Will the 10-year yield send mortgage rates over 4%?

I have been a happy camper lately, particularly with the rise of the 10-year yield as I am seeking balance in the housing market. I love these times in the market and the San Francisco 49ers are making an epic run in the playoffs, so what else can a person ask for? Other people might not be as happy as I am. I retired in 2020 from the mortgage business after 24 years, so I understand how some people who were floating their rate lock might not feel this way.

Between the FOMC meeting and stock market volatility, there is a lot of angst about the market right now so I want to break down what’s happening with the 10-year yield and how that could affect mortgage rates. I am a bond market guy because, to the core, I am an economics person first, so my discussions are more about the 10-year yield and the economic cycle versus mortgage-backed securities.

Let’s look at my 2022 forecast based on the 10-year yield. “For 2022, my range for the 10-year yield is 0.62%-1.94%, similar to 2021. Accordingly, my upper-end range in mortgage rates is 3.375%-3.625%, and the lower-end range is 2.375%-2.50%. This is very similar to what I have done in the past, paying my respects to the downtrend in bond yields since 1981.”

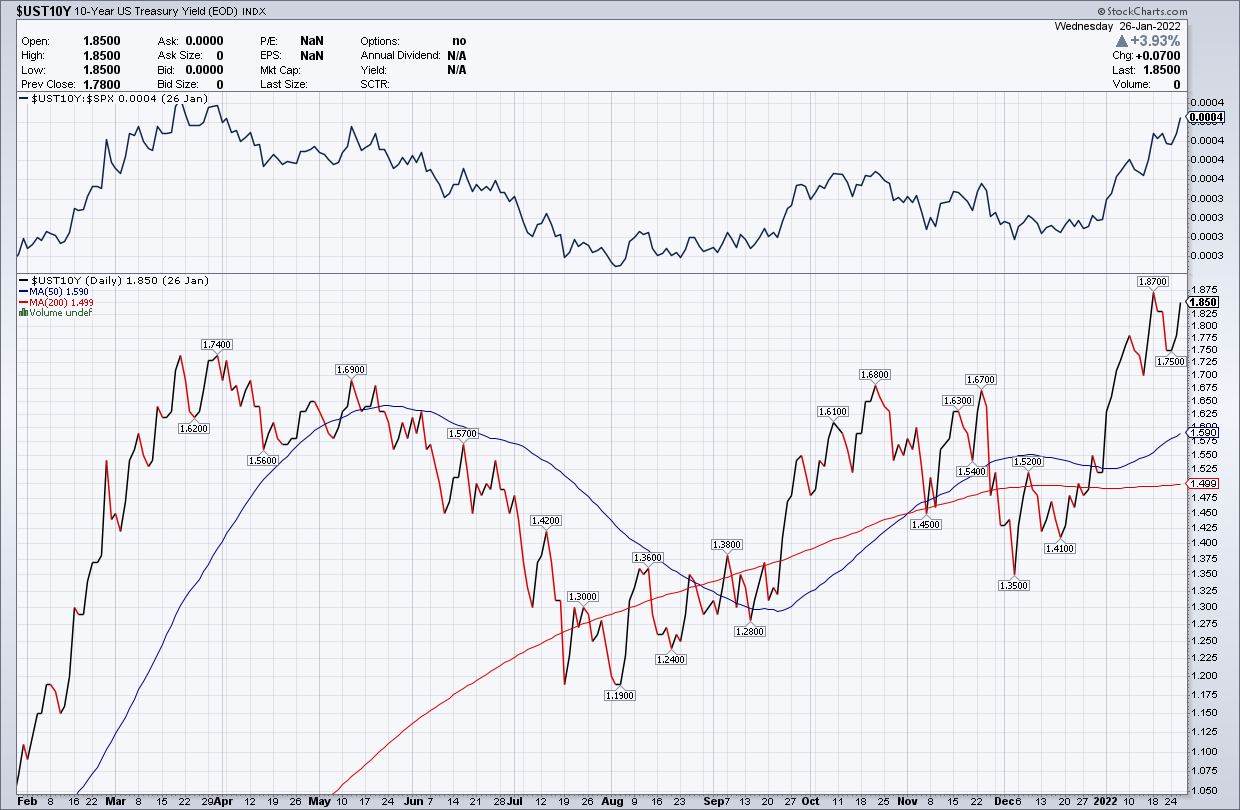

Today, as I write this article, the 10-year yield is at 1.793%. Yes, even with the hottest economic growth and inflation data in decades, the 10-year yield is still below 2%. I understand why people are confused by this because in the previous expansion when the 10-year yield was below 2%, people would be screaming that the bond market is saying we are going into recession. Some of our best economic growth and hotter inflation data have all come with the 10-year yield being in a range of 0.55% – 1.90%.

