When the refi market dried up in 2022, business took a drastic turn for Thuan Nguyen, CEO of Loan Factory and the top loan originator on the Scotsman Guide for the last two years. Prior to the downturn, more than 90% of Nguyen’s business came from refinances.

Nguyen says he has originated $467 million in origination volume this year, closing 1311 units by the end of November. This falls well below the landmark $1 billion he reached in 2020 and 2021.

Forecasting another purchase market in 2023, Nguyen started using his proprietary software for something new – to pursue relationships with realtors.

“I never had to work with realtors, but now I spend a lot of time working with realtors – supporting them and partnering with them,” Nguyen said in an interview with HousingWire.

He built features that cater to realtors’ needs – such as weekly updates on the housing market, daily alerts of mortgage rates and keeping real estate agents informed of borrowers’ pre-approval status.

While Nguyen had to cut his workforce to about half this year, he plans to scale his company in 2023 by hiring 1,000 LOs and targeting the purchase market in Loan Factory’s 44 licensed states.

“I think I built a very good system – good process and good technology. But then it’s been underutilized,” Nguyen said. “If I can open it up and share that with a thousand of LOs (…) instead of having a one to one win, now I can have a 1,000 to one win doing the same thing.”

Read on for Nguyen’s new business strategies for 2023, how he plans to scale his business and prospects for the housing market.

This interview has been condensed and lightly edited for clarity.

Connie Kim: Thuan, you hit a record $2.47 billion in origination volume last year, making you the loan originator with the most origination volume for two consecutive years on the Scotsman Guide. However, with your volume mostly coming from refis, how badly has it affected your business?

Thuan Nguyen: Not good. If you look at that (Scotsman guide) number, about 94% of my business was from refinance. Right now, there’s no more refinance, so it’s a big change.

Earlier this year was much better, but now it’s not good. I close about 60 loans a month only. For sure I won’t be able to make $1 billion [in origination volume] this year. My production until the end of November is 1311 units or $467 million. That is about one-fifth of the previous year. I don’t even know if I’ll be on top anymore.

It’s affecting everyone, but for me, it’s harder because most of my business comes from refinances.

CK: Are you doing all these productions by yourself? How is business delegated among team members?

Nguyen: I do have a team that works for me and supports me. There’s no way I can close that many transactions by myself. I cut [my team] down a lot. I have about five loan officers helping me, and I have more than 30 processors and assistants helping me.

CK: Has there been layoffs at Loan Factory as well?

Nguyen: I would say more than 100 layoffs at Loan Factory, and many of them also left voluntarily. Last year we had more than 200 employees, including LOs, processors, and assistants.

CK: With the market drastically shifting to a purchase market from refinances this year, how have you changed your business strategy, which was refi-dependant?

Nguyen: I changed my strategy a lot. In the past, I never had to work with realtors, but now I spend a lot of time working with realtors – supporting them and partnering with them.

Secondly, I did not recruit LOs, but now I have opened up. My company had only a few LOs, but now I want to grow full speed and focus on recruiting and supporting LOs.

My plan is to open up my platform, my resources, [and] my technology to help LOs who join me. Instead of focusing on myself, I’ll focus on recruiting LOs, training and supporting them and building a great platform so that they can make money easily. We have about two to three dozen independent LOs, but the goal is to have 1,000 LOs in 2023.

CK: The software you built for Loan Factory – Moso Software – automated a lot of the mortgage business model, whereas other lenders require loan originators to talk to borrowers. How has your software helped build relationships in a purchase mortgage-dependent market?

Nguyen: We built some features to support realtors. For example, we have subscriptions that go out to realtors weekly. Out of the 27,000 transactions, we have about 8,000 realtors that closed transactions with us. So the system will put them into a database and email them every week with market updates.

We also have another subscription sending daily alerts to realtors because a lot of them want to know the rates today, especially when rates keep on changing so fast. We also help realtors follow up with their clients.

