6 Ways to Find Intrinsic Value in Real Estate

Michelangelo is one of history’s greatest sculptors. I never dreamed he could teach me so much about real estate investing. But he did.

Michelangelo said, “The sculpture is already complete within the marble block, before I start my work. It is already there; I just have to chisel away the superfluous material.”

When I first read this quote, I thought it was ridiculous. Was this some weird riddle?

But this is a powerful truth, and it deals with a variety of topics, including art, love, and real estate investing.

Take a block of stone. A machine operator carved it out of a quarry, along with hundreds of others that look the same. It’s a commodity with a price tag of probably a few hundred dollars.

Now put this block of marble in the hands of an artist. An artist who can envision what this piece of rock could be. Give them the right tools and some time, and the outcome might be magic.

The artist can envision the intrinsic value of the stone. And by bringing it to life, the sculptor can create a valuable piece of art with a value exponentially higher than a rock’s. It could even reach the “priceless” realm.

So, Paul, what does this have to do with real estate again?

Level up your investing

Imagine you’re friends with hundreds of real estate investors and entrepreneurs. Now imagine you can grab a beer with each of them and casually chat about failures, successes, motivations, and lessons learned. That’s what we’re aiming for with The BiggerPockets Podcast.

The current situation in real estate investing

This is a historically difficult time to acquire real estate. Demand is at an all-time high, interest rates hover near historic lows, and inflation is looming. The BiggerPockets community has taught and encouraged hundreds of thousands of investors to get into the game. But it’s not easy.

Some investors have been told to buy, even above sensible levels, because the price will always go up. Well, it might keep going up. But ask the millions who got burned in the Great Financial Crisis of 2008 how well that went. And ask Warren Buffett and other top investors who say this is folly.

Other investors are looking for value-add deals. I heartily applaud them. But most of the value has already been added to most of the assets most investors want to acquire. Why? It’s a result of the popularity of multifamily investing and this long-overheated market.

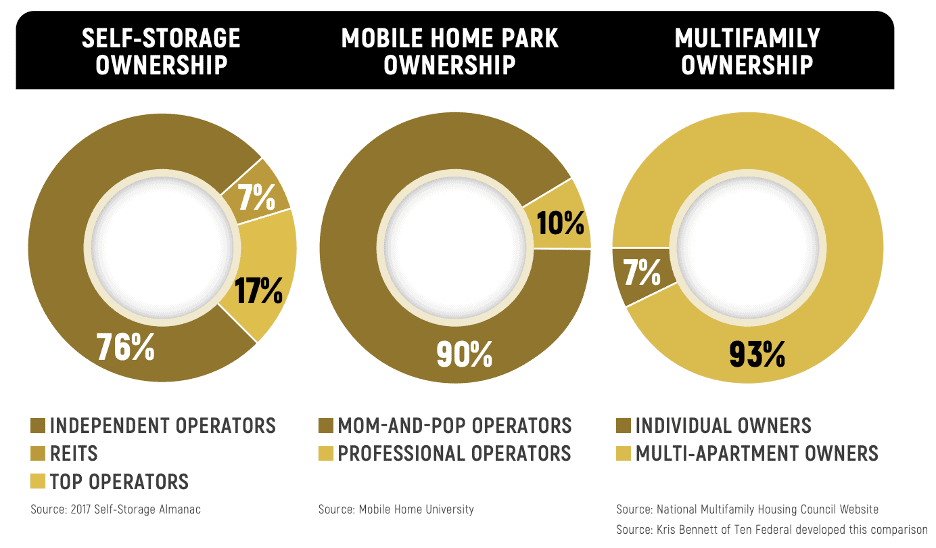

Fellow BiggerPockets investor Kris Bennett researched this situation in the multifamily realm. He concluded that about 93% of multifamily properties with 50+ units are owned by corporations that own multiple multifamily assets.

Not all of these are well-run. Not all have had the value wrung out of them. But my experience is that most of the value has been added. It is hard to find value-add opportunities in multifamily, and those coveted deals usually go to insiders.

Single-family homes are in a similar boat. It is tough to find good deals to fix and flip or rent out.

So, if we can’t make a profit by adding value, what are we to do?

Introducing the concept of “intrinsic value extraction”

For our discussion, let’s define extrinsic value as the sale price of an asset. The price at which you can acquire an asset. For our sculptor, this is the price of the block of marble.

And let’s define intrinsic value as the true potential value of the asset. This is the primarily hidden prospective value of the asset that can be achieved by a trained professional. This professional has both the ability to spot an asset with intrinsic potential and the skill to extract it.

I’m encouraging you to become that professional. Or link up with one.

