even know where it is on the map. I’m sorry. I don’t know what coast it’s on either.

But it doesn’t matter because I’m not the one that can help you with this. I can just connect you to somebody who can. So find what’s there. I mean, if you’re looking for a duplex and there’s only two in all of the city, that’s a really great indication that we need to change our focus. Could you find a really large house and turn it into a duplex? Is that something that would be easy to do? Or maybe there is a large house that’s already a duplex that isn’t official and you go through that channel?

Scott:

I don’t like the large rehab project for her at this point with that. I think that’s a big thing, like, “It’s great. You put in $30,000, $50,000 and turn it into a duplex.” Well, that’s just not reasonable relative to Nicole’s position because she doesn’t have all that cash. I like the single for the first play here. And then after two, three years, do some of the work yourself, get good with that and then take on the bigger projects incrementally with each of the next two or three projects.

Mindy:

I sometimes get ahead of myself. I’m like, “Just do it yourself.” Not everybody’s been doing it themselves for that.

Scott:

That was a big worry for me, I remember because I was like, “I have $12,000 and no skills.” I don’t want to do that on this particular project.

Nicole:

I do want to invest in real estate. I do know that. And it is a little discouraging knowing that I don’t have an overabundance of liquid cash. So it is discouraging at times, but it can be done and working towards that.

Scott:

But that’s where you can look for the work that would be reasonable for you to do yourself like kitchen … When I bought my first duplex in a very similar financial position to what you’ve got here, my evenings were spent staining the kitchen cabinets, which came unfinished. And painting and installing blinds and doing those types of things. There was a plumbing project that I did have to spend $8,000 on and that was it, and I knew that going in. That level of work might be very reasonable for you and might be able to get you a good deal.

Nicole:

I’m definitely not above doing any of that work and do have a little bit of background in that. My dad used to flip houses when I was younger. So free work, free labor.

Mindy:

Paint can transform a house for $35 a gallon. It is amazing what you can do with a gallon of white paint.

Scott:

I feel like your instincts are … I’m completely aligned with your instincts and it sounds like Mindy is as well here. House hacking is a great next option for you. Your foundation is perfectly set up for that. And real estate is you’re perfect fairway for someone who might benefit from real estate investing. You’re willing to do the work yourself. You’re willing to learn about it. You’ve got the financing options, you’ve got a good job with all this. You’ve got a high savings rate. You want the passive income in a reasonably fast period of time, so I love that. What else can we help you with today from a strategic ..

Nicole:

So recently, I cut my contributions to the [inaudible 00:36:46] which is 4% at my work so that I can save as much as possible. And I switched that over to a Roth rather than the 401(k). Does that feel like that was a good move? Should I continue with that?

Scott:

If the goal is $20,000 in income in a year and $2,000 in passive in three years and $4,000 in passive in five years, then absolutely, that’s a great move. That’ll be really hard to do inside of your 401(k) in my opinion. I like the move to the Roth. Take the free money, put it in the Roth and then put the rest towards the fund to go after the real estate investments. I think that makes sense to me.

Mindy:

I’m wondering what your W2 job is. And are there any opportunities for advancement within your company? Are there any opportunities for advancement by, advancement meaning an increase in salary, by finding a new job if you’ve been there for a while? And are there any opportunities for generating any additional income as a side project, either through your W2 or through … maybe your fluent in, I don’t know, Swahili and you want to give Swahili lessons and that’s something that is going to be a lucrative side hustle. I wouldn’t necessarily suggest doing something that’s pretty low value like DoorDash that doesn’t really pay a lot. That’s a lot of initial cash outlay in the form of wear and tear on your car and gas into your car, and then you’re not making a whole lot of money on that. Are there any side hustle opportunities for you?

Nicole:

Over the past two years, you know, since my divorce, I’ve really tried to focus on getting my life back together and focusing on my daughter. So currently, I don’t manage anyone. There are opportunities I could go back and manage people and certainly increase my salary. So that is something that I have been contemplating going back into to make additional money. Also, I have explored an additional job, maybe cleaning. I used to take real estate pictures for foreclosures. And when people left and it was disgusting, I would go and clean houses and do that. You could pick and choose what you wanted to do, which I need flexibility when it comes to having my daughter. I would clean houses for that, again, just to make that additional money.

