How a transparent marketplace provides a proven path to benefit homeowners

Selling pre-foreclosure is often the best option for distressed homeowners who don’t qualify for any loss mitigation programs, but those homeowners are understandably hesitant to choose that option and often end up choosing it when time is running out.

That makes those homeowners susceptible to predatory behavior by some buyers operating in the pre-foreclosure marketplace, behavior that has been chronicled in several prominent, recent news stories.

Given this pre-foreclosure paradox, mortgage servicers and government policymakers are forced to walk a thin line: nudging distressed homeowners toward making a choice that’s in their best interest while also arming them with the knowledge and resources they need to be protected in the pre-foreclosure marketplace.

Walking that thin line is becoming increasingly important as more distressed sales are pushed up-funnel into the pre-foreclosure marketplace — a trend that began developing about 10 years ago and has accelerated in earnest over the last two years.

Pre-foreclosure momentum

“If you’re experiencing long-term financial hardship and cannot afford your monthly mortgage payments, selling your home may be the best option,” explains a US Bank video that walks this thin line. “Our goal is to help you avoid a foreclosure sale while protecting your credit score and preserving your equity.”

Even the Consumer Financial Protection Bureau (CFPB) has weighed in, with a January 2023 blog post titled “For many struggling mortgage borrowers with home equity, selling their home could be an alternative to foreclosure.”

In its first paragraph, the CFPB blog post encourages mortgage servicers to provide distressed homeowners with a nudge toward a pre-foreclosure sale.

“Servicers can remind homeowners that a traditional sale might be one option to avoid foreclosure. … And servicers may want to suggest homeowners contact a real estate agent if the distressed homeowner is considering selling their home.”

The pitfalls of pre-foreclosure

The CFPB blog post doesn’t touch on the potential for predatory behavior in the pre-foreclosure marketplace. Those dangers can be found in recent headlines from the New York Times and ProPublica.

A July 2022 article in The New York Times traces how one man’s New York city real estate empire was allegedly built through a practice called deed theft, often targeting homeowners facing foreclosure.

“(Prosecutors and homeowners) have accused him of fraud: offering to help homeowners facing foreclosure by arranging to pay off their mortgages, while actually tricking them into signing over their buildings at bargain-basement prices. In nearly every case, the mortgage was never paid, leaving the homeowner with no property but a pile of debt.”

A May 2023 ProPublica article details how the self-proclaimed “largest homebuyer in the United States” is training its franchises to target and sometimes take advantage of distressed homeowners who are in pain. One of those sources of pain is a “looming foreclosure.”

Myriad manifestations of fraudulent and predatory behavior emerged during the five-year slide in home prices following the 2008 crash. One prominent scheme involved unlicensed “short sale facilitators” charging upfront fees to distressed homeowners and often representing “straw buyers” with lowball offers. Ethical concerns even arose for licensed real estate agents who approached distressed homeowners to list properties even though those agents were also representing prospective buyers.

