HousingWire Editor in Chief Sarah Wheeler sat down with Jason Cave, former deputy director at the FHFA where he ran their FinTech Office, to talk about where mortgage tech is falling short, and what the government should do to help.

Sarah Wheeler: What led you to leave FHFA for the private sector?

Jason Cave: I spent 30 years in the government — 27 at FDIC and three at FHFA. It was the right time to make a change and I figured it would be neat to work on some of the issues with the fintechs. There are a lot of banking challenges, just like with mortgage, and it felt like a good time to be part of the solution. So, I’ve been helping companies navigate the D.C. landscape, and just helping improve engagement. And it’s a lot of fun to wake up and do a bunch of different things on a given day. I guess I’m a gig economy worker now! A month in, I’m enjoying it.

SW: Looking at the mortgage space, what are some of the challenges when it comes to technology?

JC: There are several, but I think for IMBs specifically, it’s finding a way to get a stable investment track — something that allows you then to be able to continue to build in good times and bad times, because this industry is so boom/bust. And it seems like with technology, even when times are good, a lot of companies aren’t interested because there’s so much money to be made. That’s a broad generalization, but this is coming from discussions with lenders as well as vendors.

And then when times are tough, you know, you’ve just got to hang on and putting that kind of money into technology is tough. Many players in the mortgage space are well behind technological advances, and they need to find ways to really smooth that out, so that they’re continuing to make some investment in all the cycles. That would make them so much more efficient.

SW: You launched FHFA’s Velocity tech sprint in 2023 to bring the industry together to collaborate on solving some of the tech problems we face. What were some of the areas it focused on?

JC: We got a lot of different ideas! A lot of the discussions were very much: ‘let’s not just make incremental changes, let’s really look long-term. Like, how could we actually use blockchain or some form of distributed ledger to really build a better mousetrap?’ But the issue with so many of the ideas is that you have to have the policymakers or regulators, the GSEs, the lenders, and all the other parties on the same page. Now, the positive thing with that is, if you can get that, I think you can make real change.

The downside is that it takes a lot to get everybody there. But I think some of the problems we have today is because it’s so difficult to get everyone at the table. You have a lot of solutions, where it’s like, well, I’m not going to get everybody — I’m going to get a lender and I’m going to get a vendor and then we’re going to do this. And then somebody else says I’m going to get a title company and I’m going to get a POS provider, and we’re going to do this. And that’s quicker and easier, but I don’t know if it’s effective.

At the end of the day, I think we’re finding that companies are having challenges both on adoption and integration. And so maybe this idea of really putting in the time to get everybody at the table and start building makes sense.

A lot of people brought up things [in the tech sprint] that were not heavy lifts, but so important, like down payment assistance. There are so many programs out there, but sometimes in Washington, we forget that just because there are a lot of programs out there, doesn’t mean they’re accessible, doesn’t mean everybody knows about them. We also had some really good ideas about the front end, really being able to pull customer information quicker.

SW: What were some of the themes that came out of the tech sprint that you’re excited about?

JC: The trusted repositories. I’m excited because I think this is something that has not gotten a lot of investment and attention. And I think it goes back to the need for collective action. Just that word itself means you need to have a lot of people that are agreeing to move forward and do these transactions in a different way. And it’s going to affect all of us, but we’re going to be okay with it — we’re going to find a way to make money at it and also be efficient and lay the tracks down.

Blockchain sort of gets a bad name because it’s often connected with crypto. But a lot of these trusted systems run on distributed ledger technology. I’m not a techie, but I’ve looked at it and talked with a lot of people. And when you read what distributed ledger technology is meant for and where it really can bear the greatest fruit, it seems made for mortgage. And I think that’s something that the government and the GSEs are going to really need to encourage — I don’t think this is just going to happen from the bottom up. It’s too much money and it’s too big of a change. So I would like to see that become a priority.

SW: Where else do you think it will take government incentives or at least clearer regulation to advance tech?

JC: We need that sort of strong encouragement/directive even in areas where there’s already been work done. So one of the first things that we wanted to tackle with Velocity was the consumer information and the services that can quickly allow people to transmit what’s normally done in a paper-based, labor-intensive way. Tools such as Day 1 Certainty and AIM have been around for so long — six, seven, eight years — but take up was so low. What is the holdup? What are the bottlenecks? And how do we really push through them? And I think that’s something FHFA and the GSEs need to really push.

When adoption rates are so low, it becomes a vicious cycle. Adoption rates are low, that means people don’t think that the tools are effective, that means that they don’t use it, that means adoption rates go lower.

But think about Day 1 Certainty. I mean, one of its main reasons for coming into existence was to deal with the rep and warranty issue years ago. This isn’t just innovation, this was Fannie Mae and Freddie Mac getting the benefit of a secure, true document — it’s not something I can pull out and doctor up, it’s the actual record. And so it’s safer. You would think some of these tools are just a no-brainer, but I don’t think that’s the case. So that’s an area where Fannie and Freddie as well as FHFA should really push on it.

I would even be so bold to say I think the enterprises should be required to be getting adoption rates of 50% or more, and if they’re not, to really be able to explain why people aren’t using these very important tools they’ve developed. A lot of money has gone into building those tools. Also, to be very transparent, I am advising Argyle and they are one of those providers, so just full disclosure there that I’m advising them. But they and other companies like them are doing really interesting work.

SW: Let’s talk more about direct source data, since it seems like low-hanging fruit, whether that’s credit scores or verification of income and assets.

JC: I couldn’t agree more. And whether it’s The Work Number or credit scores, those are two examples where the consumer is paying that bill directly. And as we already know, closing costs go up every year. It’s an impediment for people — especially those with lower to moderate income — to be able to refinance and get the credit they need. So the more people do what Sandra Thompson is doing by looking at credit scores and trying to create greater competition, the better.

I mean, anytime somebody all of a sudden gets to double their fees because they see that their potential monopolies is threatened, I think it’s a sign that it’s a monopoly! As a taxpayer, I’m flabbergasted to see companies say, now that we might have to lose some of that, we’re going to increase our fees and make it up in the meantime. I think that’s a problem.

And I think that what CFPB did with the proposed Personal Financial Rights Data rule, they have started down that path with making banks share this information. Banks have been able to have a lot of our information locked up, but it’s not locked up for them — they get to use it. And when we want to use it or allow others to use it, it’s not that easy. I applaud the CFPB for really taking issue with that because it is the consumer’s information.