Scott:

I love it. I think it’s not a lot of folks would, I think, do that in your situation. And the fact that you’re willing to do that, the fact that you’re saying, “I want to become financially independent. I want to build wealth. I’m willing to house hack. I’m willing to clean. I’m willing to take on these jobs or fix it up myself.” As a single mom here with that, I think, is super impressive and something that five years from now, when we have you back on the show and you’ve got your $4,000 to $10,000 in passive income from this, you’re going to be an inspiration and very proud of that dynamic. I think it’s awesome and I love that.

Nicole:

I definitely want to make sure that I instill that in my daughter and she sees that hard work, too.

Scott:

All the right things are going on in your financial position. You have been sitting on this particular trajectory for a long time. And I’ve mentioned that before on some of the system of our guests where you come in, you’re eight, 12 months into really absorbing perspective on finance and learning about what good looks like from a personal finance position. You’ve set that up. And you just haven’t been sitting on it for two, three years to stockpile, to see the results of that piling up from a cash position and then in investment form.

So that’s why you feel like you’re behind. But I guarantee you … I don’t guarantee you. I think there’s a high probability that over the next couple of years, you will see the compounding benefits of what you’re doing here if you continue to keep this trajectory going and slowly accelerate it month to month. I think it’s awesome. We answered your question about the 401(k). What other questions do you have?

Nicole:

I haven’t calculated my FI number. Is that something that you could assist me with? And the best way to factor in my military pension.

Scott:

I wouldn’t worry about your FI number right now, honestly. I would worry about it in two years or three years once you’ve got the first $2,000 in passive cash flow. You can absolutely calculate your FI. I’ll give you the technical answer. Right now, you spend $2,600 a month. Therefore, your FI number is somewhere between years three and five when you hit $2,000 to $4,000 in passive cash flow from your real estate investments or other investments. Another way to calculate the FI number is to take the total amount of your assets, like your equity in the real estate, plus your stock market investments and boil it down to the 4% rule.

So right now, you spend 2,600 a month, 2,600 times 12 is going to be 31,200. Therefore, you need about 25 times that amount in assets. That’ll be $780,000. But I believe that as you go down this journey and build up some of those assets and get more confident with your real estate investing career and keep this going, that that number will expand to some degree and be a little higher than the $31,000, $32,000 in annual that you’re spending today. I think that’s why I wouldn’t worry about your number quite yet. I just worry about keeping the trajectory going and building the asset base.

Mindy:

Okay. I’m going to give you a completely different answer because yes, Scott’s right but also Scott’s wrong. So you are spending approximately $32,000 a year. $31,200, let’s round up to $32,000 just to make it easy. That is $780,000 is your FI number. I need to get to this so that I can start withdrawing according to the 4% rule. However, you have a pension. Your pension is $12,000 a year, approximately. So now we’re down to a $480,000 nest egg for you to withdraw from the 4% rule because of your pension. We did a show back on Episode 259 with Grumpus Maximus where he talks about pensions. Should you cash it out? Should you take it as it comes to you? Since it’s a government pension, I would not cash it out. I believe that’s what Grumpus said as well.

The government’s not going to go out of business. If they do, you’ve got way bigger problems than just the fact that your pension’s gone. So I would keep it the way it is. I would also not really worry about it. I say this flippantly and I don’t mean to, but it’s $1,000 a month. That’s not going to be hugely helpful in your … By the time you’re 58, your spending is probably not going to be just this $2,600 that you’re at right now. Maybe your mortgage is paid off and maybe it is only $1,600. And now you’ve got $1,000 from your pension and you need to cover up the $600, or make up the $600 difference and then it would be really helpful. I would keep it in the back of my mind as, “Yes, I will get this someday. But because it isn’t such a large amount of money, I wouldn’t be concerned with it so much. I wouldn’t really factor it in. I would just continue to …”

I mean, if you have $2,000 in passive income in three years and you have $4,000 in passive income in five years, you’re kind of already generating all the income you need without doing anything. You don’t seem like the kind of person who’s just going to be like, “Well, now I’m going to the beach every single day. I don’t have to do a thing for the rest of my life. I’m just going to sit around and do nothing.” I think that understanding the numbers behind the 4% rule are good. But I also think that your $4,000 in passive income goal in five years is not only doable but also a really good FI number for you in general. That’s already more than what you need to live right now.