A lot of agents send us loan pre-approval requests. Our system would monitor and update the realtor of the process of the borrower’s application. The software helps us monitor the production, the referrals they send to us, the referrals they send to them.

We track the referrals both ways, and that would allow us to improve their relationship. We send them a report every month showing how many transactions they sent us, how many clients we sent to them, and what their status is. So, with technology, we can do a lot of things and we can scale.

We build relationships with existing clients, too. For example, whenever we have a new client, we ask them how they found out about us and then we track that. We reach out to the referral and say thank you.

For example, if our client is happy with us, he refers his friends and family to us. We track that. We know who referred a new client to us; we say thank you. We show our appreciation. And I don’t think anyone out there does this. So we focus a lot on customer service.

CK: With the mortgage origination volume expected to shrink further next year, how do you plan on managing cost-cutting when you plan on hiring more LOs?

Nguyen: We have a great system in place. Everything is pretty much automated, highly automated, so we don’t have to cut costs anymore. Actually, if we have 1,000 LOs joining, we probably have to hire more people in the support system. I don’t expect to cut more, but we expect to hire more people.

I think I built a very good system – good process and good technology. But then it’s been underutilized. If I can open it up and share that with a thousand of LOs, those LOs can use those as a tool to go out and help consumers. Instead of having a one-to-one win, now I can have a 1,000-to-one win doing the same thing.

I’ve been selling subscriptions to my software, but the LO who joins my company can use my software free of charge. When they join, they can take advantage of everything I have – from technology, process, marketing, pricing, support, and even mentorship.

CK: Retail lenders gave out hefty signing bonuses to top producing LOs during the pandemic boom. Is this something you plan on doing to recruit top producers?

Nguyen: We want to recruit high production LOs, but at the same time, I see that some LOs have a lot of potential, so I’m open to everyone. Most of the signing bonus came from retail lenders. They charge super high interest rates. I don’t think that model will last.

The bottom line is how can they (LOs) attract a lot of clients, how can they close a lot of transactions. When LOs join a company, they’ll be looking for how much they will get paid per transaction, what kind of support do I need, what kind of pricing can I provide to my clients? Those are more important than the signing bonus.

CK: In addition to hiring more LOs in 2023, are you planning office expansions like you did in 2020?

Nguyen: Actually, I already expanded so fast. Right now, we are already in 44 states. So we cover almost the entire nation. License-wise, we are almost everywhere. The next step would be having 1000 LOs in the company – that’s how we’ll expand.

CK: There has been a lot of talk about retail LOs moving over to the wholesale channel amid the mortgage downmarket. Have you seen this trend as well?

Nguyen: Yes, for sure. Retail rates are so high, and I see that being a broker has so many advantages, especially the pricing. I think that trend will continue for sure. I don’t see any advantages in retail LOs.

In the past, many retail loan officers chose to work with lenders because they had a good process, a good system to support them. But now the broker system is improving a lot. Some brokers provide all kinds of support, or even the same level of support. So working with a mortgage broker that has a good support system, good process, [and] good pricing is way better than working for a retail lender.

CK: Who are your major wholesale partners, and what about them makes it easier for you to work with them?

Nguyen: Rocket Mortgage. We receive a lot of support from them – good pricing always, they have no early payoff penalty fee, underwriting support, no extension costs. There are a lot of perks they give us, and it’s in the contract. They have Pinnacle partners – I believe the top 15% of brokers would get better pricing.

CK: What kinds of products will gain traction in 2023?

Nguyen: I think right now, non-QMs are pretty popular. The newly released Freddie Mac’s Home Possible mortgage and Fannie Mae’s HomeReady mortgage to help first-time homebuyers and low income borrowers will become popular. Fannie Mae and Freddie Mac are helping people with low income, so I think that will become popular, as it will benefit a lot of people.

CK: Mortgage rates are expected to go down, but expected home sales numbers aren’t encouraging. Are you still hopeful about seeing an uptick in housing activity?