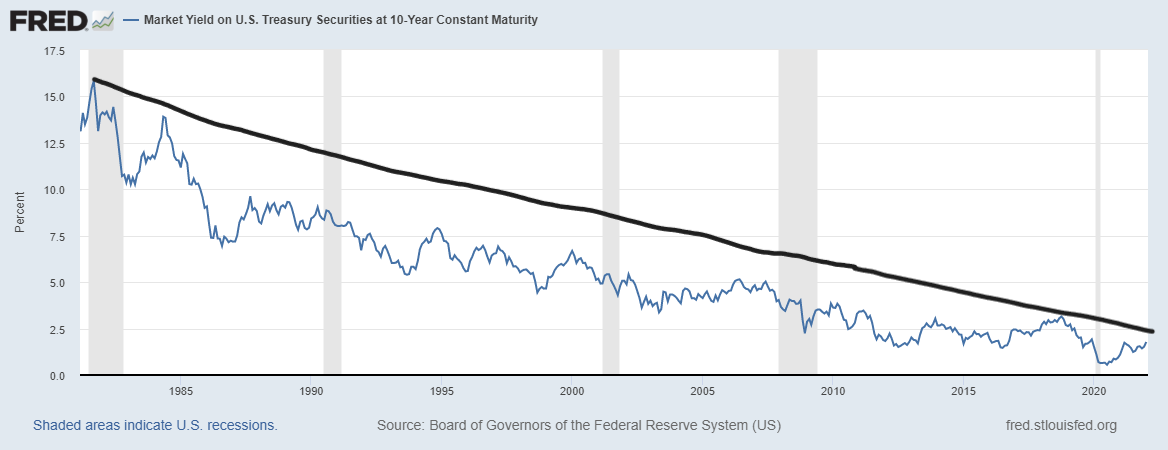

The simplest and easiest answer I can give you is that the trend is your friend, and the 10-year yield has been in a downtrend since 1981 and in some cases, I can make a case it’s been in a downtrend for thousands of years. Right now, we aren’t close yet to testing that long-term downtrend. The 10-year yield needs to break over 2.70% with conviction and duration to even have that conversation and we aren’t there yet. The chart below is instructive.

In the previous expansion, when I started to incorporate 10-year yield ranges as part of my forecast beginning in 2015, I always said the same thing up until it was apparent that COVID-19 was about to hit us: The 10-year yield would be in a range between 1.60%-3%. In 2018, we tested the higher-end range when the 10-year yield got to 3.25%.

I remember it well as everyone thought mortgage rates and the bond market were headed higher. At a conference that day, I was scolded that I didn’t know what I was talking about. Fifty economists surveyed by the Wall Street Journal all said rates would go higher, but my 2019 forecast spoke about a 10-year yield under 2%. This was based on the long-term downtrend not breaking, and I thought growth would slow, as it did.

Now on to the second portion of the 2022 forecast: “We had a few times in the previous cycle where the 10-year yield was below 1.60% and above 3%. Regarding 4% plus mortgage rates, I can make a case for higher yields, but this would require the world economies functioning all together in a world with no pandemic. For this scenario, Japan and Germany yields need to rise, which would push our 10-year yield toward 2.42% and get mortgage rates over 4%. Current conditions don’t support this.”

So much of my bond market take last year was about the 10-year yield creating a range between 1.33%-1.60%, even though the forecast range was between 0.62%-1.94%. The 1.33%-1.60% premise was a talking point of my America is Back recovery model which I wrote on April 7, 2020. We were able to establish a good period of time between 1.33%-1.60%.

