Dave Meyer:

Everyone, welcome to On the Market. I’m your host, Dave Meyer, joined by Henry, Jamil, James, and Kathy. How is everyone?

Jamil:

Great. Fabulouso.

Kathy:

Doing well.

Dave Meyer:

Good. Well, it’s good to have you all here. Jamil, we missed you while you were gone. It’s great to have you back.

Jamil:

Thank you.

Dave Meyer:

For everyone listening, we’re going to have two parts to this show today. We’re going to play a game called, Hot or Not, where our panelists are going to tell us whether they like certain strategies for this type of market, and then we’re going to go into what we call our correspondent show, where we’re going to be talking about some of the more important, and relevant news stories for real estate investors that are going on right now in February of 2023. Hey guys, ready to play Hot or Not? I feel like this could get mean. I feel like it’s like a middle school game. I have some repressed feelings about a game called Hot or Not.

Jamil:

A past trauma?

Henry:

Flashbacks of rejection.

Dave Meyer:

Yeah, just being notted a lot.

Jamil:

But is that website still up? Should we all put our pictures up on it?

Henry:

Absolutely not.

Dave Meyer:

I am on my work computer, and I’m not going to type in hotornot.com on my work computer.

Jamil:

Do they track keystrokes there on your work computer? Like what’s Dave typing today?

Henry:

Scott Trenches just watching you type all day.

Dave Meyer:

Yeah, sorry [inaudible 00:01:26] .

Jamil:

Although just to say I think if Dave was looking at Hot or Not, in my world, all that would appear would be sexy, or not sexy numbers.

Dave Meyer:

Oh yeah. Yeah.

Jamil:

It’d be like pie charts, versus line graphs.

Henry:

Look at that IRR. Mmm.

Dave Meyer:

It’s true. It’s just data visualizations, and people talking dirty about them. All right, well, enough of that. Let’s get on to our show, where we’re going to be talking about different strategies. I want to hear from each of you, is this strategy right now hot or not? And I guess it’s not like hot, like are people doing it? Is it, would you do it? So let’s start with short term rentals. Henry, hot or not?

Henry:

I’m going with nyet.

Dave Meyer:

Nyet? Okay.

Henry:

Not, not hot. I say that with a caveat. I’m doing it with a couple of deals, but I think what you’re starting to see with the Airbnb kind of slow down, both seasonality obviously is playing a role, but also the increased inventory of Airbnbs is causing demand to go down, which is causing pricing, nightly rates to come down.

And I think you saw a lot of people who had gotten into the Airbnb space because they were just like, “Oh, I can make five times what I’d get long-term rent. I just got to throw some furniture in there, and stick it up on Airbnb? Heck yeah.” Right? So, you’ve got a lot of people in this space who are truly running a business, who are truly looking at the metrics, and setting their properties apart, providing the amenities necessary in their particular regions.

They didn’t do that kind of market research. They’re not true operators. And so I think that if you look at Airbnb from that perspective, in 2023, you’re going to see a lot of those people who just kind of came in hoping to capture a bunch of cash, they’re going to fall to the wayside.

I still think buying properties at deep enough discounts that you can afford to pivot, and you can put those on Airbnb, I still think there’s some benefit there and you can make decent money with Airbnb. But, you have to operate it properly. Do the proper market research, offer the right amenities, have the right business practices in place, be able to do the proper marketing.

You didn’t have to market before, you just had to have it out there, and now you have to market, and set yourself apart. And so, it’s a more… I don’t even want to call it a more difficult strategy now. It’s what it should have been in the first place, is it’s a business, and you should treat it that way.

Jamil:

Hospitality.

Henry:

Yeah.

Jamil:

It’s hospitality. We got to get back to hospitality, right Henry? I mean let’s… There’s a Airbnb here in Phoenix, Arizona, it’s always booked because they have llamas.

Dave Meyer:

There. Everyone go out and get a llama, just go get a llama.

Kathy:

Llama. I never thought about it.

Dave Meyer:

Put a llama on it.

Kathy:

There’s one here that has a giraffe, so yeah.

Dave Meyer:

What? That seems illegal.

Kathy:

It’s a famous giraffe. It’s the one from…

Henry:

It’s the Toys “R” Us giraffe?

Kathy:

No.

Dave Meyer:

It’s Geoffrey? It’s Geoffrey.

Henry:

He retired from Toys “R” Us?

Kathy:

It’s the one from the Bachelor one, the Vegas one. What am I trying to say? The movie.

Henry:

The Hangover?

Kathy:

The Hangover. Yes, yeah, it’s the one from The Hangover. It’s that one. Yep. It’s a rescued giraffe from Hollywood.

Dave Meyer:

Honestly, you know what? I would stay there. I’m curious now. All right, so everyone, it’s short term rentals are hot if you have an obscure farm animal, but if you don’t, be very careful about it, is apparently the lesson. Does anyone else disagree? Anyone else want to give me hot or not for this? Jamil, it sounds like not? Kathy or James?

Jamil:

Yeah, not.

James:

Not.

Kathy:

Not. Not right now. I keep reading stories that actually it’s increasing now, and that vacation properties are kind of back in style, but I could tell you in our own case, we’re down 50% from last year, if not more.