Nguyen: I think we are already starting to see that with rates starting to decline [as of] two, three weeks ago. I think we already hit the bottom. That’s why I feel optimistic. A lot of people can still afford and qualify. They’ve been waiting, so early next year they’ll jump into the market.

CK: With mortgage rates expected to drop to 5% levels, some LOs expect refi activity to go from homeowners who locked in rates at 7% levels. Is this in line with your expectations for next year?

Nguyen: No, because not many people took out loans at that rate. There weren’t a lot of transactions during that period, either. Plus, if their loan amount is small, what’s in it for them to refinance? So I don’t see a lot of support for that. It has to be purchase-heavy for sure next year.

CK: For those LOs that will be sticking with the industry, what strategies should they be deploying?

Nguyen: It’s all about relationships with family members, friends, [and] realtors, so focus on that and social media. There are so many loan officers, but only some will be successful. LOs will have to spend a lot of time on marketing on social media. Loan officers have to let the public know who they are and why they are good. They have to educate the public.

It takes a lot of effort, and it’s important to choose a good partner. If you don’t have a good system, good pricing, [and a] good process in place, how can you compete? It’s all about technology and pricing. Consumers got hit with high rates. They want to shop around. So if you work for a retail lender with high rates, how can you win? How can you get the customers? That’s why I say in the next year, you will see more consolidation, more retail LOs joining the broker channel.

Source link

:215-447-7209

:215-447-7209 : deals(at)frankbuysphilly.com

: deals(at)frankbuysphilly.com

New home sales still show a historic backlog

While new home sales did beat estimates in the latest Census report, with sales just floating around near the lows of the year, we can see with the monthly supply data that the builders still have way too much backlog of homes they need to build to raise their confidence.

One of the realities of COVID-19 has been the lag to build homes in a business that requires stable mortgage rates because of the traditional time to complete a home. It didn’t help the builders that they had a global pandemic and we still have many new homes either in construction or that haven’t been started yet.

Here is the breakdown of the 8.6 months of supply in the report:

So, you can see why we aren’t issuing new permits in a more significant fashion anytime soon. Based on my monthly supply model, it’s simply too high for the builders.

Cancelation rates are exploding on them. Mortgage rates jumped from 3% to 7.375% this year. This has led to the monthly supply data rocketing out of control, which has created a waterfall dive in the builders confidence. All these new home sales reports don’t even account for current cancelation rates in the sales data. This means the headline numbers we are seeing aren’t correct.

However, even if I adjust for that, sales trends have bounced off the lows for a while. The truth here that nobody wants to talk about is that we didn’t have a massive sales credit boom in housing from 2020-2021 like we saw from 2002-2005. The purchase application data always showed this to be the case, as well as the sales data. This means currently, the new home sales data is historically low already.

Today, new home sales are even lower if you adjust to the population. Remember that the population is still growing in America, we just got the recent report from Census that shows this to be the case. “The U.S. resident population increased by 0.4%, or 1,256,003, to 333,287,557 in 2022, according to the 2022 national and state population estimates.”

From Census: Sales of new single-family houses in November 2022 were at a seasonally adjusted annual rate of 640,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 5.8 percent (±22.7 percent)* above the revised October rate of 605,000, but is 15.3 percent (±13.0 percent) below the November 2021 estimate of 756,000.

The revisions were all negative, and I expect this trend to continue unless the recent fall in rates continues. That would reverse the problem the housing market has had selling homes with mortgage rates above 7%.

We must remember that the builders don’t operate like existing home sellers; they treat their products as commodities. This means they build it and try to sell it for as much money as possible and don’t want to see a significant backlog, which creates more deflationary problems for their profit margins.

Unlike an existing home seller who needs to find a home to live in after they sell, the new home sales market will never have that issue — or living in a house with a 3% mortgage rate that they don’t want to give up. You could have specific buyers that need to sell their current home in order to buy a new home and don’t want to bother with it now since rates are so much higher.

I believe more people simply don’t qualify, and the cancelation rate is something the builders have excellent data on.