Now, I would say it’d be very nice if the CFPB expanded that to look at things such as payroll and credit scores, because the companies that I just talked about, are unfortunately not getting picked up. It’s the banks, right? And I really do hope that CFPB looks at some of these other companies, who are saying well, we built the pipes, and so we should be able to charge what we want. I don’t think so. There are a lot of subsidies in this housing space. I don’t know who built the pipes. I don’t think anybody on their own, with all their own private money, did it — I think there was a lot of help along the way. And, and again, when you look at who’s paying the bill at the end, it’s really troubling.

SW: What about alternative data? Where is that headed?

JC: I’m not sure where it’s going. I think it’s another one of those areas that with some guardrails, is going to be necessary because of demographics. The reality is that if you do 1099 work, it’s really hard to get a mortgage. I know that from the work we did at FHFA. Those processes are still geared to the 1950s Ward Cleaver family. I’ve heard concerns that some of the alternative credit information is not as robust, it’s not being based on longer-term data histories. I think it’s fine to raise those issues. I don’t think it’s fine to say that means we’re not going to factor it in or we’re going to be very stingy with whatever credit we give for those sorts of things. I think there are some companies like Argyle and others that are finding ways to be able to get that information from good verifiable sources so that lenders can bring that information in into the equation.

SW: What happens to the FHFA’s Velocity tech sprint now that you’re gone?

JC: The Velocity tech sprint and just the FinTech office in general is in very good hands. At FHFA Anne Marie Pippin is continuing to do that work. She did most of the heavy work when I was there, so you’re seeing Anne Marie at the various conferences and panels. FHFA Director Thompson continues to strongly support the work. She has Tracy Stephan, who we brought on board, who was a long term executive at Fannie and also Leah Price has joined recently. And while they have a small group, you’ve got some good leadership and also some people that have actually done this work.

Source link

:215-447-7209

:215-447-7209 : deals(at)frankbuysphilly.com

: deals(at)frankbuysphilly.com

Institutional buyers pumped the brakes on purchase activity in 2023

In December 2023, a startling rumor started to spread on social media — that large institutional buyers had purchased 44% of the available homes on the market in 2023, leaving policymakers concerned with the potentially predatory grip of these entities.

HousingWire lead analyst Logan Mohtashami immediately debunked the claim.

In fact, a recent study published by SFR Analytics shows that purchase activity among institutional buyers significantly decreased in 2023. The 10 largest institutional buyers collectively purchased 1,500 to 3,500 homes per month last year, the study shows. Purchase activity peaked in July, driven by a portfolio acquisition completed by Invitation Homes.

The analysis is limited to resale properties and does not include new construction, which means that build-to-rent activity is excluded.

While it took more than 5,000 acquisitions per year to make it into the top 10 largest single-family rental (SFR) buyers in 2021, the threshold was downsized to 671 in 2023. Zillow, which was the second largest institutional buyer in 2021, exited the home-flipping business in November of that year after failing to accurately forecast the prices for buying and reselling homes.

A variety of companies earned a spot on the top 10 list for 2023, including real estate investment trusts such as Pretium, Amherst, Invitation Homes and Tricon. Two iBuyers, Opendoor and Offerpad, were also on the list.

Choctaw American Insurance was the only lease-to-own company to land on the list. New Western, meanwhile, also stood out as a marketplace for real estate investors.

Opendoor (8,603 homes purchased), New Western (5,233) and Pretium (3,324) reaped the lion’s share of business in 2023, according to SFR Analytics. FirstKey Homes was the only large SFR fund not to be featured on the list.

The hot markets of 2023

Institutional buyers went all in on Dallas in 2023, snagging almost 3,000 homes in the metropolitan area. Atlanta came in second with about 1,900 homes purchased, followed by Houston (1,575) and Phoenix (1,383).

Investors of all sizes purchased 46,419 residential properties in fourth-quarter 2023, according to Redfin data. That amounted to $32.3 billion worth of property, or 10.5% less than in the final quarter of 2022. Meanwhile, total U.S. home purchases fell by 12.2% year over year to 251,462, the lowest fourth-quarter level since 2012, Redfin reported.

To generate its analysis, SFR Analytics leveraged nationwide deed and assessor data to track the single-family rental home market.

Source link

Don’t get too excited about the jump in existing home sales

We got a great existing home sales report on Thursday, but is this data already too old? Existing home sales showed a jump in sales, which was anticipated by most as we had positive, forward-looking housing data due to mortgage rates falling from 8.03% to 6.63%. However, the last four weeks have had negative trending data. This is nothing dramatic, but similar to what we saw in 2023 when mortgage rates rose from 5.99% up to 7.25%.

But before we address this, let’s look at the report because this report still shows what I have believed for a long time: even with elevated mortgage rates and home prices, lower rates lead to more demand as we are working from historically low levels of sales.

Here are some charts reviewing today’s report with a host of data lines from the NAR existing home sales report:

https://www.nar.realtor/newsroom/existing-home-sales-rose-3-1-in-january

A few critical glaring points: active inventory is still historically low, and so is monthly supply data. This is the timeframe where seasonality kicks in for both to go lower and it will be interesting to see where inventory goes this year with the NAR data. Our data lines here at Housing — which track things weekly — show inventory is growing year over year with new listings growth as well.

From NAR: Total existing-home elevated 3.1% from December to a seasonally adjusted annual rate of 4.00 million in January.

Last year, we had 12 weeks of positive, forward-looking housing data, but it all fell into the March report we got for February, so we had a big jump in sales and a lower trend the rest of the year. This year, we might have a split two-month increase in sales before the forward-looking data takes us lower. The recent existing home sales bounce surprised some people, but the context is critical: we were working from a lower bar in sales this year than last year.

The recent move in mortgage rates from 8.03% to 6.63% pushed the purchase application data positive. Since November of 2023, purchase application data was positive for about eight weeks before it turned negative after rates rose to above 7% again.