Dave Meyer:

Same. Yeah, mine mine’s down a bit too, and I don’t know, I feel like it was a gold rush, and now it’s back to just grinding it out, like any other business. It’s not like the easy money any more like it once was. But maybe it’ll rise again. We’ll see. All right, let’s move on to buy and hold. Kathy, I’m just going to give you a layup right now.

Kathy:

Hot. So hot. So, so hot.

Jamil:

I mean, can anyone disagree with that?

James:

Yeah, I’m a, I’m going to disagree with that.

Dave Meyer:

You are?

James:

I’m a not on buy and hold.

Dave Meyer:

Really?

James:

But it depends on what you want to buy. Like the BRRRR properties I think are really hot. That’s a hard to buy. But for us, at least in our market, the lower income stable ones where you’re just putting 20% down, like a traditional rental property, and that’s kind of how I’m defining that the, you’re still competing against first time home buyers, and that market is competitive. Yes, the market’s down, but we’re moving stuff, and so it’s hard to get a good, stable, just buy and hold. And again, I’m classifying this as single family rentals. I think there’s a lot of multi family, a lot of BRRRR opportunities, but if you just want that straight base hit, single-family rental deal, not a good yield right now, I would get something else.

Dave Meyer:

Yeah, that’s interesting. So you’re saying basically you like rental properties, but it needs to have some sort of value add component.

James:

Yeah. It needs to have value add. I just don’t think the opportunities are there. If you want your base hit rental deal, 20% down, carpet, paint, release, the margins are not good. Not with the rates right now. And you have to put more money down, and I think you can get into buy and hold, but you got to get the ones that no one wants, or the ones that are a little bit hard, and then those deals are substantially better than they were 12 months ago. So there’s opportunities, and holdings, but just not for your straight base hit deals. This is thought… I think for me, you can get 3x your return in the other spaces.

Kathy:

It’s funny, I would’ve thought that, but I just had a conversation with our Indianapolis team at Real Wealth, and they said the cash flows today are the same that they were before, because rents have gone up so much in those areas, and now there’s more inventory.

Last year you couldn’t even get anything, and if you did you’d have to outbid other people. You’re not having to do that now, but the rents have gone up, and they’re holding. So he said it’s no different, and in so many cases the sellers are actually paying points to bring your rate down, and so you’re probably getting the same, if not better rate than you could get last year. So, I thought that was really interesting, and we had looked at the proforma, and tore it apart, and he was right. It’s similar.

Jamil:

Right now. I like buy and hold as a short term strategy. I know that kind of sounds crazy, but I think that if… Because I’m allergic to holding stuff, and I’m going to continue to be that way, because of past trauma, 2008, and getting my hand burnt when I was trying to buy a multi-family.

But what I’m going to say is, I am still seeing opportunities to buy really, really deeply discounted property out there, and if I can hold it just this period of time of pain where I think things start to stabilize, and once we come around the bend, if I can at least break even between my purchase, until my exit, which I think will be 18 to 24 months from now, I am looking for substantial returns on that. So, I just want to buy, hold. I don’t even care if I cash flow, just break even until I can take my exit, and cash in my chips at the casino.

Dave Meyer:

All right, so that’s like lukewarm, lukewarm, not hot or hot. It’s like-

Jamil:

Yeah. Yeah.

Dave Meyer:

Yeah. Okay.

Henry:

I mean, I agree. I think James and Kathy are both right, honestly. It’s similar to the Airbnb conversation. There was a gold rush when the market was super hot, and you could get 2% interest rates, and things were going up in value so quickly. So, you could buy something at a slight discount, and all of a sudden you’re renting it out, rents were going up, so you can make the cash flow work.

You’re not going to find those easy opportunities as much, the ones James was talking about. You’re not going to be able to make those pencil. But if you can, and are good at looking, and finding undermarket value deals, I mean, the discounts that we’re able to get, and then the rents that we’re able to get from, after we renovate those properties, man, we’re cash flowing just as much as we were before.

And a lot of the times it’s making more sense, because typically in my business, we keep the multis, and we sell the singles, but right now, the way we’re deeply getting the discounts on these singles, it makes more sense sometimes for me to just keep them as rentals, even if I do it in that short term timeframe, like Jamil is talking about, when I can sell them at more of a discount.

So even if it’s not something I want to keep in my portfolio forever and ever, the cash flow makes sense right now, because if I do turn those deals, like for example, I have a deal right now, I’m closing today, I’m going to make a $17,000 profit. It would’ve made more sense for me to just renovate it a little bit, stick a tenent in, and cash flow it every month until the market changed. So, the numbers are just making more sense as rentals on single families, depending on the type of discount you’re able to get, and how much you got to spend on that reno.

Dave Meyer:

For sure. All right, well let’s do one last one. Let’s talk about flipping here. James, hot or not?

James:

I think it’s hot. If you find the right opportunities, but it has to be ones that… Where we’re having success in flips right now is going in the spaces that everyone’s freaked out by. There is a lot of opportunities in there. When we’re buying an average price of seven to 950,000, the discounts are about 15% cheaper than the flips that we’re looking that are 300 to 500 on the acquisition.

