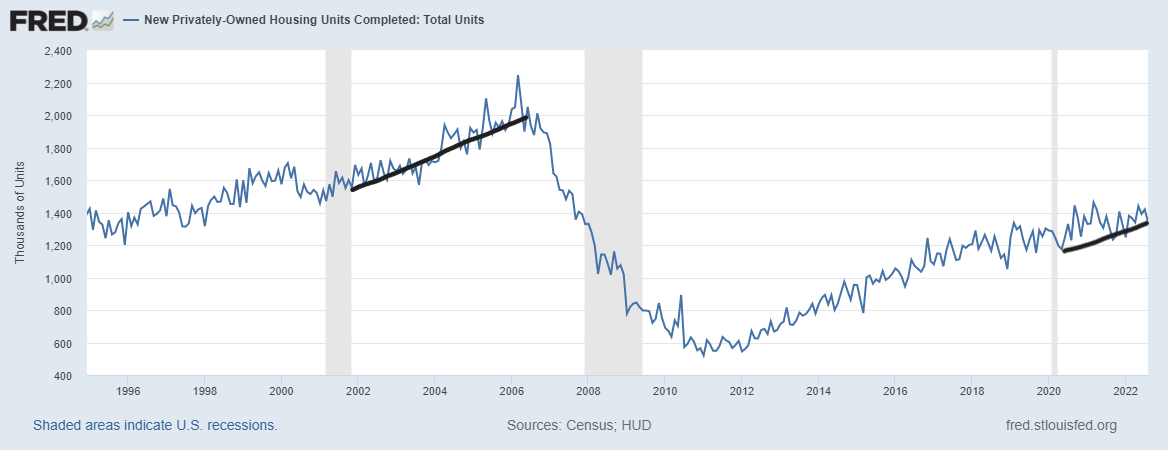

Housing completion data is now savagely unhealthy

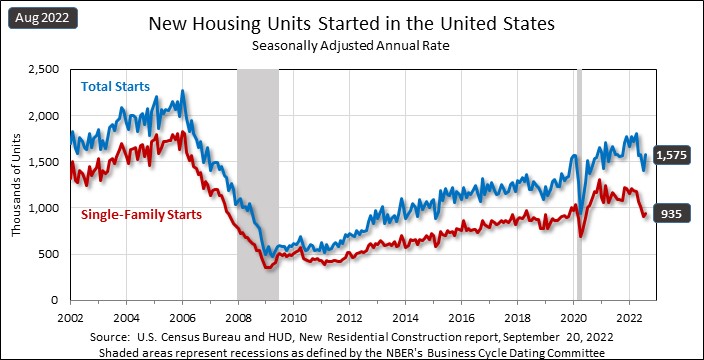

Housing construction in the U.S. during the brief COVID-19 recession, to that recovery, and now in the new housing recession, is going to go down in history as one of those crazy data lines we lived through. Just to give you some perspective here, at the peak of 2005, we had about 2.24 million housing completions in the monthly report. Today, even with over a decade of building growth, we are at 1.342 million.

The latest Census report shows that in August, privately owned housing completions were 5.4% below the revised July estimate of 1.419 million, but 3.1% above the August 2021 rate.

