Housing demand rises as inventory falls

Housing demand is up and it’s time to track the spring housing data and see what the selling season will bring. As I always stress, we are working from the lowest bar ever with demand, so let’s add historical context to the data. But, even with mortgage rates higher this year than last year, demand is rising.

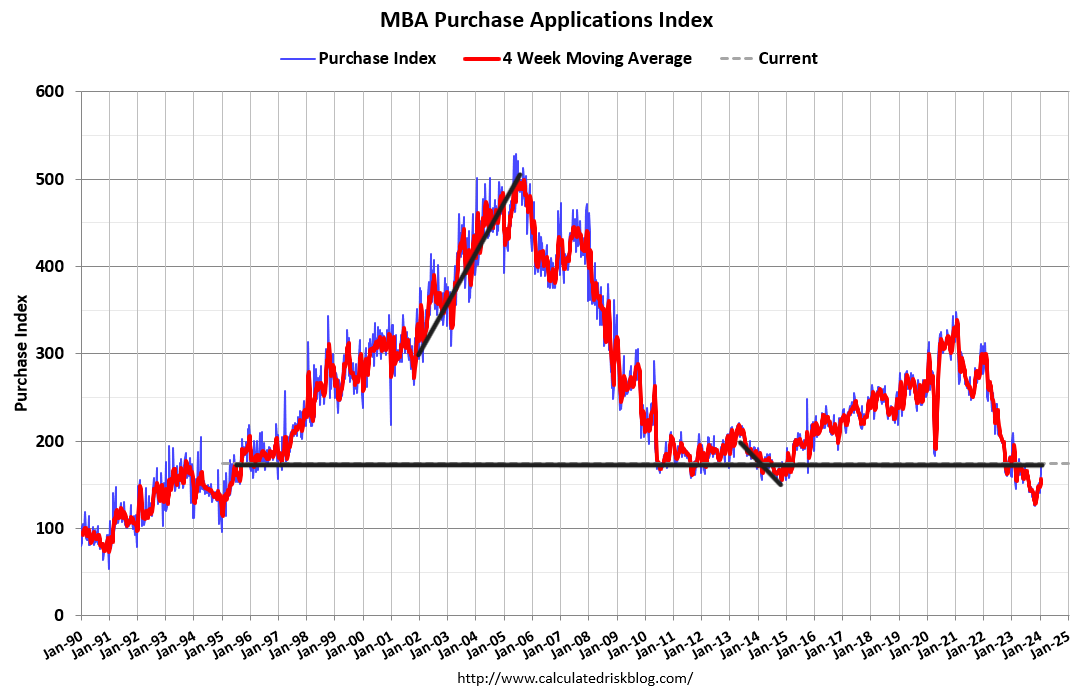

Purchase application data

As we get closer to the end of the first month of 2024, forward-looking purchase application data looks good. Once I make some holiday adjustments, we have eight weeks of a positive trend since mortgage rates fell from the 8% high, and as of now, the slightly higher rates we’ve seen recently haven’t impacted the data just yet. Historically, higher rates negatively impact the weekly purchase application data, and I will look for this over the next few weeks . But it’s very early in the seasonal demand timeframe for housing, so we will take it one week at a time. Purchase apps were up 8% week to week and still down 18% year over year. Last year at this time we got a boost in demand with rates heading toward 6%.