And so, it can be hot if you get into the right space. I think the overall investor demand is that the not right now. No one’s really looking for flips, which is another good thing for us. We can go find those opportunities that are there. I mean, I just bought a house, we contracted it yesterday. I would’ve paid 600 for this at the beginning of the year, or at the beginning of 2022. We just contracted over 435.

Jamil:

[inaudible 00:12:08].

Henry:

Wow.

James:

And not only can I flip it, I can also build a daddy with a backyard.

Dave Meyer:

Oh, nice.

James:

But because it was a full permit job and it’s going to be a 12 month project, everyone’s like, “Nah, I don’t want to deal with this right now.” So, the margins have… Starting to really increase on the ones that are tougher. So if you can hang in there, and actually go after… Go where no one else is going, and you can absolutely crush it right now.

Dave Meyer:

Anyone else have thoughts, hot or not, on flipping?

Kathy:

I would’ve said not hot, but James is so hot that it’s making flipping sound hotter. But he makes a really good point that, I mean really, I wasn’t flipping when it was super hot for everybody, because I’m just not good at it, but maybe it’s time to start. But there’s a lot of belief that rates are going to go down in May, because the inflation numbers are going to look so much better year over year, and the average is year over year, and that may is really the month that that’s going to happen. And so, if you were to get something now and try to sell it in May, that could be really good timing, now that you mention it. It makes a lot of sense if you get it now with the discount, and then resell when mortgage rates are better.

Jamil:

Personally, of course I flip houses on TV, and so A, I have to for a part of my life, but secondly, the price point really matters. And for me, I’m staying away from the luxury, or, I’m not super luxury, but that between 750 and 1.5 million kind of price point, I’m staying away from flipping anything in that range. I’m really liking manufactured homes. I’m really liking really, really, really, really entry level fix and flips with minimal repairs, that that product is still moving. It’s profitable, and as long as you can acquire at a good price, it’s safe.

Dave Meyer:

All right. Hot. Enough said. Flipping is hot.

Henry:

Yep. I got two deals. I got two deals I’m going to net six figures on at flips right now, in this crazy market.

Dave Meyer:

Nice.

Henry:

And we’re talking six figures in Arkansas, so the margin is… That’s huge for here.

James:

Yeah. What kind of cash on cash return is that? Is that like two, 5000%?

Henry:

Yeah, well, I literally have no money in either one of the deals, so it’s infinite for me.

Kathy:

Smoking hot.

Dave Meyer:

James, those are the type of numbers I look at on hotornot.com, just those types of IRRs. All right, well we’re going to take a quick break, but then we will come back with our correspondence show.

Okay. Serious time everyone. All right, that was fun. Now, let’s talk about the news. James, you have a story for us about how the housing market is performing. Can you share something with us?

James:

Yeah, so this article is from Fortune Magazine, and it says, “Well, we are in a bifurcated housing market correction. Just look at these four charts,” was the title, and what it references a lot. It talks about how John Burns, which is a great data source in general, was predicting at the beginning of the year, a big decline, versus what they were saying at Zillow, where Zillow was actually predicting a 24% increase this year, year over year.

And John Burns came out pretty negative at the beginning of the year, thinking that there was going to be a fairly big decline, and it turns out he was not wrong in a lot of the major cities, and what it looked like was, in the top 150 major housing markets, 100 of them declined pretty drastically. San Francisco was down 10.5%, Austin’s down 9.5%, Reno’s down 9.3%, et cetera. And then there was 50 that were really just flat.

And what it comes down to, we’ve all been talking about it for the last couple months, is just the affordability in the market, and the markets that have been the biggest decline also had the furthest appreciation, but they were already at the top of the market going into this last… Like in 2018, things were at the top, and people were hitting their affordability. Once rates dropped so low, it spiked everything up again. But once those rates started increasing, it just had to get back down to the affordability.

And so, it really talks about how they believe that rates are going to continue to increase for next year, and that you need to watch, in these… As you’re investing, or how I read it is how you’re investing, you can look at the markets, and where their affordability ranges are, and that has a huge, huge impact on whether that market’s actually going to decline.

It’s not about that fad of a market anymore, or like… Some of the novelty in the markets have worn off, and it’s really just comes down to straight affordable. Can the buyer pay this with what income that they’re making? And so, as a flipper, or an investor, how I kind of read that is we think rates are going to go up, then yes, we could see further decline, like in Seattle. Seattle was a big drop.

I know in Jamil’s market too, in Phoenix, we saw a big drop, and it all had to come in with that top end of the market. And so, if you think rates and affordability are going to continue to climb, that those could actually deflate even further. But, it is talking about how it really just made two different markets. You have your affordable markets, and your expensive markets, and the affordable markets have seen very, very little, to zero decline. Like in Charleston, they were saying, has saw zero, and the expensive markets are deflating down.

And I did think that was the interesting point. Yeah, it comes down to affordability, got two markets, and I actually think there is going to be a third market though. It’s not just going to be two. I think you’re going to have your affordable markets, like tech, and that’s what we’re seeing right now. Seattle, San Francisco, Austin, the markets have deflated about 10% from last year, and I’m seeing it about 25% down from peak pricing.