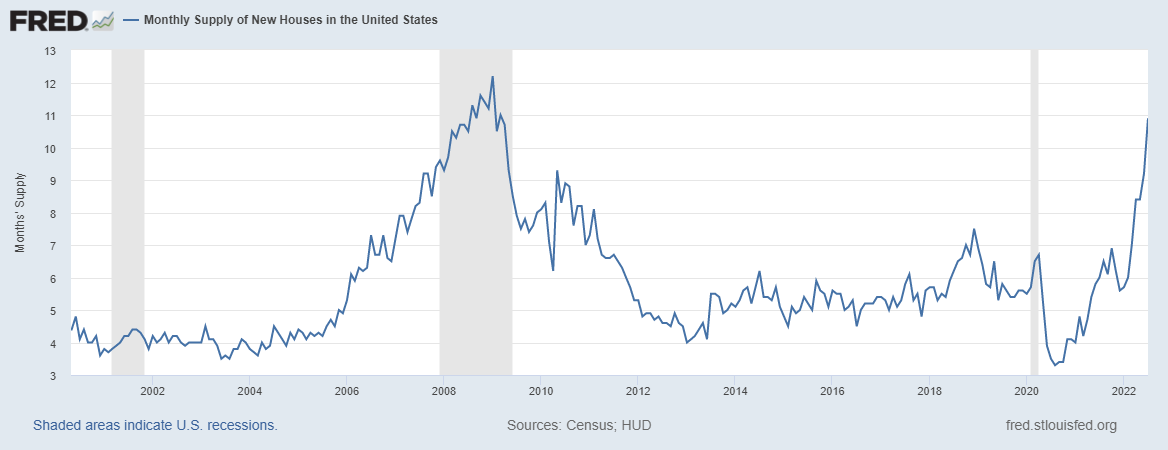

As you can see below, this chart speaks volumes, and trust me when I say this: the builders are going to take it nice and slow on completions until they know they can sell 9.84 months of homes they have under construction or have not even started yet.

Ladies and gentlemen, welcome to the savagely unhealthy housing market.

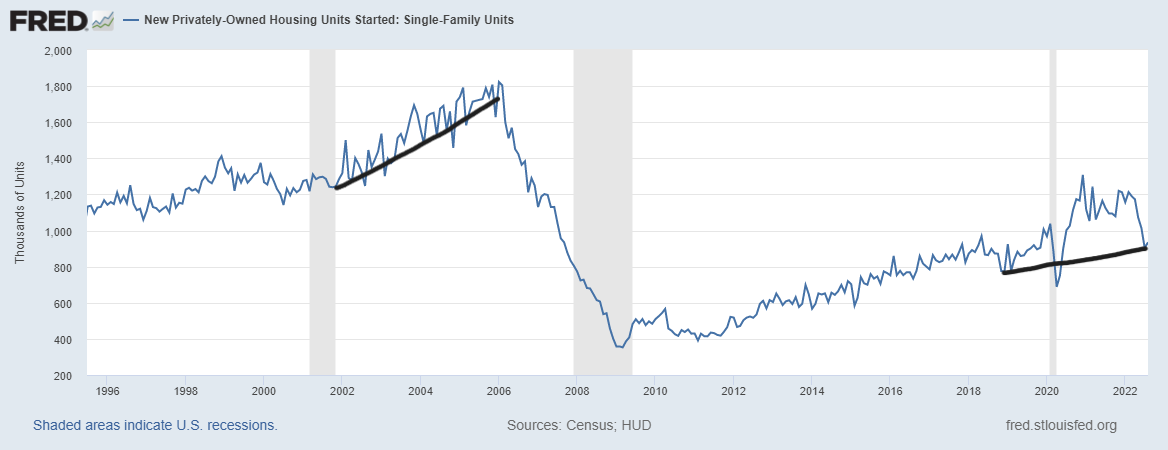

Now that mortgage rates have spiked up so much, the housing construction growth we have seen in single-family construction is done. It was a good run and we have legs to go lower in single-family construction until rates fall again.