Nicole:

When I thought about that goal, that was, for me, to live comfortably and be able to take vacations and do whatever I want to do with my daughter, that $4,000 would be comfortable for me. Even though I’m living below that now, it’s for a reason. But I don’t want to continue to live that low. Thank you. That helps me a lot with understanding with that perspective.

Scott:

It’s this trajectory of, “Hey, I’m going to spend at this very low level for a period of time in order to stockpile the asset base. And then as my asset base begins growing and compounding, and that’s a greater and greater percentage of my wealth accumulation, it’s not just coming from the spread between my income and my savings.” You can begin easing off and letting the assets pay for incremental lifestyle expenses. And that’s what I found to be true for my personal life.

I would never have been able to articulate that when I first wrote the book with that but I can see that now. That’s how I would think about the FI journey is. Get the first couple thousand in passive cash flow and then take a look in three, four, five years from position of even greater financial strength and say, “Okay. What is the end game now? And how do I make sure that I’m never dependent on wage income on a go forward basis?” But also have that trajectory to get in the lifestyle I do want at the end state.

Nicole:

Yes.

Mindy:

Okay. Before we let you go, I have one more comment about the VA loan. The VA loan is a wonderful tool for our veterans. I think that it is fantastic. And I think that it also has a lot of stigma around it from real estate agents who don’t necessarily understand what it is and what it does. It is a benefit to you. There’s not really a lot of downside to the sellers. And having a lender who specializes in the VA loan is going to help get your VA loan offers accepted more so than a lender who’s like, “I’ve done them before.” They can take a really long time. They can take forever because there’s all these little steps that you have to do. But a good VA lender knows that you can start all those steps as soon as you go to contract.

I have a VA lender who’s done three VA loans for me, 21 day closes. And that is kind of unheard of in lending in general. But in the VA loan world, I’ve seen people write 45 day VA loan closes. And they’re like, “Well, I hope I don’t have to extend this.” In this market right now, it’s unfortunate, sellers don’t have to jump through hoops and “deal with the problems I’m doing” for those of you who aren’t watching me on video. They don’t have to deal with the problems of the VA loan. There aren’t problems with the VA loan. I have had more problems with FHA loans than I have ever had with a VA loan. They’ve always been smooth sailing. But because there are so many agents who don’t deal with these loans on a regular basis, they can see one and maybe they have two identical offers.

But one is a VA loan and one is a conventional or an FHA. They’ll be like, “I’ve heard VA loans are terrible so I’m just going to go with this one.” So when you go to use your VA loan, make sure you’re using a lender who does them all the time, who knows all the … I don’t want to say loopholes, because that makes it sound like they’re doing something wrong. They’re playing by the book. I mean, it’s a government program. There’s rules and you can either follow them or not get your loan approved. But they jump through all the hoops in such a fashion that it doesn’t take forever to get it closed. That’s my rant. The end.

Nicole:

I actually had a nightmare with purchasing the home that I live in now. The credit union that should deal with lots of VA loans and I literally had to do the work myself to get my certificate of eligibility. They got the wrong one. It was a nightmare. And if you could send me that lender, that would be great because I will not use the lender I used before because I almost lost the house because of how poor of the process it was. And it was a 45 days and they wanted to extend it. It was just a horrible experience. Luckily, everything worked out. But I do not recommend the lender I use. It was a bad process. Like you said, there is a stigma around VA loans, but there’s nothing wrong with them. And the lender makes all the difference.

Mindy:

It really does. I will send you that when we’re off the call.

Nicole:

Thank you.