But now we’ve kind of hit this affordable market, and we’ve sold a ton of houses in the last 10 days. I was running about 35 to 40% pending on all of our… At any given time we have about 60 to 70 listings. We were running about 35 to 40% pending for the last six months, and now we are up to 55 to 65% pending, and I’m getting offers regularly on all product, not just affordable.

We listed our farmhouse flip for $3.25 million. We were anticipating to be on at 60 days. We got an offer in 10 days. And so, things are moving again. So, as a flipper, I’m going, “Okay, well if the rates are going to spike up, I just need to undercut my values a little bit.” But there is this sweet spot where things are trading, and it also leads to big opportunities in these deflated markets.

Because what this is saying, is it’s all based on affordability, if we all think rates are… I think rates are going to drop in the late quarter, that means I’m going to see some appreciation there, too. And that’s what you can check for to get those massive equity pops, and really change your whole trajectory in real estate, for me. So I’m looking for those opportunities that I’m going to see those equity pops, because it makes it kind of more of an equation. Like, “All right, if we know where it’s going to sell on the affordability factor, then we just got to watch rates, and we can run with the rates, and kind of watch those equity positions rise or shrink.”

Dave Meyer:

Are you saying, James, that you think it’s picking up in Seattle because prices have fallen so far that they’re now affordable again?

James:

Yeah, it just got out of reach for people, because there’s still a ton of buyers in our market. We listed a couple homes last week, or we have a listing coming up right now in Mount Lake Terrace. Mount Lake Terrace is… So it’s north of Seattle, good commuter city. We saw massive appreciation in this neighborhood the last two years. I’m talking about 50, 60% appreciation. Huge, because just location, development, and the city also being improved.

And it definitely shrunk about 10% from where it was in the peak, but I pulled up, or [inaudible 00:20:34] get into list, there isn’t one home for sale in the entire city of Mount Lake Terrace that I saw that would be… So I’m going to be the only house for sale.

Dave Meyer:

Whoa.

James:

And what happened is, there was a lot more inventory in the wintertime, which I do think the seasonal slowdowns are coming back. Seasonal slowdowns were always a real thing, until COVID hit. Wintertime, you’re always going to sell your… It is going to take longer to sell, it’s going to sell for a little bit less. And then with rates increasing, it got the inventory increased more. But I mean, we’re talking about, their inventory increased like 35, 40% in these areas, if not up to 80%, and it got absorbed in the last two weeks, very, very quickly.

And we’re actually starting to see some multiple offers again too, where things are getting actually bid up, as well. So, I feel like it had this sudden drop, we’re on the shelf, and now the consumers are… They have to buy it. There is so many buyers in our market, they just can’t get in reach with what’s coming to market. And now, with the pricing getting down to that sweet spot, things are getting consumed again. I mean, there is a substantial amount of buyers in our market, even with the high rates, and no inventory.

Dave Meyer:

Wow. Super interesting. Yeah, I’ve heard a lot of that. I was just talking to my real estate agent in Denver who was saying something similar, and I guess Seattle and Denver are probably those types of tech markets. What you were talking about, that tier of tech markets that are high priced, and have seen some of the furthest drops, peak to current, so far. Jamil, given you’re in a pretty pricey market there, what’s going on with you in Phoenix?

Jamil:

Well, we had a very seismic type report by the New York Post, where Goldman Sachs predicted a 2008 style crash in Phoenix, Austin, San Diego and San Jose, and they’re predicting 27% or greater price decline for 2023. So, this obviously created just a massive ripple effect of conversations amongst the investor community, and real estate agents, and whatnot. So, my phone was blowing up, and so of course I start doing some digging, and looking at how true is this prediction.

And looking at the corrections, of course, each of these markets have seen declines, and what I’ve seen so far, from peak to present, we’re looking at about a 9.9% peak to present drop in Phoenix, Arizona, San Jose. And again, data is varying between different sources, but it’s all relatively close, from in San Jose I’m seeing about 8.9% peak to present, San Diego, 6.7% peak to peak to present decline, and in Austin, 14% peak to present decline, which is… I mean that, to me, if I’m looking at a possible market that could have that type of depression, or that type of crash, it could potentially be Austin.

But again, the fundamentals in each of these markets are really strong, and you still have very, very strong lending criteria. Days on market on average is like 30 days, or less in each of these markets. You’re also seeing these surges in first time landlords, which is an increasing thing, which is an interesting thing to think about, because people who have cheap debt in these markets, rather than just go and throw their house on the market, and sell it at a steep discount, they’re deciding to turn into landlords, and they’re going to hold that house, and keep that cheap debt, and possibly remove that from creating inventory increases.

The other interesting piece, because I have KeyGlee in my world, we’re in one of the nation’s largest wholesale operations, and I’m looking at buying, and what the institutional buyers are doing, and it’s just interesting timing that we see a report like that come out, and the institutions that we’re working with are all turning up, they’re buying in those markets.

And then when I say turning up, I mean they’re reaching back out to us. They’re emailing saying, “Hey, send us everything,” but our buy boxes have changed dramatically. So now, they are decreasing substantially where their offer number would’ve been. And so, it’s like they’re looking at a report like that as their justification for coming in, and trying to purchase that 25% below where they would’ve been purchasing, say, three or four months ago.