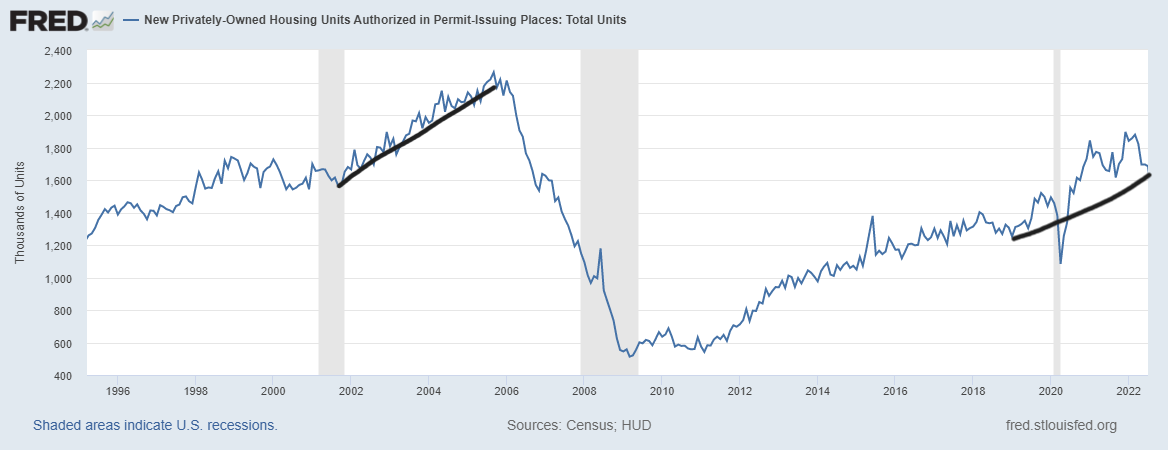

In this report, housing permits did fall, coming in 10% under the July level and 14.4% below the August 2021 level. This shouldn’t be shocking considering new home sales are falling and monthly supply has spiked for the builders. People have to remember that the builders are here to make money, not to build more homes for the existing home sales market. That market represents their biggest competition, and it’s an army they add to every time they sell a house. Since new homes are more expensive than existing homes, they have to manage their supply according to demand.

My rule of thumb for anticipating builder behavior is based on the three-month average of supply:

- When supply is 4.3 months and below, this is an excellent market for the builders.

- When supply is 4.4 to 6.4 months, this is just an OK market for the builders. They will build as long as new home sales are growing.

- The builders will pull back on construction when the supply is 6.5 months and above.

I will get more bullish on housing starts, permits, and completion data once the monthly supply data for new homes is below 6.5 months and new home sales are growing. We are clearly not there at all. Per the last report, we are standing at 10.9 months — and only 1.06 months of that supply is a finished product.

- 7.33 months of supply is under construction

- 2.51 months of supply hasn’t even been started yet

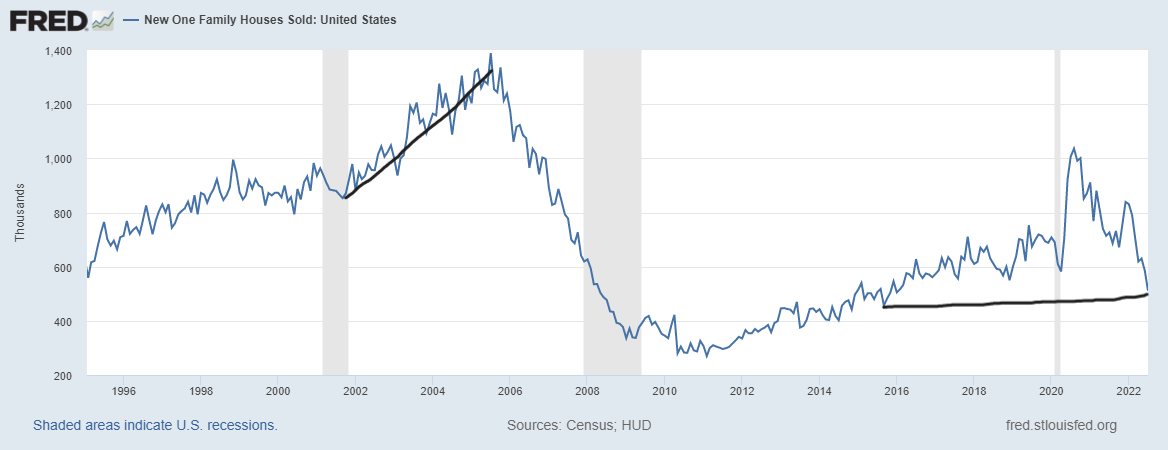

Another big difference between now and the peak of the housing bubble is that new home sales were roughly at 1.4 million at the peak, and now the last print is at 511,000. No sales credit boom, no major sales credit bust.