Scott:

You had at least one more question. I’m cheating here, looking at the notes since you haven’t asked yet. But I think you were wondering about whether 2022 is a good time to do all this stuff. Is that right?

Nicole:

Yeah.

Scott:

I love talking about this one because it’s always on top of everyone’s mind. I bought my first property, a duplex for $240,000 in Denver, Colorado when I was making $50,000 a year and saved up my first 20,000 in 2014. And everyone was talking about how the market had been going up for five, six years in a row, it was absolutely crazy. And there’s no cash flow left in the market in Denver. It was the peak of the market and the bubble was about to burst. I bought the property in November. All of 2015, I was worried about the crash. 2016, second property. 2017, I think it was. The next one, 2018 was the next one. Another one last year. And the whole time, you’re worried about the market conditions. Nobody can predict the market reasonably well.

I will try to pick the market for you anyways in a few seconds here. But I think that it’s just very hard to do that. And it’s like, “I’m going to base my investing philosophy over a lifetime because I would like to be financially free for the entire rest of my life. Not just the next couple of years with this.” So I buy one property every year or two, and don’t worry about the market conditions. I’m just consistent. The strong financial foundations, spending less than you earn and buying and buying and buying and buying. Never to the point where that property can bankrupt you, but always with the idea that long term, that property will go up in value, rents are going to increase. I’m going to pay down the mortgage and it’s going to be a long term winner.

That philosophy I think, is a really powerful position to not worry about the market. Because if the market tanks next year, great. You are going to buy property number two next year and you’re able to get that one at a lower value with that. It’s the dollar cost averaging with real estate, you’d know that long term over a five, 10-year period, if you sustain it, absent apocalypse, which is going to affect everyone, you’re probably going to be in a pretty strong position even if you do have to go through a couple of years of downturn.

That’s the risk we’re going to take with real estate if you’re going to use leverage to buy an asset. But I think that you can feel comfortable over a long period of time that you’re playing the long term averages reasonably well, or at least I do, with that. That’s my answer about the market. And I think that it’s much more predicated on your personal position, which I think is nearing a position of a really strong position to get into real estate with a strong savings rate. Plenty of down payment and $15,000, $20,000, $30,000 left over in cash in emergency reserve.

Now, second part of that, what do I think’s going to happen in 2022? The big question mark this year is interest rates, right? So the Fed is signaled that they’re going to raise interest rates in March and people are pricing in, I’m hearing, up to five interest rate hikes over the course of this year. Long term, the factor, if you forget about those interest rates, you think prices are going to rise. If interest rates were to stay flat, prices should rise. Because millennials are buying homes. There’s a ton of demand. There’s not enough land, there’s enough … The supply and demand factors are really strong for this. I mean, I’m interchanging them. But lots of people want homes. There’s no supply of labor, there’s not a supply of land, there’s not a lot of water in parts of the country. It’s just hard to get these properties built.

And I think Dave Meyer estimates that there’s four million, our VP of data analytics here, estimates that there are four millions home short of meeting demand in the country currently. It’s going to take eight to 10 years at current build rates to really catch that up. But interest rates rise, that can have a big impact on things. And so my prediction for 2022 is that I think interest rates will rise. I’m not clear on how much that will affect pricing. It could be that prices come down, it could be that they don’t appreciate quite as much as they did last year. It could be that they appreciate a tremendous amount because the interest rates don’t rise enough to offset those factors.

What I think might happen this year is that rates will increase, prices may not appreciate as much and rents will rise very quickly relative to that because of inflation. Is that the worst thing in the world if you don’t get that much appreciation? Or even if your property loses some of its value, but rents increase over the next couple of years, if you believe that. I wouldn’t make an investment decision based on a market forecast because no one can predict the market. But I do have fun talking about that and at least thinking through that. That’s my bold hypothesis, is that rent growth will outpace property growth in 2022 for the first time in a while but we’ll see.

Nicole:

After talking to you guys, I’m not going to let any of that hold me back and I’m definitely going to make that next step. Do my research like you said, and make that next step.