So it’s like this, is report creating movement which will actually fulfill the prophecy that this situation could potentially occur? So, that’s interesting. But, on the other side of that, after the holiday season, we looked at our pendings, just here in Phoenix, Arizona, and I mean, it’s spiked, just like James was reporting, in the last little while his flips, he’s at what, 50 or 60% pending, where normally he’d be at like 35, 40% pending.

We’re seeing something very similar here in Phoenix, Arizona as well. So, how does that happen? How is a 30% decline supposed to occur, when we still have low inventory, when building has screeched to a halt, when we’ve got home locked buyers, because interest rates were low for all that time, and they do not want to let go of that asset?

I mean, I don’t know. I don’t see it. I don’t see it. I don’t see it naturally happening. But again, everything that we’re looking at, and working with right now, are not natural real estate cycle phenomenon. This is all manipulation. It’s all so many different factors, and agencies, and institutions, and doing things. I’m not a conspiracy theorist, I’m just looking at the writing on the wall and I’m like, “Who’s controlling? Who is the puppet master here, and how do I become friends with that person?”

Kathy:

I could tell you one of the puppet masters is the one we’ve been talking about for a year now, and it’s the Fed, and what they’ve been doing. And this isn’t my article, but it’s an article that’s really good, and I’ll just share it really quickly. It’s from National Association of Home Builders, and I think you guys also saw this, how many households were priced out by higher mortgage rates in 2022.

And it shows these graphs of when interest rates went from 3.25%, to percent to 7% in a matter of months. I mean, what a shock to the system. This is doubling the payment in just a matter of months. And in that process, it went from 44 million people who could afford to buy a home, down to 26 million in a matter of months. We’re talking 15 million people priced out, boom, just like that, in a matter of months. I’ve never seen anything like it.

Now, recently, we went from that 7% rate down to about 6.4%. So this article is basically saying in the last few months that brought 2.6 million people back into the market. Now, as over the next few months, most people are assuming, and seeing that with inflation going down, so will mortgage rates, mortgage rates follow inflation, and that we will probably get into the high fives. And that brings in a whopping almost 8 million more people who can afford to buy.

So, a lot of what, again, James was saying earlier, and what you are saying now, Jamil, of like there’s this change, it’s because now there’s more people who can come back in, and they’re learning, and they’re being educated by their mortgage broker that, “Hey, you’re going to pay a little bit more to get your rate down maybe to the fives, maybe a point or two.”

I just talked to a mortgage lender yesterday who said, “It’s just like a point or so to get you into the fives.” And again, that’s bringing in 8 million more people, and paying that one point is a lot less than the higher prices that they were paying before. And you have a lot of people who are sitting on cash, ready to buy, and suddenly couldn’t, but had the down payment. So, it’ll be a lower down payment, but the difference goes towards paying down the rate. So, that may be one of the reasons you’re seeing more people coming back in, and sales picking up.

Dave Meyer:

And people are coming in with FOMO. They missed the opportunity.

Kathy:

Yeah.

Dave Meyer:

Because rates spiked, and now they’re back in it, and they are moving right now. They are really jumping on stuff. They don’t want to get priced back out again.

Kathy:

Yeah.

Dave Meyer:

When you put it that way, Kathy, it’s pretty amazing. The housing market has been as resilient as it is.

Kathy:

Yeah.

Dave Meyer:

The fact that we’re seeing, I think the Kay Schiller came out the other day, in a seasonally adjusted manner. It’s just 2.5%, peak to trough, to peak to current is 2.5% declines, and that’s with what, 30% of buyers being priced out? It is pretty remarkable, and I think why, to your point, Jamil, 30% declines. Maybe in a few markets, who knows, but it just seems unlikely, especially with what’s happened in the last couple weeks with there’s a lot of activity going on.

Kathy:

Yeah. And it’s important to note that with sales down, sales down 30%, you’re getting a smaller pool of properties to even look at, and averages to even look at. It was kind of like in 2009, when everything was a foreclosure that was on the market, then prices seemed really low, but it wasn’t a real price, it was just foreclosure prices, because that was the main what was on the market, and that’s what we’re seeing. What’s on the market is maybe being discount, but that doesn’t really state the whole, it’s sales are down so low, it’s just a small percentage of what’s out there.

Dave Meyer:

Yeah, absolutely. Well it’s interesting what you said Jamil. I’m curious to hear how it evolves with these institutional buyers, because you’re sort of at the forefront of it in Phoenix. I think it would be interesting to know, in some of those other markets that you mentioned, you said like San Jose, I don’t think that’s a big institutional buyer area, or San Diego, it’s so expensive.

Jamil:

Not a huge institutional buyer area, but they do buy there, and it’s some of the… Also those smaller portfolio buyers, which are still… It’s still in the hundreds of millions of dollars when we’re talking about access to capital, and their ability to purchase. So, I mean, they’re still buying, they’re turning on the taps.