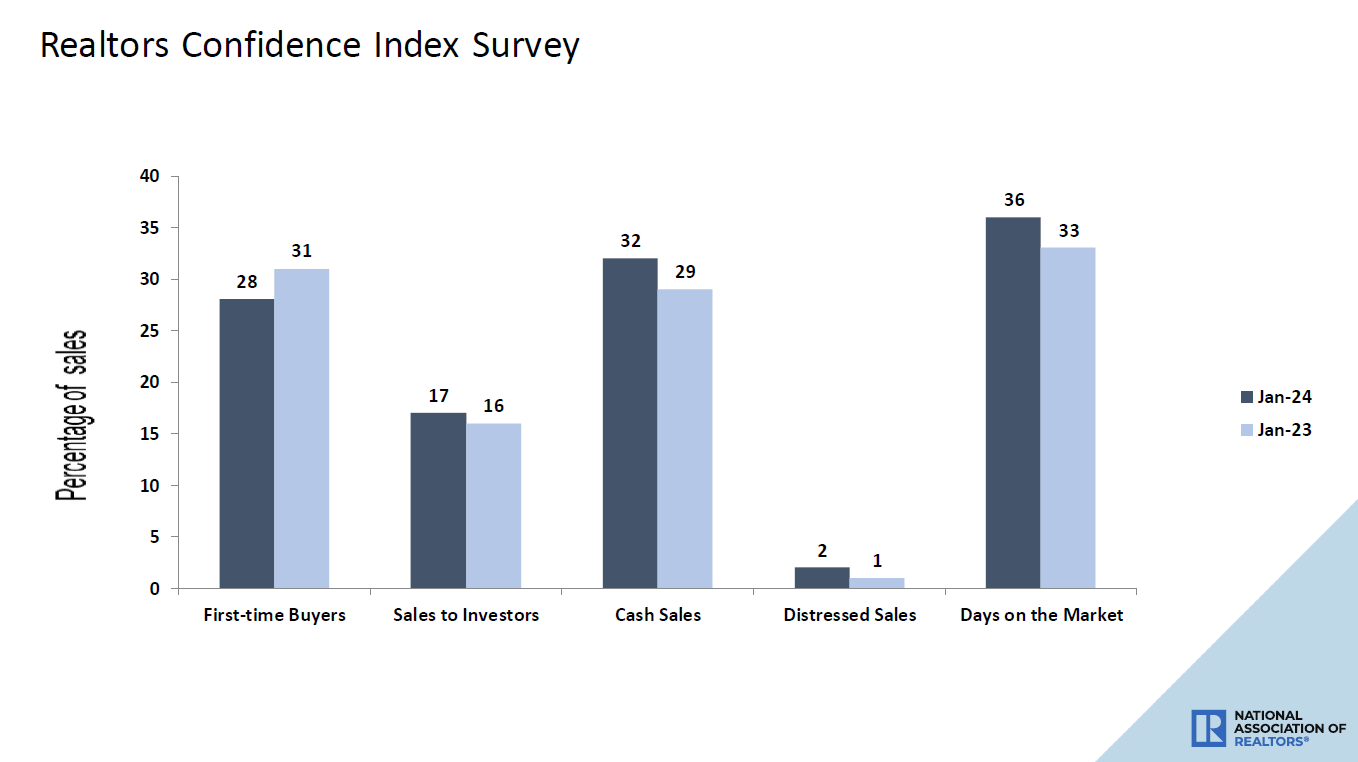

From NAR: First-time buyers were responsible for 28% of sales in January; Individual investors purchased 17% of homes; All-cash sales accounted for 32%; Distressed sales represented 2% of sales; Properties typically remained on the market for 36 days in January.

.

A few notes on the data above: obviously, distressed sales are not a thing and haven’t been for some time. Another positive data line is that the days on market are above 30 days, which is something I would love to see year-round. The days on market are very seasonal, but we haven’t had the days on market stay over 30 days year-round since 2020, which is a reflection of active listings still being near all-time lows.

Cash sales rising year over year looks normal as mortgage demand is lower year over year. So, as it goes with traditional January data, there are no real surprises here but a glimmer of hope that with more inventory this year, the days on market can show year-over-year growth every month.

This existing home sales report was solid, as lower mortgage rates did their thing, but looking at the current data, the last four weeks have had negative purchase application data. Purchase apps look out 30-90 days before they hit sales data. Sometimes it comes early or later in that timeframe, but after eight positive weeks of positive purchase apps, we have now had four straight negative weeks. This means 2024 is starting to look a lot like 2023 unless rates fall soon.

We don’t want to see mortgage rates break out toward 8%; even the Fed has said getting to 8% was a restrictive policy and something that isn’t in its interest. So let’s keep an eye out on that 4.34% level on the 10-year yield and hope that doesn’t break. Otherwise we could have a horrible carbon copy of what we saw in 2023.

Source link

Why is Fannie Mae optimistic about a housing market recovery?

The year 2024 has started with cautious optimism that mortgage rates will drop, sparking much-needed activity in the sluggish U.S. housing market.

Mortgage rates, however, have been on a rising trend of late. Recent data shows that the economy is booming, while the Federal Reserve is signaling that it will take its time before cutting benchmark interest rates.

HousingWire’s Mortgage Rates Center showed the 30-year fixed-rate mortgage at 7.21% on Feb. 23. And according to Freddie Mac‘s Primary Mortgage Market Survey, the average rate inched closer to 7% this week.

Fannie Mae, however, remains optimistic that housing market activity will pick up as existing home sales and new single-family housing starts are expected to grow modestly in 2024.

While existing home sales dipped slightly in December by 1% to a seasonally adjusted annual rate of 3.78 million units, an increase in mortgage applications and December pending home sales that led to average closing times of 30 to 45 days indicate that a modest rebound in sales is underway.

With a low supply of existing homes for sale, demand for new homes is likely to remain strong, and the limit on new home sales will be determined by homebuilder production capacity, according to a report released Friday by Fannie Mae’s Economic and Strategic Research (ESR) group.

“Single-family permits in contrast edged up 1.6 percent in January, back in line with the overall starts series,” the report noted. “With single-family permits and starts now back in alignment, we expect new single-family construction to continue to drift upward in coming months.”

Fannie Mae forecasts total mortgage origination volume of $1.92 trillion in 2024, down slightly from $1.98 trillion in its previous forecast. Volume is expected to climb to $2.36 trillion in 2025, compared to the ESR group’s January forecast of $2.44 trillion.

Softening economic growth anticipated

The ESR group upgraded its 2024 macroeconomic growth outlook due to a stronger-than-expected fourth-quarter 2023 gross domestic product (GDP) report, as well as incoming data on recent population growth and immigration trends that point to faster payroll and GDP gains over the forecast horizon.