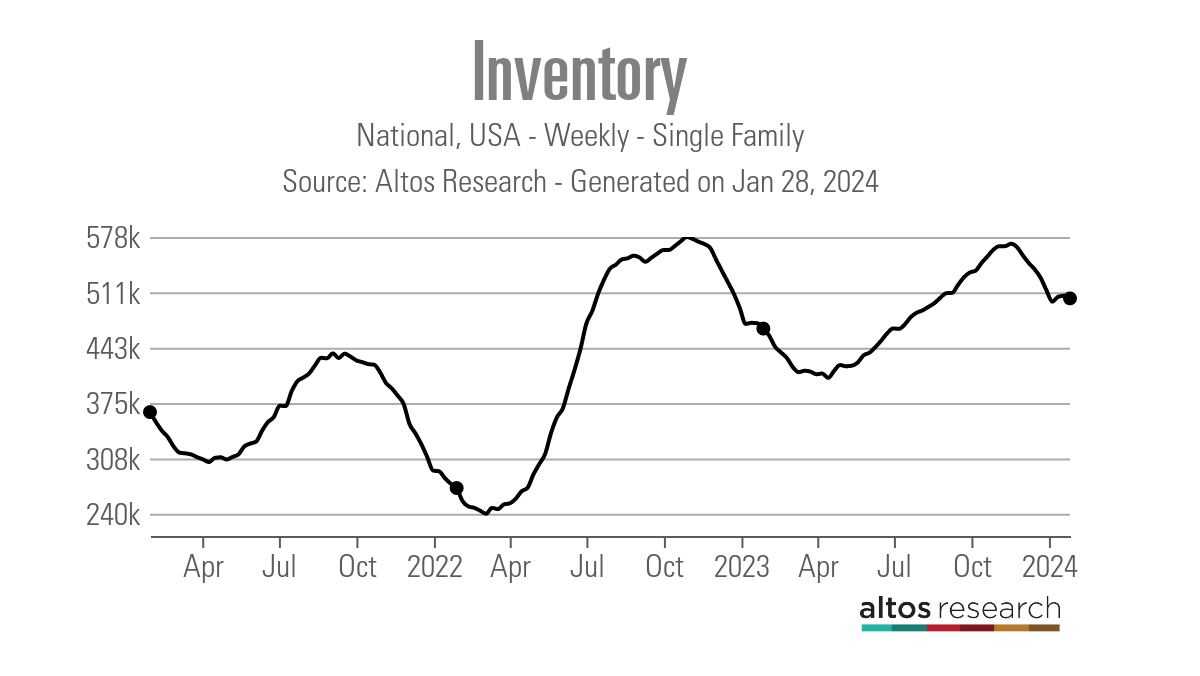

Weekly housing inventory data

Here is a look at last week:

- Weekly inventory change (Jan. 19-26): Inventory fell from 506,414 to 503,233

- Same week last year (Jan. 20-27): Inventory fell from 472,852 to 466,391

- The inventory bottom for 2022 was 240,194

- The inventory peak for 2023 is 569,898

- For context, active listings for this week in 2015 were 938,453

Last week, we saw active inventory fall slightly week to week. This is common in January. We have had some positive purchase application data recently, and the pending home sales report came in as a beat last week. So, inventory falling looks normal. However, I would like to see the inventory bottom very soon and have a more traditional seasonal increase, rather than having a bottom in March or April.

New listings data

One of the more positive stories about housing inventory recently is that we found a bottom in new listings data last year, and we have been starting to grow new listings data for some time now on a year-over-year basis. It isn’t anything significant, but I will take it after what we have been through the last few years. This is something I talked about on CNBC recently.

Weekly new listing data:

- 2024: 44,921

- 2023: 42,843

- 2022: 47,713

Price cut percentage

Every year, one-third of all homes take a price cut before selling — nothing abnormal about that. However, this data line accelerates higher when mortgage rates rise, and demand gets hit harder. A perfect example was in 2022: when housing inventory rose faster, the percentage of price cuts rose faster as home sales crashed. That increase matched the slope of the inventory increase, and people needed to cut prices to sell their homes.

Toward the end of 2022, that marketplace changed as home sales stopped crashing and the market stabilized. So far this year, the price cut percentage data is still on pace to break below the lows we saw in 2023 in the spring. This data line is very seasonal, so what is occurring now is very normal.

This is the price-cut percentage for the same week over the last few years:

- 2024: 31.%

- 2023: 34.%

- 2022: 20.%

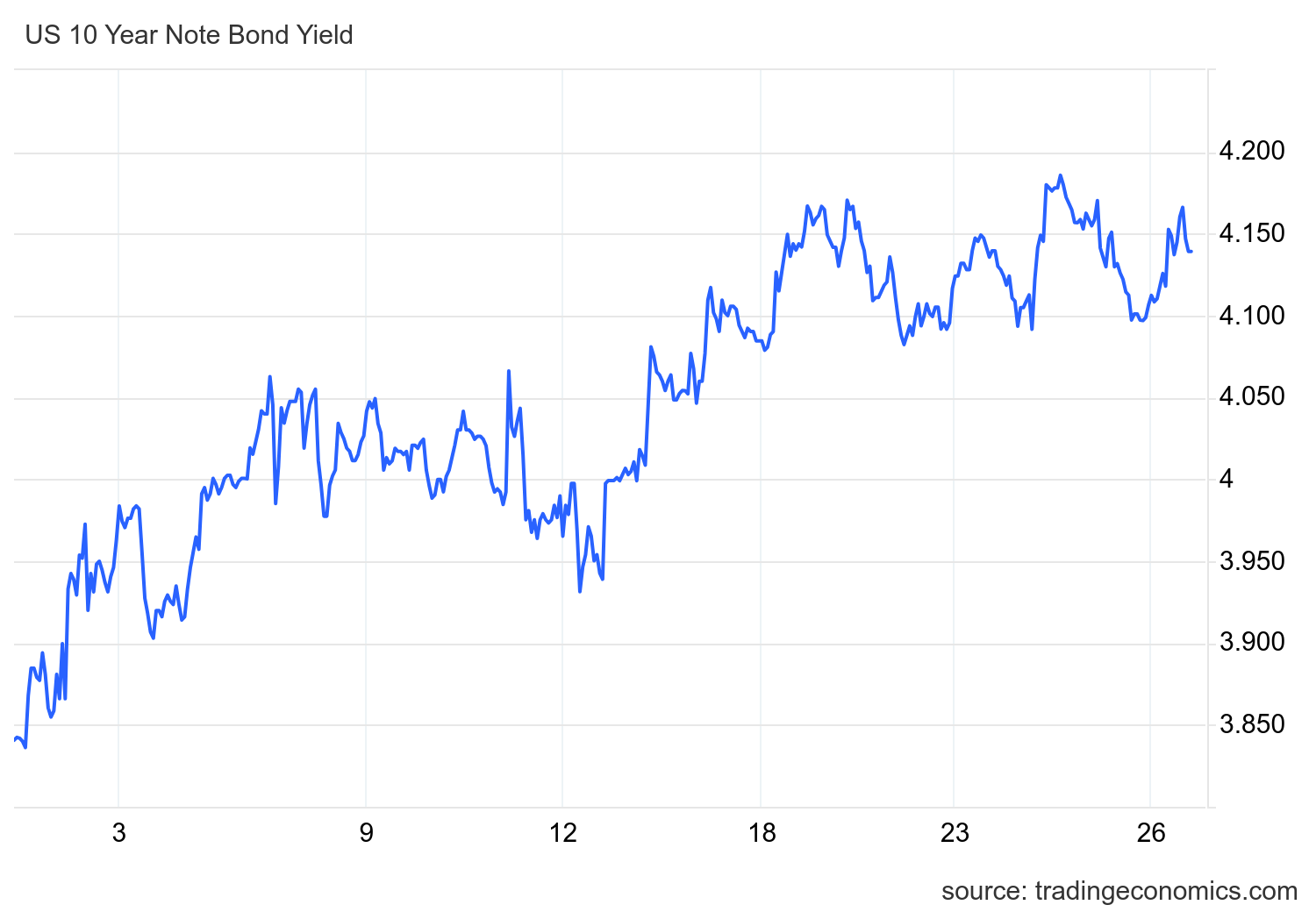

Mortgage rates and the 10-year yield

The 10-year yield is the key for housing in 2024. In my 2024 forecast, I have the 10-year yield range between 3.21%-4.25%, with a critical line in the sand at 3.37%. If the economic data stays firm, we shouldn’t break below 3.21%, but if the labor data gets weaker, that line in the sand — which I call the Gandalf line, as in “you shall not pass” — will be tested.

This 10-year yield range means mortgage rates between 5.75%-7.25%, but this assumes spreads are still bad. The spreads have been improving this year so much that if we hit 4.25% on the 10-year yield, we won’t see 7.25% in mortgage rates.

Last week, we got great news on inflation data, and we have been saying the inflation growth rate has slowed. However, in the economic game of rock-paper-scissors, it’s labor over inflation data, and the jobless claims data are too low, so the Fed hasn’t pivoted yet. Monday’s podcast will go over this topic more clearly.

The 10-year yield started last week at 4.14% and ended the week there. Mortgage rates ranged between 6.875% and 6.95%, ending the week at 6.90%. There is not much movement with the 10-year yield and mortgage rates. It’s wild to think that three to six month PCE inflation data is running below 2%, and mortgage rates are still this high. Remember, the Fed hasn’t pivoted and is still very restrictive.

The week ahead: Jobs, the Fed and home prices

It’s jobs week! So we will get the four labor reports: Job openings, ADP, jobless claims and the BLS jobs report. The Federal Reserve meets this week: we won’t see a rate cut this time but the key is the language they use in this meeting after the recent inflation data we saw. Also, the question and answers should be very interesting. We also have some home price data, which of course is a bit lagging from what is happening currently, but we will get those reports as well.

:215-447-7209

:215-447-7209 : deals(at)frankbuysphilly.com

: deals(at)frankbuysphilly.com