Henry:

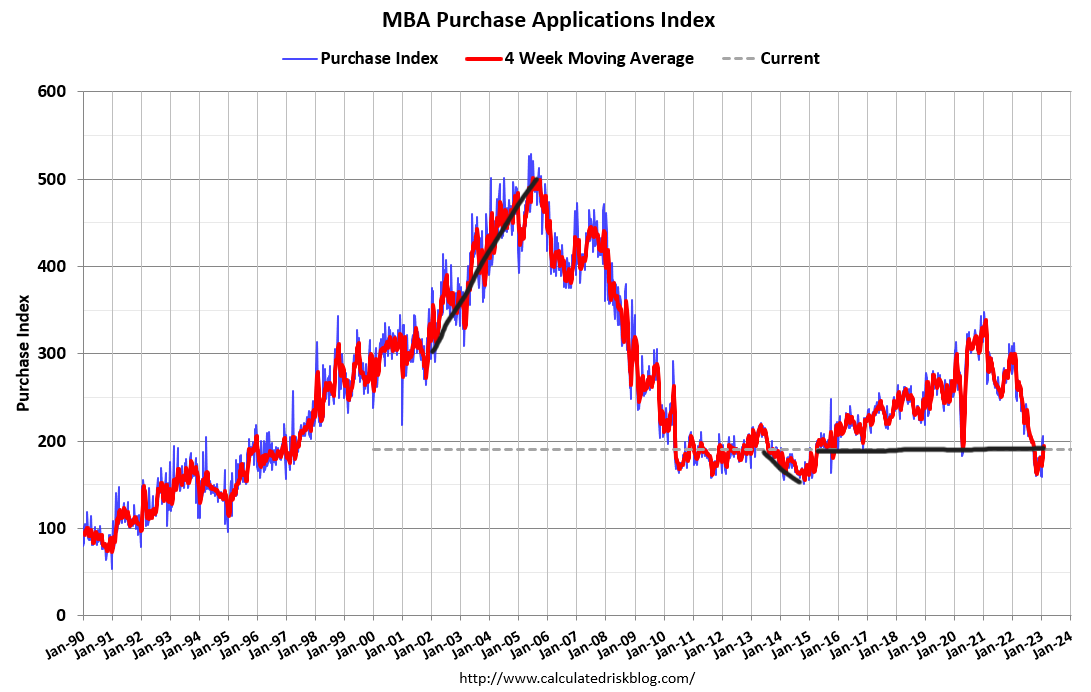

I am with you Jamil. I get it. I also, not a conspiracy theorist, but I mean, you can put pieces together of a puzzle, and if it makes a picture, it makes a picture. But what you’re saying is echoed in my market, it’s also right in line with the article that I brought to share, which is that mortgage demand has jumped 28% in one week, as interest rates are now at their lowest point in months.

And so, the highlights of the article are just saying that the average interest rate for a 30 year fixed is around between 6.2 To 6.4, and more people are applying for mortgages. It’s up 25% week over week. Now, putting that into perspective, that’s still down 35% from 12 months ago at this same time. But when you look at rates being at their lowest point since September, that’s significant.

And I think what you’re starting to see is that people are realizing that the two and 3% interest rates, that ship has sailed. I think people are finally starting to get it. We’re not going back there. We’re not going to get that low again. I mean frankly, a lot of people don’t want to get that low again, because what does that mean for what’s happening in the economy, if we have to get there again?

And so, people are just starting to realize that this is what you pay for an interest rate now. Life happens, and things move on. Yes, people are… There is a subset of people who are priced out of the market, but that’s going to happen, no matter what interest rate you’re at. So, there are some people that can afford to buy, some people that can’t. I think people are starting to… I think the sticker shock is wearing off, and it’s just now this is what rates are, and life continues to move on.

People need to move for different reasons. People want to move for different reasons. And when you have two income households who have stable jobs, and are making a decent salary, it’s easier for them to afford homes. And what I’m seeing in my market is echoing that. It’s echoing what you’re saying as well. We listed a flip, which would be considered for a luxury flip in my market, and that’s a “risky” strategy right now unless you’re James Dainard. So, those luxury flips, we put it on the market, we had it on the market for 24 hours, had 10 to 12 showings, and got four offers, all over asking price.

Jamil:

Over asking.

Henry:

Over asking. One of them… We listed it at 550, and we are under contract at 570.

Dave Meyer:

And what’s the median home price in your area, Henry?

Henry:

The median home price in my area is like 300.

Dave Meyer:

Oh, so this is really upscale.

Henry:

275 to 300. Yeah.

Dave Meyer:

Okay.

Jamil:

I think I want to move to northwest Arkansas, man.

James:

Yeah, I think we all should move there.

Dave Meyer:

We keep saying that, but I don’t even know if they have an airport. How do you even get there?

Henry:

We have an international airport. You have to remember-

Dave Meyer:

Sure.

Henry:

That the Waltons funded this place. Do you think the Waltons aren’t going to have an international airport built here, where they can get in and out?

Dave Meyer:

I think they have an airport that they use. I don’t know if we’re allowed to use it.

Henry:

Private.

Jamil:

Henry, was that 20% spike in mortgage applications national, or just in the-

Henry:

National.

Jamil:

Region… That’s nationally?

Henry:

Yes.

Jamil:

Guys.

Henry:

Mortgage applications are up. More people are entering the market because I think they feel a little more comfortable that these are what the rates are going to be, and people are applying for home loans. And also, to echo what Jamil was talking about, the money is starting to be in demand again.