A growing pre-foreclosure market

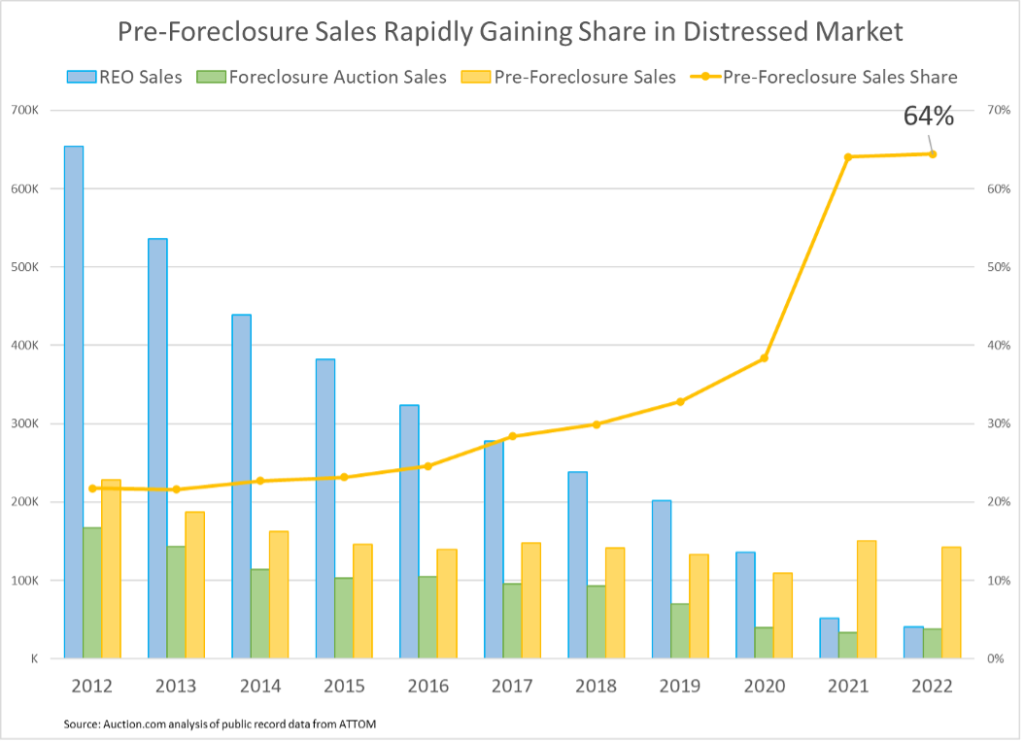

While it’s hard to quantify the prevalence of such predatory behavior, the opportunity for it is growing as the pre-foreclosure market grows. An Auction.com analysis of public record data from ATTOM Data Solutions found more than 150,000 pre-foreclosure sales nationwide in 2021, up 37% from 2020 to the highest level since 2014. Pre-foreclosure sales were defined as properties sold via an arms-length sale where a public foreclosure notice was filed prior to the sale, excluding foreclosure auction sales.

By comparison, only 33,000 properties were sold at foreclosure auction in 2021, the lowest level since 2003. That’s not too surprising given the pandemic-triggered nationwide foreclosure moratorium on government-backed mortgages (excluding vacant properties) that was in effect through the end of 2021.

But even after the foreclosure moratorium expired, pre-foreclosure sales continued to far outpace foreclosure auction sales. In 2022, there were nearly 142,000 pre-foreclosure sales compared to about 38,000 foreclosure auction sales and about 40,000 sales of bank-owned (REO) properties. That means pre-foreclosure sales accounted for 64% of all distressed property sales in 2022, the highest share on record.

Nudges from mortgage servicers are likely contributing to the growth in pre-foreclosure sales, but proactive marketing to distressed homeowners by prospective buyers is also a likely contributor.

“Our team tries to make every effort to purchase the properties on the front side,” said Mary Tritt, managing broker at Tritt Realty, a Carrollton, Georgia-based company that buys and renovates distressed properties. “When the (foreclosure auction) list comes out, us as well as other investors are trying to knock on the door, we’re trying to speak with those homeowners to see if there is anything that we can do to purchase the property before it actually goes to foreclosure.”

Tritt said her goal is to help the homeowner avoid foreclosure while also selling the property for “top dollar.” She will offer to list the home for sale on the MLS if there is enough time before the scheduled auction. But she noted that not all investors operate this way.

“Many times, we’ll find the sellers will try to sell their properties to an investor who’s come through and offered some too-good-to-be-true number only to find out that investor doesn’t have the money to purchase it and save the property before it goes to foreclosure auction,” she said. “So, we try to advise against that. Whether or not someone sells to us or to someone else, we’re just making sure that they truly understand the process and how to save the property or sell the property before it goes to auction.“