Fannie Mae’s 2024 GDP outlook is for 1.7% growth in 2024, compared to 3.1% in 2023. The ESR group previously forecast a “mild recession” for 2024.

“An unsustainably low savings rate suggests softer consumer spending going forward, consistent with the pullback in January retail sales, and slowing local and state tax receipts point to slower direct government spending growth,” the report stated.

Further, while payroll growth looks to have reaccelerated in December and January, other labor market measurements indicate softness. The ESR group expects that the labor market “on net” is likely to cool in the near future.

“Market dynamics continue to reflect significant uncertainty regarding the sustainability of stronger-than-expected recent GDP growth, the continuity of the decline of inflation, and the path of monetary policy change, not to mention the many ways in which historical relationships in housing and the larger economy remain out of balance post-pandemic,” Doug Duncan, Fannie Mae senior vice president and chief economist, said in the report.

Source link

Industry experts are closely watching delinquency rates, insurance costs

Mortgage servicers, regulators and economists are closely watching the delinquency rates for Federal Housing Administration (FHA) loans following a spike in the fourth quarter of 2023.

Industry experts say that although there’s a correlation between unemployment and delinquency rates, some homeownership costs — including insurance — have increased significantly over the past two or three years, which has had a strong financial impact on homeowners. But experts also say the situation is not as bad as the one experienced during the COVID-19 pandemic.

The sources spoke about these issues during this week’s Mortgage Bankers Association (MBA) Servicing Solutions Conference & Expo in Orlando.

The latest MBA data shows that the delinquency rate for one- to four-unit properties rose to 3.88% at the end of 2023, compared to 3.62% in the third quarter, but still below the historic average of 5.25%. Meanwhile, the FHA-insured loan delinquency rate recorded a larger jump during the same period to 10.81%, up from 9.5%, the highest level since Q3 2021.

“We are seeing a bit of a pickup for two quarters in a row, but it’s very important to keep in mind that we were at the absolute lowest point in delinquencies in the third quarter of 2023,” Marina Walsh, MBA vice president of industry analysis, research and economics, said in a market outlook session.

According to Walsh, the delinquency rate for FHA loans increased by 130 basis points from the third to fourth quarters, but the current level is “certainly not nearly where it was at the height of COVID-19.”

In addition, she said that foreclosures are not picking up, so borrowers are either paying off their loans before entering the severe delinquency stage, or if they are in the serious delinquency stage, they are entering a workout.

“The question I posed to all of you is, ‘Is this a blip or a bigger trend?’” Walsh said, adding that based on data MBA has received from the industry, she believes the delinquency rate could come down a bit in first-quarter 2024 following the end of the busy holiday shopping season.

“All these increases in costs impact people’s ability to pay, without question,” Steven R. Bailey, senior managing director and chief servicing officer at PennyMac Financial Services, said in an executives’ perspective session. “But we still see the strongest correlation is between unemployment and delinquency.”

Bailey said that although increases in delinquencies are not a trend that servicers want to see, “I don’t look at it with the same fear that I used to look like.”

Homeowners insurance

According to industry experts, one of the costs affecting homeowners is their insurance, which can lead to increases in delinquencies. California and Florida are among the states where the situation is more evident.

Seven of the 12 largest insurers in California have either paused or restricted new policies over the past 18 months, including State Farm and Allstate. In September, the state’s top insurance regulator announced that new rules are in the works to persuade insurers to remain.

In Florida, the departure of many insurers and reinsurers has resulted in homeowners paying an average of nearly $4,000 a year, almost three times the U.S. average, according to estimates from the Insurance Information Institute. In some instances, homeowners have seen their insurance costs more than triple, but a new bill seeks to help them.

“That’s a combination of both rates from a carrier perspective, as well as just the increase in home values,” Patrick A. Sullivan, vice president of industry relations and compliance at Assurant, said in a session about homeowners insurance.

Sullivan said reinsurance is another factor weighing on homeowners insurance costs, a function of the global capital markets. He added that reinsurance costs have more than tripled over the past three years.

“Homeowners insurance is certainly a problem we need to tackle together,” John Bell, executive director of loan guaranty service at the U.S. Department of Veteran Affairs (VA), said during a regulatory session.

“I hope that there are others on this panel and others out there that want to work together to try to solve some of those rising prices that our homeowners just can’t absorb, and at some point in time, it’s going to hurt the market.”

Bell said that if a home costs $800 per month more than last year, the industry needs to figure out how to solve it. Bell and the VA are working to move forward with options to help veterans avoid foreclosure, including a partial claim solution.

FHA Commissioner Julia Gordon, who announced the agency’s new payment supplement partial claim during the conference, added that the issue of homeowners insurance will take a village to tackle.

“And that’s going to take real work in the states also, which is hard, and we just have to do it if we want people to be protected,” Gordon said.

Source link

7 ways to avoid being a ‘broke’ real estate broker

For many real estate agents, a logical step on their path of professional development is becoming a real estate broker, then working as either a managing broker or a broker-owner.

However, unlike other industries where promotion to the management level is generally tied to additional income, some brokers find themselves struggling to perform at the same financial level as their most successful agents.

For brokers who are franchise owners in a big-box brokerage model, upstream costs can make it difficult to maintain profitability. For brokers who are indie broker-owners, overhead and operating costs can make it practically impossible, especially during the start-up years.

It’s no fun being the broke broker, and it can keep you from offering your agents the support they need to grow their businesses and, by extension, your business. Here are seven ways to ensure you avoid being the brokest person in your business:

1. Determine whether you’ll be a competing or non-competing broker

You may find that you can’t secure your own income without being in production, at least initially. Make sure that you have a plan in place to feed leads to your agents as needed or that the agents you’re recruiting are experienced enough that they won’t feel like you’re working against their interests.

2. Develop a profitable commission structure

Make sure that you crunch the numbers on your commission structure to ensure you can operate profitably and in a way that allows you to earn an income that’s fair, competitive and aligned with market standards for your area.

3. Focus on volume or premium listings (or both)

Make sure that your marketing and branding allows your agents to secure higher volume or premium listings so that they (and you) can generate larger commissions. Provide the support and resources needed to help your agents work in these markets.