I’ve had two conversations in the last seven days. One with an institutional buyer, just like Jamil was talking about, called me and said, “Hey, send me anything. Send me what you have, we want to buy.” And one a bank, yesterday, a banker, small local bank literally reached out to me and said, “Hey, we need your business. I can still do loans with a six in front of them,” which is, when you’re talking about commercial lending, we’re usually paying a higher rate, so that’s solid. So he’s like, “Bring me what you got. I can do loans with a six in front of them. I’m willing to be flexible with the rates and terms.” So, they’re wanting to lend, more people are buying, and so I kind of see what you’re saying, Jamil. I see what you’re saying.

Dave Meyer:

I like it. All right. Well, that’s super interesting. I mean, I think that we’re in this really odd spot with mortgage rates, where people don’t know if they’re going to go up or down. And so, anytime there’s this… Like over the next year or so, where if there’s these short term fluctuations where they go down, people are jumping in.

And I think this just goes to show something that people overlook from a housing market perspective, is just demographics. There are just a lot of people who want to buy homes, and they are willing to wait for a little bit for a mortgage rate, but most people aren’t like us, where they’re sitting around looking at the interest rates, and forecasting what they’re going to be in May, and then October, and thinking about their strategy. They’re like, “I want a house. It went down half a point, and I’m going to jump in now.” It just goes to show, that’s how homeowners who make up 70% of the housing market make their decisions. It’s not what we’re talking about. All right, Kathy, let’s round it out. What do you got for us?

Kathy:

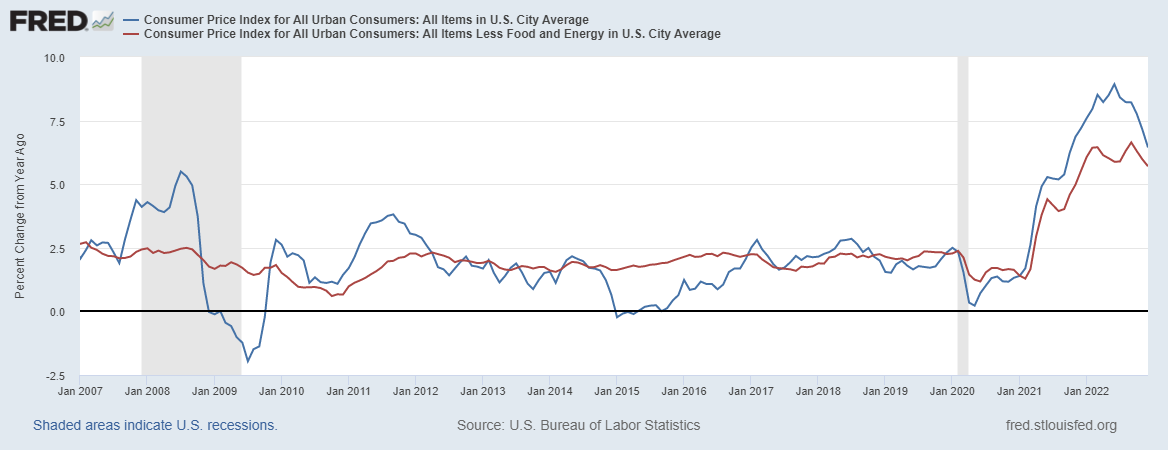

Well, this is actually a blog from the JP Morgan website. It’s JP Morgan Chase. The Economic Outlook for 2023, Trends to Watch. This was actually written in December, but I really think they’re pretty spot on so far. They said, “The US economy likely will slow this year, but the economy will grow.” So, it’s like half a percent to 1%. So, super slow growth, but that’s not a recession. That’s important, I think, for a lot of people who are hearing… I mean, all you have to do is type in recession on Google and you might want to get a handkerchief, and just cry a little bit.

But yes, the economy is slowing, but it doesn’t really look like a recession is coming quite yet, and they kind of predict it would be maybe towards the end of the year, or 2024, but mild. So, we shall see. It depends a lot on what the Fed does. Now the Fed just raised rates another 0.25%, and it looks like they’re going to do it again probably in their next meeting, another 0.25%.

And they’ve been saying for a long time they’re shooting for about a 5% fund rate, Fed fund rate, and they’re almost there. So, it could just be one more. A lot of people are in agreement that it would just be one more quarter percent rate hike, and then it just holds there for a bit.

And based on what we’re seeing, where we keep seeing job growth, and we keep seeing jobless claims declining, in spite of everything that’s happened this year, that could be true. That could be true that it’s a very mild recession at the end of the year. So those thinking that it’s going to be a 2008, it’s different. It’s different. Totally different dynamics this time around.

And then, as far as the housing market, you guys all said it all, I think we know it may be better than JP Morgan. I don’t know their lenders. They might probably need to know what to expect too. They’re expecting residential investment could be down 10 to 12% in 2023.

So again, that’s not a 2008 housing market crash, and that’s an average, meaning that some areas would do worse, and some areas would do better. And that’s what we were talking about, these different markets. I’ve been following John Burns Real Estate for many, many, many years, and that was always his message is that every single market is different. And there, again, no national housing market, and some are going to be more affordable, some are going to be less affordable, some are overpriced, some are underpriced. You’ve got to know your market in the end, when it comes to housing, but the overall economy really doesn’t look as bad as some people want to tell you it will be.