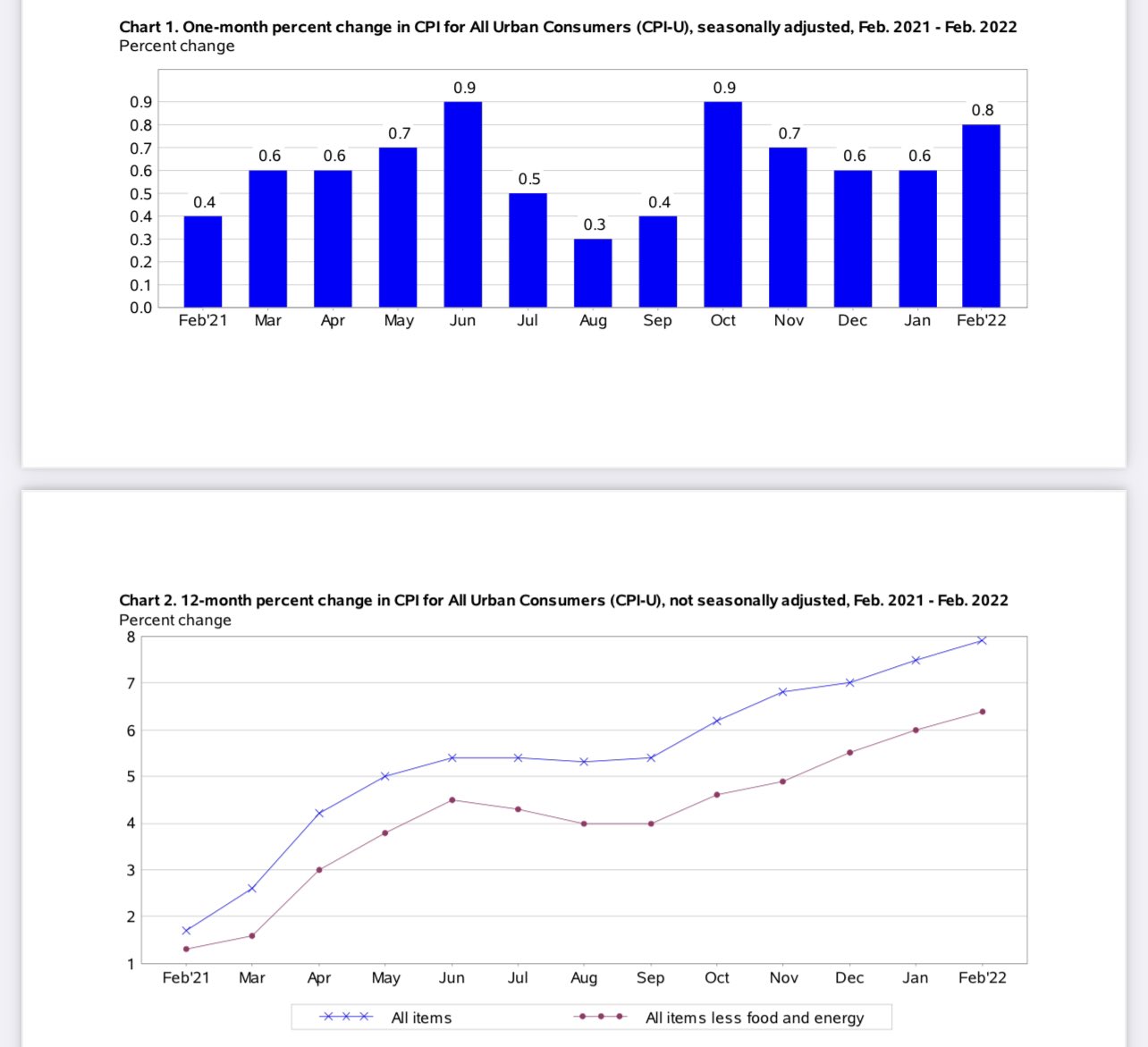

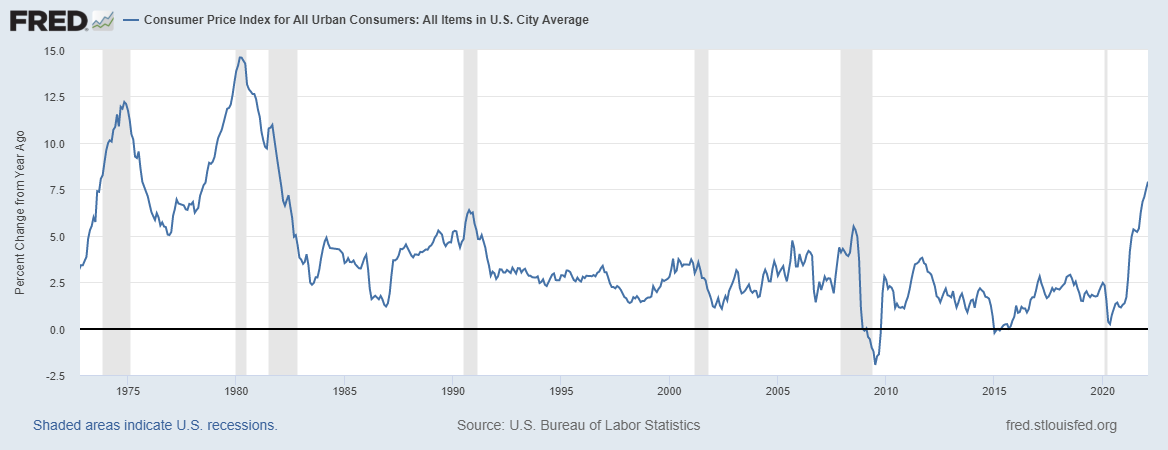

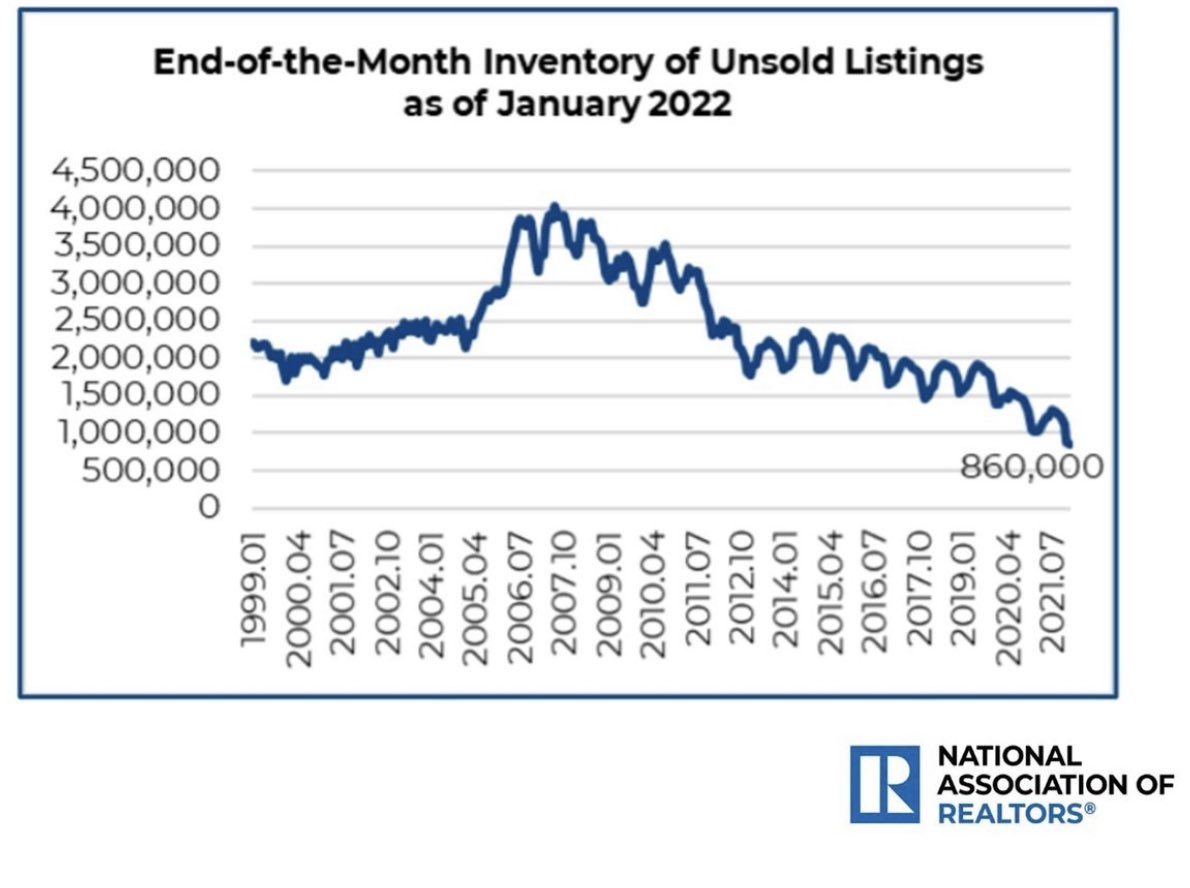

Mindy:

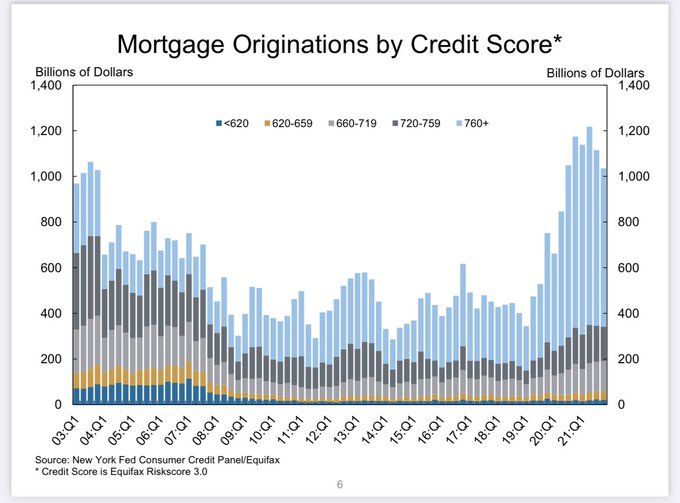

In addition to everything that Scott said, I think we still have low inventory. I’ve got a really great graph that I will include in the show notes, which can be found at biggerpockets.com/moneyshow282. You can also find it at fred.stlouisfed.org/series/houst or just click on the link here. Scott, I shared it in the show notes that we have, and it is showing housing starts dropping from … What is this? 2006. They just went down almost to nothing all the way down to 2009 and they have not come back up to where we were in pre-2006 levels. So I think that there is an enormous shortage of houses to be purchased. So I think that yes, interest rates are going to go up. The Fed has said they’re going to do that. That might cap the skyrocketing prices a little bit but I don’t think that the market is going to just stop. Of course, past performance is not indicative of future gain. Your mileage may vary. Insert other clever comments here.

Scott:

There are no guarantees but I’m planning to buy again this year per my strategy that I outlined.

Mindy:

I’m keeping an eye on the market. When something nice pops up, I might snap it. And if nothing else, I’m helping people buy.

Scott:

Any other questions or things that we can help answer or discuss today?

Nicole:

No. I think you guys really covered it all and gave me a better understanding of what I need to do and just the research I need to make for making that first step into real estate investing. So thank you, I appreciate it.

Scott:

Well, thank you for sharing your story here and for the great discussion today. Thank you for plugging the book and letting us plug a bunch of bigger podcast stuff today. Hopefully, that’s helpful to you. Really look forward to seeing what you end up deciding and doing over the course of this year. I’m very optimistic about the next couple of years from a success standpoint for you.

Nicole:

Thank you. I will keep you guys posted.

Mindy:

Please do. We would love to check back in with you in a few months … Maybe in a year. Let’s see what’s going on in a year.

Nicole:

Let’s go with a year.