4. Leverage your expertise

Perhaps you have a wide network that allows you to develop relationships with other brokers and pursue high-net-worth clients. Perhaps you’ve developed specialized expertise that would allow your brokerage to dominate a specific niche or market segment. Position yourself as an industry leader and subject matter expert, and develop your unique value proposition to enhance the reputation of both your and your firm.

5. Optimize your management

Make sure that you’re doing what’s best for your agents so that they can produce at the highest possible level — and so that you spend less time on recruitment, onboarding and retention activities. Expand your team in a smart way so they’re happy to support each other instead of competing with each other for crumbs.

6. Diversify streams of income

Add additional services to your brokerage’s offerings, from property management to consultation and investment services. Pursue strategic partnerships with lenders or title companies. Start a real estate school or use your professional expertise to develop your own real estate investment portfolio. The more ways you make money, the higher your income and the better protected you are in the face of market adjustments.

7. Draw on the expertise of others

Work with a tax strategist and employ a fractional CFO to ensure that you’re making smart decisions with every dime that goes in or out of your brokerage. Make sure that you’re doubling down on the activities that generate revenue and delegating the support tasks to others so that you can use your talents in the best way possible.

Your financial success depends on your agents — and vice versa. Make sure that you’re creating a business where everyone can succeed, including (and especially) you.

Troy Palmquist is director of growth for eXp California.

Source link

RE/MAX looks to teams to boost its U.S. agent count

Less than 24 hours after announcing Nick Bailey’s departure from the firm, RE/MAX executives found themselves on a call with investors and analysts to discuss the company’s fourth-quarter and full year 2023 earnings.

In his opening remarks, Erik Carlson, who was named CEO of RE/MAX Holdings in November, mentioned the promotions of Amy Lessinger, who is replacing Bailey as RE/MAX president, Abby Lee and Susie Winders, but he made no mention of Bailey other than to note his departure. Additionally, no analysts asked questions about the changes the firm made to its C-suite.

“These are well-deserved positive changes that I believe will help us navigate the road ahead and realize our full potential,” Carlson said.

In their new roles, the firm’s new leaders find themselves tasked with getting RE/MAX back on a profitable track. Despite losing $10.9 million in Q4 2023 and a total of $69 million for the full year, RE/MAX’s revenue of $76.6 million in Q4 was down only 5.7% year over year, while the $325.7 million in yearly revenue was down 7.8%.

These results came as the number of existing home sales dropped 18.7% year over year in 2023 to a near 30-year low of 4.09 million. RE/MAX’s U.S. agent count, meanwhile, fell from 58,719 at end of 2022 to 55,131 at end of 2023.

The company’s global agent count is up 0.6% annually to 144,835, due to slight growth in its Canadian agent count and a strong uptick in its international agent count, the latter of which rose from 60,175 at the end of 2022 to 64,536 at the end of 2023.

With this in mind, Carlson said two of the firm’s main priorities are to stabilize and grow its U.S. agent count and to expand its mortgage business. He said leaders are confident that these areas can “grow into a meaningful revenue business.”

“Posting gains in those two areas would build market share, increased revenue and earnings, and will create momentum for additional growth,” Carlson said.

As RE/MAX has attempted to overcome the challenges posed by housing market conditions, executives said they have reevaluated some of the programs the company offers in an effort to pinpoint which initiatives are worth further investment. One such program, Carlson said, is its teams initiative, which is launched in mid-2022 and expanded again in 2023.

“As a result of the program impact and our lessons learned, we are expanding the modified version of the program to encourage team recruitment and growth across much of the U.S.,” Carlson said. “From our perspective this is prudent, proven investment that will help franchises grow their offices, help team leaders build larger teams and, simultaneously, it sends a message across the industry that teams have yet another reason to affiliate with RE/MAX.”

Under the modified teams program, in order to unlock the program’s financial incentives (which include reduced recurring fees and a broker fee cap), a brokerage in an eligible state must first add any combination of six team leaders or members from outside the RE/MAX network.

RE/MAX executives also addressed the commission lawsuits and the firm’s settlement agreement related to the Sitzer/Burnett, Moehrl and Nosalek suits, which was confirmed as a nationwide settlement.

“While the settlement came at a significant financial cost, we believe it was the right decision for all our stakeholders, affiliates, employees, shareholders and debt holders alike,” Carlson said. “We view it as an investment in the brands, the networks, the franchisees and, most importantly, the agents.”

Executives noted they were “cautiously optimistic” about the settlement gaining final approval in May, an outcome that would see copycat litigation also go away. They also noted that RE/MAX is viewing this as an opportunity to further double down on agent education.

“In RE/MAX University, we offer something called the Accredited Buyer Representation Designation, which gives our agents education on exactly how to articulate their value proposition, so we anticipate that there will be more demand for that as we move forward,” Lessinger said.

As RE/MAX heads further into 2024, executives said they expect to continue seeing a purge of nonproductive agents across the industry, as well as more transactions in 2024 than in 2023, which they believe will serve their highly productive agents well.

Source link

Title earnings marred by slow market, cybersecurity incidents

Despite slower housing market conditions, Big Four title firms Stewart, First American and Fidelity National Financial all managed to earn profits in 2023.

Stewart, which reported its earnings earlier in February, posted a revenue of $2.26 billion in 2023 and a net income of $30.4 million. Both figures were down significantly from 2022 when it recorded $3.07 billion in revenue and net income of $162.3 million.

In fourth-quarter 2023, Stewart earned revenue of $582.2 million and net income of $8.8 million, which was down from the $13.3 million in net income it earned a year ago. Despite declines in title transaction volume, Stewart’s title segment still reported an operating revenue of $503 million for Q4, down 14% annually, and a pretax income of $27.3 million, down 2% annually.

On a call with investors and analysts, Stewart CEO Fred Eppinger noted that the company’s focus in 2023 was on creating a more resilient firm that would be able to succeed in all phases of the real estate market cycle.

“As we close 2023, we are operating in an environment that saw mortgage interest rates reach a high of 8% during the fourth quarter before falling to around mid-6% near the end of the year,” Eppinger said.

“Mortgage rates and rate volatility continue to impact transaction volumes, and we find ourselves at historic lows for sale of existing homes. As I have said before, we see 2024 as a transition year toward a more normal market for existing home sales during 2025 and believe the next six months will likely be very challenging given the macroeconomics laid on top of a typical seasonal impact.”

To achieve its goal, Eppinger noted that Stewart is focusing on improving its technology and efficiency.