Dave Meyer:

I’m so glad you brought this up, Kathy, because I think that there is this overwhelming media narrative that there’s going to be a recession, and I think that is very unclear still. Economists, I just saw this poll by Bloomberg that said, I think it’s like 65% of economists think there’s going to be recession. So two out of three, that’s not a sure thing.

Goldman Sachs is the first bank that just upwardly revised their forecast. So, now they’re feeling more optimistic. They just said there’s going to be no recession in 2023. So, there’s some really interesting stuff here. The labor market is holding up surprisingly well. We just saw that GDP grew almost 3% in the fourth quarter. There’s interesting stuff here.

But I do want to say, that for the housing market in terms of appreciation and prices, narrowly avoiding a recession could be the thing that pushes housing prices down further, because that’s probably the only scenario I see where mortgage rates actually go up from where they are right now. Right?

Because if there’s a recession, that pushes down mortgage rates, and the only way I think mortgage rates go up is if the economy, if the yield curve kind of normalizes, and bond yields go up, and then we start to see mortgage rates closer to seven again. So, I don’t think they’re going to be crazy, but it’s just interesting that the overall economy doing well might be the thing that makes the housing market do worse.

Kathy:

Well, it wasn’t saying that the economy’s going to be robust, or again, growing. Normally you’d want to see a two or 3%, or 4% growth, and they’re saying maybe a 0.5% to 1%. So, I’m kind of still in the camp that mortgage rates are going to decline this year, based on the fact that the economy is slowing.

But this is, again, these are the headlines people see is, “Oh, the economy is down,” but oftentimes what they’re not seeing is, it’s the rate of growth that’s slowing. And that’s the same with housing prices. Like, “Oh, it’s down.” Yeah, the rate of growth is down, and that’s good compared to last year. So, again, read articles fully, because the headlines are meant to scare you, and unfortunately, too many people only read the headline.

James:

Does anyone else think that this is more of a slow squeeze, rather than a… It kind of had its jolt, now it’s like this slow squeeze that we’re going to be in for the next 12 to 24 months, but also, this slow squeeze could actually make rents go through the roof. As housing is just kind of out of reach, because if the economy’s not growing rapidly, that’s what we also saw. It wasn’t just rates, of why the housing market exploded. That was a huge portion of it, but it was also stock growth, investment growth, where access to liquidity was through the roof for people.

People were just printing money, and they could put money down. It’s like, “Oh, the house is up at 200 grand. Well, I’ll just put that down as by down payment.” And so the liquidity’s been squeezed, and so, right now, the cost of housing and the rent, it’s still a way out of whack. And so, I’m actually really starting to dig into some of these rental markets like, “Hey, I still see… Whereas I thought it was going to be stagnant, I’m actually starting to think that there could be some growth in some certain neighborhoods for sure.” Because the cost to own is just so out of whack still, and the slow squeeze is just going to make it harder to absorb that. Things will sell for pricing, but it’s going to be slower. So, in my opinion, rents are going to climb at that point.

Dave Meyer:

Interesting. Just because in markets, especially like in Seattle, just does not make sense financially to buy a house.

James:

No. Or like in Newport Beach. I mean, my rent payment’s a third of what my mortgage payment would be.

Dave Meyer:

Wow.

James:

No, it’s My rent payment is 50% less than my mortgage payment, if I put 50% down.

Dave Meyer:

What? That’s crazy.

James:

Oh, it’s crazy.

Dave Meyer:

Wow.

James:

I’m like, “It doesn’t make any sense to me. I’ll go buy an apartment building instead.” I don’t know. It just doesn’t… But yeah, so I could see some growth in that sector. The slow squeeze will actually, I think, get runway on the rents.

Dave Meyer:

All right. Well, I think that’s great advice. Don’t assume, just because people are saying that there’s a recession, and it’s a foregone conclusion that that is true. It’s actually a much more complicated, and nuanced economic situation, and that’s why there’s not really a real definition of recession. We’re just in this gray area.

I think Mark Sandy, the guy at Moody’s called it like a slow session. It’s like, it’s just going to be slow, and the economy’s going to be lame, but it’s not actually going to go backwards. So, there’s some nuance to it, and listen to shows like this, so you can understand it.

All right. Well, thank you all for being here. This was a lot of fun to have everyone back together. If you guys enjoyed this show, we would really appreciate some reviews. We get tens of thousands of people listening every week, but we only get like one review a week. All it takes is what? Five seconds. Go, give us a five star review on Spotify, or Apple. We really appreciate it. If you enjoy this type of show, and this type of content, it would mean a whole lot to us. Thank you all for listening. We’ll see you next time for On The Market.

On The Market is created by me, Dave Meyer and Kailyn Bennett, produced by Kailyn Bennett, editing by Joel Esparza, and Onyx Media, researched by Pooja Jindal, and a big thanks to the entire Bigger Pockets team. The content on the show On the Market are opinions only. All listeners should independently verify data points, opinions, and investment strategies.

:215-447-7209

:215-447-7209 : deals(at)frankbuysphilly.com

: deals(at)frankbuysphilly.com