Price realization for pre-foreclosures

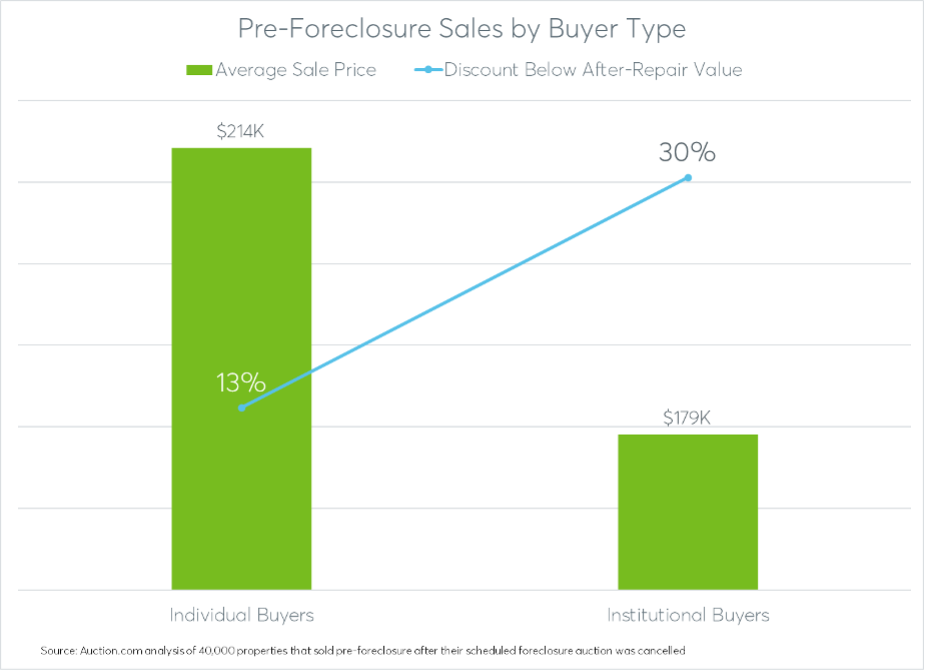

A deeper dive into pre-foreclosure sale data reveals that while many of these properties may have equity on paper, most are still selling well below their estimated after-repair market value. An analysis of more than 40,000 pre-foreclosure sales that occurred between 2018 and 2023 — after previously being scheduled for foreclosure auction on the Auction.com platform — shows the properties sold for 18% below their estimated after-repair market value on average.

While some discount below market value is to be expected with these properties — many are in distressed condition due to deferred maintenance — a look at the discount by buyer type indicates that some buyers are getting a bigger discount than others.

About one-third of the pre-foreclosure sales went to buyers identified in the public record data as institutions, including companies, corporations and limited liability companies. These institutional buyers purchased pre-foreclosure properties for 30% below estimated after-repair market value on average.

There are good reasons why institutional buyers might buy pre-foreclosure properties at a deeper discount. Institutional buyers are typically willing and able to take on more highly distressed properties in need of substantial renovation that an individual buyer may be hesitant to tackle. And institutional buyers can often provide more flexibility in terms of a graceful exit for the current occupant of a pre-foreclosure property.

Still, the opaque nature of the pre-foreclosure space may be enabling some institutional buyers to make off-market, lowball offers that distressed homeowners accept without listing the property in a transparent marketplace like the multiple listing service (MLS) or the robust foreclosure auction environment created by companies like Auction.com.

“Auction.com hinders my in-person auctions by advertising the available deals to the general public … (which) only drives up the price at auction,” wrote one buyer in response to a Auction.com survey sent out in March 2023.

Mary Tritt’s husband, Tony, has been investing in real estate in his local market west of Atlanta for more than 20 years. He’s seen the foreclosure auctions disrupted by transparent marketplaces like Auction.com, but recognizes that disruption is good for the market even if it may mean higher acquisition prices for him.

“Let’s face it, the auction industry, in general, has utilized online platforms to bring higher bidding on every widget imaginable. I’ve seen it firsthand play out in the housing market, specifically at non-judicial foreclosure sales and bank-owned REO auctions,” he said, adding that the disruption can also create efficiencies for his business. “An ideal scenario would be for all properties to land within the Auction.com platform, then I could cover more counties on foreclosure day, with far less labor!”

Democratized with transparency

Just as the previously opaque foreclosure auction marketplace has been democratized with transparency, inclusion and innovation over the past decade, so can the pre-foreclosure marketplace be democratized. The journey to a more transparent marketplace can start with mortgage servicers who go above and beyond simply suggesting a pre-foreclosure sale to distressed homeowners.

To help these vulnerable homeowners, servicers can provide them with a proven path to getting the highest and best offer for their home. In the distressed property world, that proven path involves some combination of listing the property for sale on the retail (MLS) marketplace and putting it up for auction on a competitive platform that is likely to receive multiple, competing bids from buyers who are experienced in dealing with distressed properties and distressed homeowners.

Local community developers like Mary and Tony Tritt understand that a more transparent pre-foreclosure marketplace will result in more competition from other buyers, but they also understand more competition will result in better outcomes for distressed homeowners and help winnow out bad players.

“While I realize that aggressive marketing of pre-foreclosures will inhibit our opportunities from both the pre-foreclosure perspective as well as at the foreclosure sale, I also recognize that the long-term health of our industry along with the specific outcomes for distressed owners will likely be markedly improved,” Tony said.