“These strategic investments are resulting in cost ratios that are somewhat elevated given we are in a market with historically low transaction volumes,” Eppinger said. “However, we are setting Stewart up for better overall performance in the future. We believe that these long-term investments coupled with thoughtful near-term expense management will improve our structure and financial performance in the long term.”

Executives at First American also lamented the challenging housing market conditions posed in 2023.

“While difficult market conditions will likely persist this year, we do expect to benefit from modest growth in both our residential and commercial businesses, but this could change depending on the path of mortgage rates,” First American CEO Ken DeGiorgio told investors and analysts on the firm’s Q4 2023 earnings call earlier this month.

“We continue to run our business efficiently and maintain a strong balance sheet, which allows us to invest in strategic initiatives that support long-term growth, while returning capital to shareholders.”

In 2023, First American recorded total revenue of $6.004 billion, down from $7.605 billion in 2022. Its net income last year was $216.8 million, down from $263 million a year prior. This decrease came as the number of title orders opened during the year fell from 895,500 in 2022 to 629,100 in 2023.

Additionally, First American’s title revenue fell by roughly $1.8 billion from 2022, finishing last year at $5.725 billion, as the title segment’s net income dropped from $757.4 million to $494 million during the year.

In Q4 2023, First American reported a 15% year-over-year decrease in revenue to $1.429 billion, along with a $20 million decline in net income to $34.1 million. Title revenue for the quarter also fell to $1.321 billion, as the number of title orders opened dropped from 153,100 in Q4 2022 to 124,600 in Q4 2023.

DeGiorgio noted during the call that the firm’s financial results were materially impacted by the December cybersecurity incident that resulted in First American’s systems going offline for a few days.

“We were performing well in a challenging market ahead of the cybersecurity incident that occurred in late December,” DeGiorgio said. “We elected to take systems offline, which materially impacted the company’s operations and, consequently, our fourth-quarter financial results. Our title orders and related product demand appear to have returned to normal levels, however. We expect no significant ongoing impact from the incident.”

He also noted that the firm was grateful for the support and patience of agents, customers and other industry participants during the cybersecurity incident.

Cybersecurity was also a topic of discussion on Fidelity’s Q4 2023 earnings call, as the firm suffered its own attack just weeks before First American was hit. According to CEO Mike Nolan, Fidelity’s Q4 2023 title segment results were negatively impacted by the incident.

“We estimate the incident reduced adjusted pretax title earnings by $8 million to $10 million and lowered our adjusted pretax title margin by roughly 50 basis points and 12.3%, which would have been in line with the prior year quarter to 11.8% as reported,” Nolan told investors and analysts during the firm’s Q4 2023 earnings call.

“As challenging as this event was, it really showcased how our team pulled together.”

Despite the cybersecurity incident, Fidelity’s title segment performed well in both Q4 and full year 2023, reporting revenue of $1.7 billion for the quarter and $7.038 billion for the year. The title segment reported an adjusted net income of $174 million for the fourth quarter and $760 million for the full year. Both of these figures were down from $180 million in Q4 2022 and $1.2 billion in full year 2022.

These results came even as the number of purchase orders opened during the quarter were down 1% and the number of refinance orders opened were down 11% annually.

Due to losses reported by the firm’s corporate and F&G Annuities and Life segments during the fourth quarter, Fidelity as a whole reported a net loss of $69 million during these three months, even as revenue rose from $2.557 billion in Q4 2022 to $3.432 billion in Q4 2023.

For full year 2023, the firm reported total revenue of $11.752 billion and net earnings of $517 million.

Looking ahead, Nolan is optimistic about how the firm will fare in 2024.

“As always, we will manage our business to the trend in opened orders to protect our profitability,” he said. “We feel that we are well positioned for the current market and poised to benefit from a potential turn in the housing market, should mortgage rates drop in 2024. Beyond the near-term pressures, we remain bullish on the mid- to long-term fundamentals of the real estate market.”

Source link

Jason Cave, formerly of FHFA, on government’s role leading tech

HousingWire Editor in Chief Sarah Wheeler sat down with Jason Cave, former deputy director at the FHFA where he ran their FinTech Office, to talk about where mortgage tech is falling short, and what the government should do to help.

Sarah Wheeler: What led you to leave FHFA for the private sector?

Jason Cave: I spent 30 years in the government — 27 at FDIC and three at FHFA. It was the right time to make a change and I figured it would be neat to work on some of the issues with the fintechs. There are a lot of banking challenges, just like with mortgage, and it felt like a good time to be part of the solution. So, I’ve been helping companies navigate the D.C. landscape, and just helping improve engagement. And it’s a lot of fun to wake up and do a bunch of different things on a given day. I guess I’m a gig economy worker now! A month in, I’m enjoying it.

SW: Looking at the mortgage space, what are some of the challenges when it comes to technology?

JC: There are several, but I think for IMBs specifically, it’s finding a way to get a stable investment track — something that allows you then to be able to continue to build in good times and bad times, because this industry is so boom/bust. And it seems like with technology, even when times are good, a lot of companies aren’t interested because there’s so much money to be made. That’s a broad generalization, but this is coming from discussions with lenders as well as vendors.

And then when times are tough, you know, you’ve just got to hang on and putting that kind of money into technology is tough. Many players in the mortgage space are well behind technological advances, and they need to find ways to really smooth that out, so that they’re continuing to make some investment in all the cycles. That would make them so much more efficient.

SW: You launched FHFA’s Velocity tech sprint in 2023 to bring the industry together to collaborate on solving some of the tech problems we face. What were some of the areas it focused on?

JC: We got a lot of different ideas! A lot of the discussions were very much: ‘let’s not just make incremental changes, let’s really look long-term. Like, how could we actually use blockchain or some form of distributed ledger to really build a better mousetrap?’ But the issue with so many of the ideas is that you have to have the policymakers or regulators, the GSEs, the lenders, and all the other parties on the same page. Now, the positive thing with that is, if you can get that, I think you can make real change.

The downside is that it takes a lot to get everybody there. But I think some of the problems we have today is because it’s so difficult to get everyone at the table. You have a lot of solutions, where it’s like, well, I’m not going to get everybody — I’m going to get a lender and I’m going to get a vendor and then we’re going to do this. And then somebody else says I’m going to get a title company and I’m going to get a POS provider, and we’re going to do this. And that’s quicker and easier, but I don’t know if it’s effective.