Mindy:

Okay, great. Well, we will talk to you soon. Thank you, Nicole. Okay. Scott, that was Nicole. That was a great episode. That was a lot of fun. I’m super excited for all of the options she has available. She’s doing really great. I think that we stink at being supportive and celebrating all the great things that she’s doing. Her budget, her spending is so good without feeling unnecessarily restrictive to her. She’s doing awesome. She’s saving money every month and she’s got clear cut goals. I love her story.

Scott:

What I think was really important that we heard today was Nicole is willing to do whatever it takes to move her financial position to the next level. She is considering moving into a house hacks. She’s willing to move into an Airbnb. She’s willing to clean up really what sounded like horrible messes from foreclosure properties and those types of things to get ahead. She’s not above doing that. And I think that’s what it takes to really get the start of this grind over with. To be willing to take on that house hacks project and to earn those extra bucks by putting in the extra hours and doing the work that you don’t want to do for a couple of years to get that financial foundation. Over the hump where it can begin to support you in the asset base, it gets large enough to start snowballing you.

That asset base outside of your retirement accounts, outside of pensions that only come into play when you turn 58. That asset base that you can actually spend in your early or middle aged adult life with that. I think she’s doing all the right things to set herself up for that. What’s so hard and frustrating for many listeners who are probably in her position is because she’s only been on this trajectory for a year or two, really, and building that financial position, she feels like she’s behind. So just give yourself another one, two, three years if you’re in a position like Nicole’s because you will see those results or you will have very good odds, at least, of seeing those results carry through if you’re willing to pull those big levers and grind it out for a couple years, the snowball will start rolling down the other side of the hill with it.

Mindy:

If you’re listening to the show, if you’re thinking about your finances, if you are tracking your net worth, tracking to your spending, if you are even being conscious of the fact that money comes in and money goes out, you are so far ahead of the average American who doesn’t do any of those things. And she’s got a positive net worth, she’s got a plan, she has well-defined goals. She would really have to try not to succeed. She would have to try to sabotage herself in order to not succeed, just because she’s so driven and she’s going to do the work.

Scott:

But another thing you just said there that’s such a great point, clearly defined goals. It’s so hard to put together a good financial plan and say, “What should I do with my 401(k) or my Roth?” Well, it depends on your goals. “My goal is to save up 20,000. My goal is to get $2,000 a month in passive cash flow within three years. My goal is to get $4,000 within five years.” Okay, great. Now we can work with that and back into that and say, “Well, is that realistic? Well, if you’re willing to clean foreclosures on the weekends and house hack, it’s realistic. If you’re not willing to do those things and want to live in a nice house that’s a big percentage of your income and have your car payment, maybe that’s not realistic for you.” We can give feedback about that.

Mindy:

She doesn’t have the goal of $10,000 in passive income by the end of the year. That’s not a realistic goal. Her goals are realistic, her goals are doable and she’s taking steps to do them. Like you said, she’s willing to do the work. She’s willing to do, what is that phrase? Be willing to live like nobody else now so you could live like nobody else later. She’s willing to go above and beyond, to go extra, to do more so that when she’s a little bit older, she doesn’t have to go above and beyond.

She doesn’t have to do extra. She doesn’t even have to do the bare minimum. It does it for her. It’s called passive income. But you have to do the work now. You can’t just sit around and go on vacations all the time and eat bonbons and go to the beach every weekend. And all of a sudden, life is great and throwing money at you. That’s not how it works. You got to do the work at some point. And she’s ready. She’s willing. She’s going to do it. And she is going to be successful.

Scott:

Love it.

Mindy:

And we’ll check in with her in about a year. I can’t wait to see all of the successes that she’s had in the next year.

Scott:

Absolutely.

Mindy:

Okay. Scott, this was a super fun episode. Are you ready to get out of here?

Scott:

Let’s do it.

Mindy:

From Episode 282 of the BiggerPockets Money Podcast, he is Scott Trench, and I am Mindy Jensen saying, in honor of Girl Scout Cookies season, peace out, Girl Scout.

:215-447-7209

:215-447-7209 : deals(at)frankbuysphilly.com

: deals(at)frankbuysphilly.com