I chose the latter. And I’m achieving the highest consistent profits of my 20+ years in real estate.

6 examples of extracting intrinsic value

I’m not going to dive deeper into the mechanics of intrinsic value extraction because the specifics vary significantly by asset class. Instead, I’m going to give you a handful of brief examples to raise your excitement level.

Upgrading self-storage

My firm invested in a self-storage facility acquired from a feuding group of Texas siblings for $2.4 million cash (extrinsic value) in March of 2019. After upgrading marketing and operations, the facility appraised at $4.6 million. The operator had obtained debt of $2 million, leaving only $400,000 equity in the deal. When the property sold for $4.6 million (intrinsic value) in late 2020, equity holders walked away with $2.6 million in cash.

Finding clever land uses

My son bought an 85-acre mountain parcel for $215,000 (extrinsic value). He sold the timber from it for $200,000 within a month. Within a few years, he will have the opportunity to carve it into about ten lots worth an average of $30,000 each. In the meantime, he can rent out hunting rights for at least $1,000 annually to cover his taxes, and he can potentially retain a long-term cell tower lease valued at $800 per month. After adding some value through surveys and soil tests, his intrinsic value is north of $600,000. (Can you tell I’m proud of my son?)

Flipping mobile home parks

My firm invested in a Midwestern mobile home park acquired at $7.1 million ($3.5 million equity and about $3.6 million debt) in early 2020. The owner hadn’t visited the park in over five years, and it was in decline. Our operating partner slashed bloated costs and improved the community. He passed utilities back to the tenants and modestly raised the extremely low rents. Within a year, the park was sold to a great operator who saw upside in filling around 50 vacant lots. The sale price was over $14 million, with an IRR of 347%.

Increasing gross rents

My real estate broker friend Eric Eickhof helps Minneapolis investors acquire seemingly overpriced homes near the university campus for around $400,000. Most investors turn up their noses on these homes that rent for $1,500 or so per month. But Eric coaches them to rent them for $700 per bed, often giving them gross rents of well over $4,000 per month.

Adding to the advertising budget

My friend Jerry paid $5 million ($1.7 million equity) to acquire a 125,000-square-foot warehouse with a $200,000 net operating income. He saw an opportunity to increase the value by implementing some basic business strategies. He spent $45,000 in advertising to fill vacancies and drive rents. He even charges the parking lot food truck $500 rent, which goes straight to the bottom line. The value is $7 million now, and his equity more than doubled.

Dividing and conquering

AJ Osborne, an innovative self-storage developer, acquired a Super Kmart in Reno for $6 million. He sold off the parking lot to an apartment developer for $2 million, leaving equity of $2.5 million plus debt in the deal. He cut the building in half and created a beautiful self-storage facility. With only 40% of the facility leased, he turned down an institutional investor’s $26 million offer.

There are other examples, too. One of my friends is trying to buy underpriced office space in DC to condo out to individual buyers. One is strategizing about converting malls to senior living. Another bought a residential home and converted it to commercial space. I bought a five-acre non-subdividable waterfront tract and got a variance to create a small subdivision.

Asset classes with the highest potential intrinsic value

I mentioned the challenges of finding multifamily and single-family properties with high intrinsic value potential. So, what asset types have the most substantial potential?

Some may believe that severely distressed asset types have the highest potential. Malls, retail, and hotels are certainly at low values now. But just buying an asset at a rock bottom price, even at a foreclosure sale, does not necessarily fit this model. It can, as in the example of the Kmart conversion to self-storage. But not always.

I would argue that the best places to find deals like this are in mom-and-pop-owned assets—property types with a severely fragmented ownership base and owners who don’t have the knowledge, desire, or resources to increase income and maximize value.

These owners have often owned their assets for a long time. And they are benefiting greatly from the compressed cap rates driving up the value of nearly all real estate assets.

My two favorites are self-storage and mobile home parks. I have discussed my reasoning on these asset types in a variety of previous articles. Here is a graphic comparing multifamily ownership to self-storage and mobile home parks. I want to thank BiggerPockets member Kris Bennett, who originally conceived this comparison for Ten Federal Storage.

Do I sound biased toward these asset classes? I probably do. I have entered my third decade in the real estate investment world, and as of now, these are the best asset types I’ve seen. But this could change tomorrow.

One thing that won’t change is my passion to invest in assets where the intrinsic value significantly exceeds the price. I hope you see the value in this powerful strategy.

Oh, and thank you, Michelangelo.

:215-447-7209

:215-447-7209 : deals(at)frankbuysphilly.com

: deals(at)frankbuysphilly.com