At the end of the day, I think we’re finding that companies are having challenges both on adoption and integration. And so maybe this idea of really putting in the time to get everybody at the table and start building makes sense.

A lot of people brought up things [in the tech sprint] that were not heavy lifts, but so important, like down payment assistance. There are so many programs out there, but sometimes in Washington, we forget that just because there are a lot of programs out there, doesn’t mean they’re accessible, doesn’t mean everybody knows about them. We also had some really good ideas about the front end, really being able to pull customer information quicker.

SW: What were some of the themes that came out of the tech sprint that you’re excited about?

JC: The trusted repositories. I’m excited because I think this is something that has not gotten a lot of investment and attention. And I think it goes back to the need for collective action. Just that word itself means you need to have a lot of people that are agreeing to move forward and do these transactions in a different way. And it’s going to affect all of us, but we’re going to be okay with it — we’re going to find a way to make money at it and also be efficient and lay the tracks down.

Blockchain sort of gets a bad name because it’s often connected with crypto. But a lot of these trusted systems run on distributed ledger technology. I’m not a techie, but I’ve looked at it and talked with a lot of people. And when you read what distributed ledger technology is meant for and where it really can bear the greatest fruit, it seems made for mortgage. And I think that’s something that the government and the GSEs are going to really need to encourage — I don’t think this is just going to happen from the bottom up. It’s too much money and it’s too big of a change. So I would like to see that become a priority.

SW: Where else do you think it will take government incentives or at least clearer regulation to advance tech?

JC: We need that sort of strong encouragement/directive even in areas where there’s already been work done. So one of the first things that we wanted to tackle with Velocity was the consumer information and the services that can quickly allow people to transmit what’s normally done in a paper-based, labor-intensive way. Tools such as Day 1 Certainty and AIM have been around for so long — six, seven, eight years — but take up was so low. What is the holdup? What are the bottlenecks? And how do we really push through them? And I think that’s something FHFA and the GSEs need to really push.

When adoption rates are so low, it becomes a vicious cycle. Adoption rates are low, that means people don’t think that the tools are effective, that means that they don’t use it, that means adoption rates go lower.

But think about Day 1 Certainty. I mean, one of its main reasons for coming into existence was to deal with the rep and warranty issue years ago. This isn’t just innovation, this was Fannie Mae and Freddie Mac getting the benefit of a secure, true document — it’s not something I can pull out and doctor up, it’s the actual record. And so it’s safer. You would think some of these tools are just a no-brainer, but I don’t think that’s the case. So that’s an area where Fannie and Freddie as well as FHFA should really push on it.

I would even be so bold to say I think the enterprises should be required to be getting adoption rates of 50% or more, and if they’re not, to really be able to explain why people aren’t using these very important tools they’ve developed. A lot of money has gone into building those tools. Also, to be very transparent, I am advising Argyle and they are one of those providers, so just full disclosure there that I’m advising them. But they and other companies like them are doing really interesting work.

SW: Let’s talk more about direct source data, since it seems like low-hanging fruit, whether that’s credit scores or verification of income and assets.

JC: I couldn’t agree more. And whether it’s The Work Number or credit scores, those are two examples where the consumer is paying that bill directly. And as we already know, closing costs go up every year. It’s an impediment for people — especially those with lower to moderate income — to be able to refinance and get the credit they need. So the more people do what Sandra Thompson is doing by looking at credit scores and trying to create greater competition, the better.

I mean, anytime somebody all of a sudden gets to double their fees because they see that their potential monopolies is threatened, I think it’s a sign that it’s a monopoly! As a taxpayer, I’m flabbergasted to see companies say, now that we might have to lose some of that, we’re going to increase our fees and make it up in the meantime. I think that’s a problem.

And I think that what CFPB did with the proposed Personal Financial Rights Data rule, they have started down that path with making banks share this information. Banks have been able to have a lot of our information locked up, but it’s not locked up for them — they get to use it. And when we want to use it or allow others to use it, it’s not that easy. I applaud the CFPB for really taking issue with that because it is the consumer’s information.

Now, I would say it’d be very nice if the CFPB expanded that to look at things such as payroll and credit scores, because the companies that I just talked about, are unfortunately not getting picked up. It’s the banks, right? And I really do hope that CFPB looks at some of these other companies, who are saying well, we built the pipes, and so we should be able to charge what we want. I don’t think so. There are a lot of subsidies in this housing space. I don’t know who built the pipes. I don’t think anybody on their own, with all their own private money, did it — I think there was a lot of help along the way. And, and again, when you look at who’s paying the bill at the end, it’s really troubling.

SW: What about alternative data? Where is that headed?

JC: I’m not sure where it’s going. I think it’s another one of those areas that with some guardrails, is going to be necessary because of demographics. The reality is that if you do 1099 work, it’s really hard to get a mortgage. I know that from the work we did at FHFA. Those processes are still geared to the 1950s Ward Cleaver family. I’ve heard concerns that some of the alternative credit information is not as robust, it’s not being based on longer-term data histories. I think it’s fine to raise those issues. I don’t think it’s fine to say that means we’re not going to factor it in or we’re going to be very stingy with whatever credit we give for those sorts of things. I think there are some companies like Argyle and others that are finding ways to be able to get that information from good verifiable sources so that lenders can bring that information in into the equation.

SW: What happens to the FHFA’s Velocity tech sprint now that you’re gone?

JC: The Velocity tech sprint and just the FinTech office in general is in very good hands. At FHFA Anne Marie Pippin is continuing to do that work. She did most of the heavy work when I was there, so you’re seeing Anne Marie at the various conferences and panels. FHFA Director Thompson continues to strongly support the work. She has Tracy Stephan, who we brought on board, who was a long term executive at Fannie and also Leah Price has joined recently. And while they have a small group, you’ve got some good leadership and also some people that have actually done this work.

Source link

Hispanic household wealth tripled over the past decade: NAHREP

Hispanic household wealth ballooned to $63,400 in 2022, growing more rapidly than any other demographic group in the country, according to a recent report published by Hispanic Wealth Project, a nonprofit established by the National Association of Hispanic Real Estate Professionals (NAHREP).

While other racial and ethnic demographics have seen an increase in household wealth during that same period, Latinos were the only racial or ethnic demographic to increase their wealth by more than threefold over the last decade from $19,998 in 2013.