Proven pre-foreclosure path

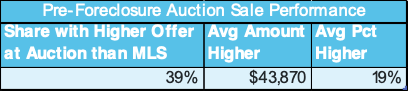

The dual-marketplace approach has produced optimal outcomes for both servicers and borrowers in a pre-foreclosure sale program created by Auction.com called the Market Validation Program (MVP). It allows servicers, in cooperation with distressed borrowers, to post properties on Auction.com that are also listed as short sales on the MLS.

While the MLS produced the highest and best offer about 60% of the time in MVP, nearly 40% of the properties got a higher offer from the Auction.com platform. And those higher offers were often substantially higher — an average of $44,000 (19%) above the MLS offer.

That’s likely the case for two reasons: first, not all properties are promptly listed on the MLS by the listing agent. The Auction.com data shows 47% of properties in the MVP program were not yet listed in the MLS when they were referred to Auction.com. The second likely reason for the higher auction offers: Some pre-foreclosure properties are a better fit for the local community developers using the Auction.com platform than the retail buyers dominant on the MLS.

“The last one I purchased was a short sale, which was a first for me with Auction.com,” said Karen Tyler, owner of Prodigy Realty in Virginia Beach, Viriginia, of an MVP purchase. “I didn’t even know it was a short sale listed on my own MLS because that particular property was not something I would look at for an investment property through the MLS. But if it’s an Auction.com property, I actually pay a little more attention to it.”

Uncovering hidden equity

Furthermore, 6% of the winning bids on Auction.com resulted in a full payoff of the mortgage in foreclosure. That means the property did not sell as a short sale as expected and the distressed homeowner was able to walk away with something to show for the equity uncovered by the power of dual transparency.

“Elated,” said homeowner Pam Mormino, whose home sold via the MVP program for $46,000 above the highest MLS offer and more than $40,000 above the total debt owed on the mortgage. “It really relieved so much stress on me.”

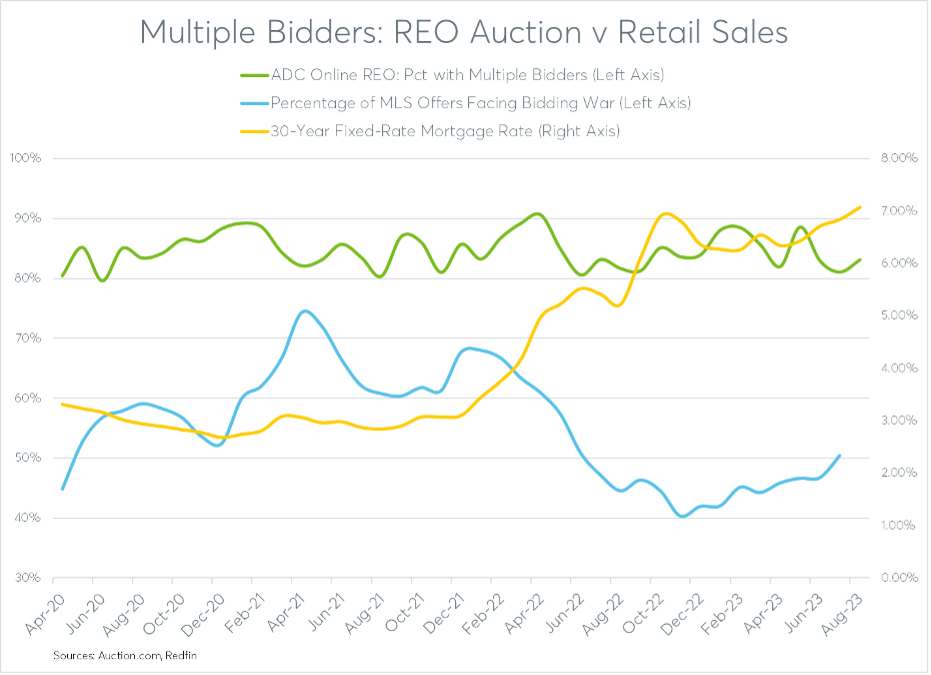

The higher offers on the Auction.com platform also stem from a more consistent level of competition in than in the retail, MLS marketplace. Competition in the retail marketplace tends to be more volatile, subject to market conditions such as rising mortgage rates. Over the past four years, 80 and 90% of all bank-owned (REO) auctions on Auction.com receive bids from multiple, competing bidders, while the share of MLS properties with multiple offers has ranged from as low as 40% to as high as 74%, according to an analysis of data from Redfin.

:215-447-7209

:215-447-7209 : deals(at)frankbuysphilly.com

: deals(at)frankbuysphilly.com