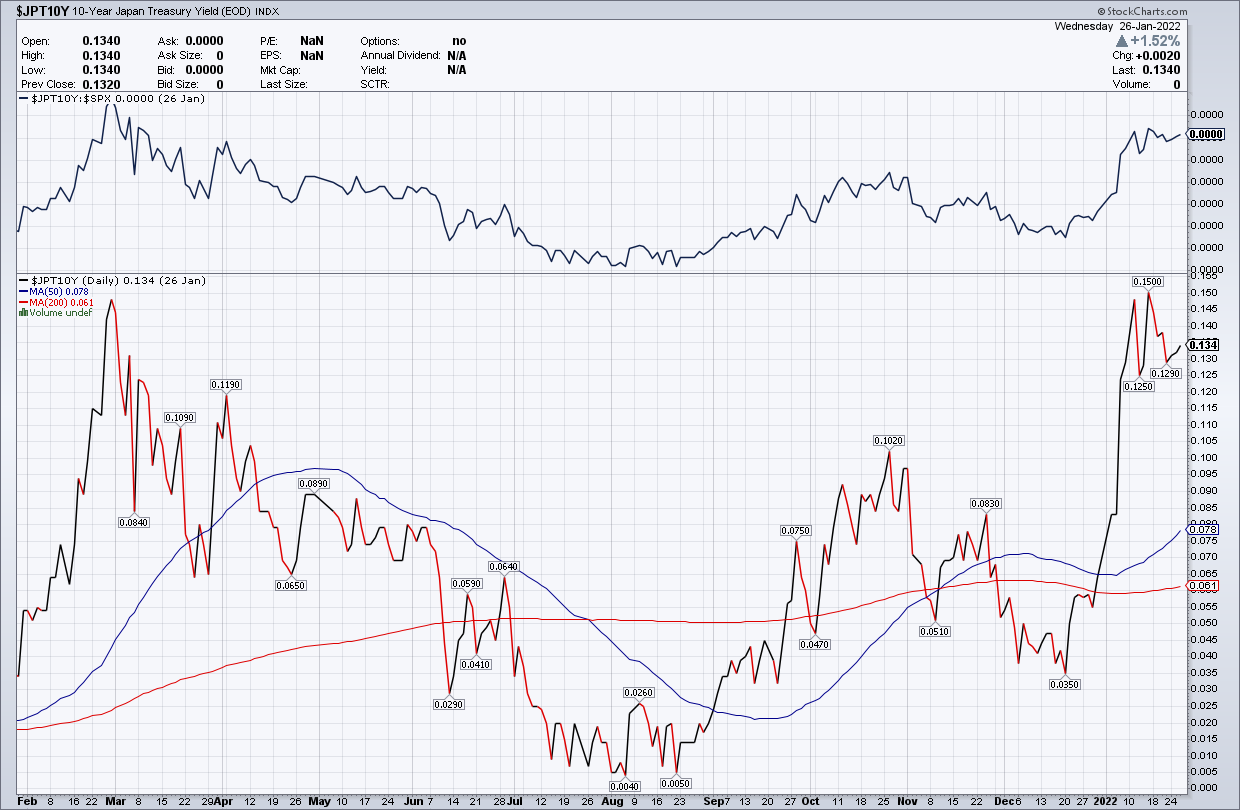

This year, I have said there is a way for the U.S. 10-year yield to get above 1.94%, but it needs help from global yields, particularly in Japan and Germany. As you can see in the charts below, the 10-year yields of both countries have been rising.

This premise that we need Germany and Japan yields to rise is working, but it’s simply not enough yet to get us over the hump. This 1.94% level is very personal to me because I talked about it so much before COVID-19 hit us. On Dec. 28, 2019, I wrote: “Currently, the 10-year yield is at 1.88%. For many months on social media sites, I have talked about how important it is for the bond market to close above 1.94% and get follow-through selling. A yield above 1.94% would mean that the bond market has more confidence that we will have higher growth next year. Until then, I would be skeptical of any story that predicts a higher rate of growth for 2020.”

At the time, COVID-19 wasn’t yet a pressing issue. The rest is history on what happened here and around the world.

I know it seems like a crazy time with stocks falling and bond yields rising. However, if you ignore the noise, everything still looks about right. If our 10-year yields had risen well over 1.94% (3.50% plus) due to inflation and Germany and Japan weren’t increasing, I would be having a different conversation today. However, that isn’t the case.

I understand some people’s confusion because inflation data should send yields much higher. However, that isn’t happening and economic growth is booming. But, the economy’s growth rate can’t sustain itself unless population growth takes off or productivity does. In time, things will moderate to a proper trend, and the supply shortage issues will be gone as demand gets back to normal and the world economies heal. What that means is that we will go back to being a country with slowing population growth in a world that has a lot of economies with slowing population growth.

Now the question is: can yields take mortgage rates over 4%? The key will be Germany and Japan, so keep watching their yields. The longer we go without our 10-year breaking over 1.94%, the higher the risk that the bond market will rally and send yields — and mortgage rates — lower. With housing inventory hitting fresh new all-time lows, sub-4% mortgage rates combined with sub-4% unemployment rates are not what I want to see heading into the spring home-buying season.

The post Will the 10-year yield send mortgage rates over 4%? appeared first on HousingWire.

:215-447-7209

:215-447-7209 : deals(at)frankbuysphilly.com

: deals(at)frankbuysphilly.com