Homeownership led Hispanic household wealth growth, which is the single greatest contributor to wealth for most American families, the report noted.

Hispanic families who own their homes have on average 26.4 times the net worth of those who rent.

As of late 2023, Latinos had a homeownership rate of 49.5%, just shy of NAHREP’s goal of 50%.

“Continued Hispanic homeownership rate increases, in combination with recent home price appreciation, has substantially boosted Hispanic household wealth,” said the report.

One-third of Hispanic household wealth could be attributed to home equity, or equity held in a primary residence in 2022. This was a substantial increase from 2013 when Latinos held just 26.7% of their net worth in their homes.

In 2019, homeowning Latino families had a median $109,081 in home equity — calculated as value of primary residence minus mortgage debt.

By 2022, Latino’s home equity increased by nearly 40% to $150,000 driven by home prices that skyrocketed during the COVID-19 pandemic.

When considering all property holdings, including equity in residential and non-residential investment properties, real estate consists of 45.5% of Hispanic household wealth.

Beyond homeownership, real estate served as a strong investment vehicle for Latino families.

Between 2013 and 2022, the share of Hispanic households owning investment properties increased from 7.3% to 9.5%.

Despite a significant Hispanic household wealth growth, a sizable wealth gap between Hispanic and non-Hispanic White households persists.

In 2022, non-Hispanic White households held an additional $219,900 in median net worth over their Latino counterparts. Similarly, the general population holds more than twice the wealth of Hispanic households.

Latinos still have a lower share of investment property ownership than the general population at 13% and the non-Hispanic White population at 14.4%.

In the past, the Hispanic community’s over-investment in real estate and limited diversification left it “particularly vulnerable during the economic crises,” the report pointed out.

“Asset diversification is critical to the creation of wealth and financial security … Fortunately, the proportion of Latinos investing in various asset categories, particularly non-cash financial assets is increasing.”

“Education is crucial to understanding the value of diversification, and mandating financial education in public schools is an important first step in teaching younger members of the community the fundamentals of financial security,” said the Hispanic Wealth Project.

Source link

More Units Doesn’t Mean More Money—Why a Single-Family Home Can Beat a Fourplex

The notion that investing in multifamily is always better than investing in single-family is false. The goal of real estate investing isn’t to own a particular type of property but to secure a reliable income. The reliability of this income doesn’t depend on the property type but on the tenant who occupies the property.

To show you what I mean, I will compare the financial performance of a typical fourplex in Las Vegas to the kinds of properties we’ve targeted over 16 years.

Typical Las Vegas Fourplex Characteristics

Note: The property cost and rent came from averaging the 36 fourplexes for sale today (Jan. 31, 2024). The typical in-between tenant renovation cost came from property managers who specialize in multifamily properties.

Almost all fourplexes in Las Vegas were built before 1986 and are located in distressed areas. The typical tenant stays less than one year, and the time to renovate and re-rent is three months. The typical cost for the in-between tenant renovation is $2,000.

The typical unit rent is $800 to $900 a month. The typical cost to buy a fourplex in reasonable condition is $650,000 to $700,000.

Assuming a one-year tenant stay, the unit is vacant three months out of every 15 months. Assuming a higher-end $900/month rent:

Our Single-Family Target Property Characteristics

Out of our over 490 properties, the average tenant stays for more than five years. The typical in-between tenant renovation cost is $500. The time to renovate and re-rent is one month.

For the property segment we target, $700,000 can get you two properties. The typical rent for such a property is $1,800-$1,900/month.

Assuming an average $1,850/month rent:

This means the net rent from the Las Vegas fourplex over a 10-year period is significantly lower than that from two single-family homes. This is due to shorter tenant stays, longer vacancies, and higher turnover/repair costs.

Other Considerations

Here are some other factors to keep in mind.

Low income reliability

The tenant segment that occupies fourplexes in Las Vegas is near-minimum-wage workers. They are typically the first to be laid off and the last to be rehired during economic downturns.

During the 2008 financial crash, many multifamily properties were vacant and boarded up. Many were foreclosed upon. However, our clients had zero decrease in rent and zero vacancies during the same period. The difference was due to the different tenant segments the properties attracted.

Limited rent growth

Because near-minimum-wage workers occupy multifamily properties in Las Vegas, the rent is tied to the minimum wage, which is currently $12/hour. So, you cannot increase the rent significantly unless the minimum wage increases.

If you were to upgrade the units in an attempt to increase rents, it would not be effective. Individuals who can afford higher rents typically do not choose to live in distressed areas.

Inability to screen out bad tenants

The people who occupy multifamily homes in Las Vegas typically live cash-based lives. This means there is little financial history upon which to evaluate them for payment performance.

According to one property manager, any financial history they have is likely to be bad. The screening process for cash-based tenants: “If they have two pay stubs and enough cash to pay one month’s rent, they are in.”

Leases mean little to cash-based tenants

Minimum-wage workers tend to have few possessions, so if there is an issue, they put their possessions on the back of a pickup and go down the street to the next property.

So, Multifamily or Single-Family?

Should you buy multifamily over single-family? It depends on the tenant segment it attracts. The property type does not matter.

My first investment property was a multifamily in Houston. On paper, it was a cash cow. In reality, due to nonperforming tenants, evictions, damage, and other costs, I lost money every year. My cash cow was actually a money pit.

I next bought two fourplexes in a suburb of Atlanta. They performed well, and there were few issues.

The difference was the tenant segments the properties attracted. The Houston property was a C (D?) class with near-minimum-wage cash-based tenants. The Atlanta properties were B+ class, and the tenant segment was credit-based and earned significantly more than minimum wage.

Final Thoughts

The type of property is irrelevant. Choose one that attracts a tenant segment with a high concentration of reliable tenants. In Las Vegas, the properties that attract the tenant segment with the highest concentration of reliable people are single-family homes with specific characteristics.

Buy the type of property that helps you reach your financial goals. Don’t follow others’ opinions.

Find an Agent in Minutes

Match with an investor-friendly agent who can help you find, analyze, and close your next deal.

Ready to succeed in real estate investing? Create a free BiggerPockets account to learn about investment strategies; ask questions and get answers from our community of +2 million members; connect with investor-friendly agents; and so much more.

Note By BiggerPockets: These are opinions written by the author and do not necessarily represent the opinions of BiggerPockets.

Source link