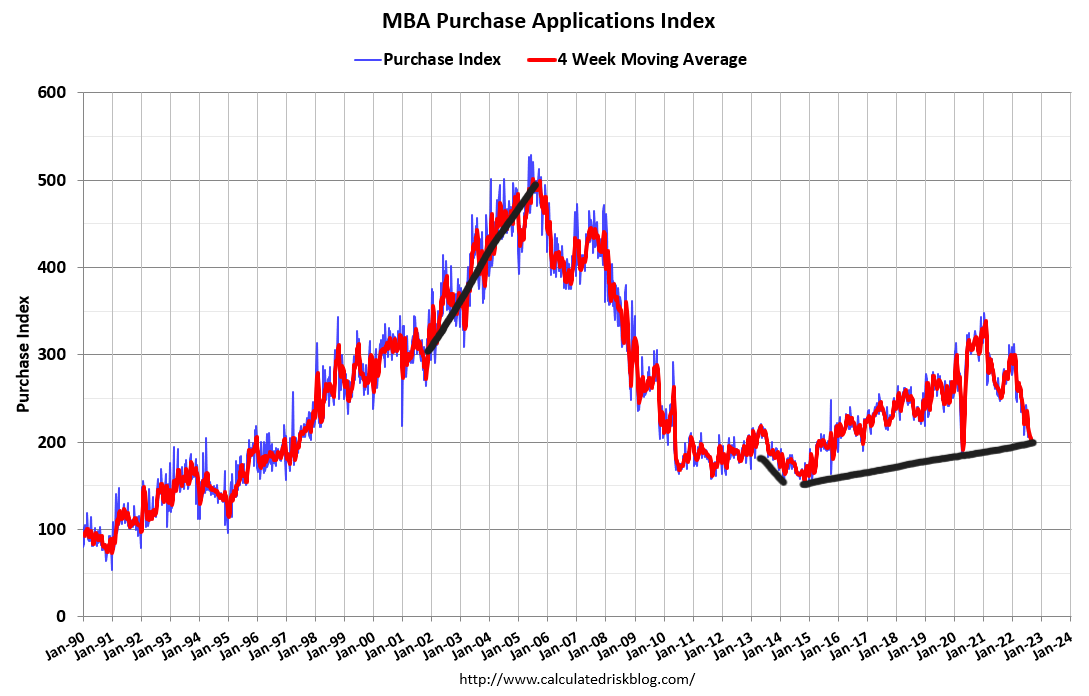

You can really see this in the purchase application data, which is already below 2008 levels today. During the housing bubble years, sales, starts, permits and completions data all moved together in a boom and then a bust. Not the case this time around as we haven’t seen the kind of booming sales market like we saw from 2002-2005.

Housing starts did pick up in this report, but revisions were negative. Again, the monthly reports can swing wildly, but the trend is always your friend. Multifamily construction has held up very well in 2022, while single-family weakness continues. We had a small pick-up in single starts coming off a negative revision print, so some context with that data line.

All in all, we should not be surprised at this housing starts report. As rates keep rising, more and more pressure will be added to the single-family starts data, which can fall a lot more as long as the builders are dealing with their excess supply.

Back in March of this year, when I wrote that the business model for the builders was at risk, this is what I meant. If they can’t sell their product at the prices they want, they will stop building single-family homes until they feel comfortable building again.

We had this happen in 2018: when rates got to 5%, monthly supply spiked above 6.5 months and the builders paused on construction for about 30 months. However, rates quickly fell in 2019 to stabilize the market place.

That isn’t the case here, as rates keep rising and are much higher than 5%. It’s a much different backdrop for housing, especially after the massive home-price gains since 2020. One thing is for sure, the savagely unhealthy housing market continues.

The post Housing completion data is now savagely unhealthy appeared first on HousingWire.

:215-447-7209

:215-447-7209 : deals(at)frankbuysphilly.com

: deals(at)frankbuysphilly.com