Monthly supply of new homes still too high

My rule of thumb for anticipating builder behavior is based on the three-month supply average. This has nothing to do with the existing home sales market; this monthly supply data only applies to the new home sales market

The monthly supply data did fall in this report to 8.6 months, but it is still simply too high for the builders to issue more permits; thus, the housing recession continues.

From Census: For Sale Inventory and Months’ Supply The seasonally‐adjusted estimate of new houses for sale at the end of November was 461,000. This represents a supply of 8.6 months at the current sales rate.

The median sales price of new homes doesn’t reflect reality

The median sales price looks strong year over year and slightly declines month to month. However, we always have to be skeptical of median sales prices, especially in the new home market. Selling bigger homes in a smaller sales lot can distort prices. This can also work in the opposite direction, as median sales prices can seem to fall significantly when smaller-priced homes are selling.

From Census: Sales Price The median sales price of new houses sold in November 2022 was $471,200. The average sales price was $543,600.

A lot of new homes left to build

With excess housing supply and so many homes left to build, you can see why the builder’s confidence has collapsed, as mortgage rates have risen so much this year.

We have seen that since mortgage rates have fallen, purchase application data has grown for over seven weeks, and the builder’s confidence looking out six months went positive, working from a shallow bar.

The housing market dynamic can undoubtedly change if mortgage rates can move down to 5% with duration and stick. If that doesn’t happen, the housing recession, which started in June of this year, will be hitting its first anniversary next year. The early Christmas present of lower mortgage rates did breathe some life into this sector, and we will keep our eye on that going forward.

Source link

New home sales surprise in November

New home sales, to the surprise of many, rose by 5.8% in November to a seasonally adjusted annual rate of 640,000, according to data published by the U.S. Census Bureau and the Department of Housing and Urban Development (HUD) on Friday.

New home sales data last month was much stronger than had been anticipated; the market had expected a contraction of 4.7% in November. The median sales price of new houses sold last month was $471,200 and the average sales price was $543,600, according to the data.

A combined dip in mortgage rates and significant incentives from homebuilders was the driving force last month, analysts said. But make no mistake, conditions are still sub-optimal and the new home sales data doesn’t capture all of the headwinds, such as declines in permitting and cancelations.

“Despite the modest uptick in contracts signed on new homes, the housing market remains in a lull, a pattern that likely will continue as we head into January,” Lisa Sturtevant, the chief economist of Bright MLS, said in a statement. “The median price of a new home rose again in November, defying expectations that builders would slash prices to work through inventory… Instead of cutting prices, builders seem to be working through existing inventory by offering concessions instead of price cuts. Home prices did fall from October, which is more of a seasonal trend.”

The Census Bureau and HUD also sharply revised estimates downward for the past three months to account for high rates of cancelations. Since July, about 10,000 contracts have been canceled each month, according to data from John Burns Consulting. Though gross new home sales year-to-date is 602,000, new new home sales are about 519,000, the company’s data shows.

The seasonally adjusted estimate of new houses for sale at the end of November was 461,000, which represents 8.6 months of supply at the current sales rate.

The incentives will need to be amped up if homebuilders are to make sales.

“Builder sentiment and permit data indicate ongoing weakness in the new-home market,” said First American Deputy Chief Economist Odeta Kushi. “With higher mortgage rates and greater economic uncertainty, new-home prices will need to continue to adjust to entice more buyers.”

Added Sturtevant: “Homebuilders are banking on home shoppers returning to the market in the first part of 2023. With mortgage rates sliding, it is likely that there will be more traffic as we head into spring. However, new home builders will face more competition from existing homes as inventory continues to rise.”

Source link

Prepayment activity to slow in 2023 as mortgage delinquencies face pressure

Prepayment activity is expected to face seasonal headwinds into early 2023 after hitting another record low in November.

“Record low refinance activity and lackluster home sale volume driven by still historically tight home affordability” was the result of prepayment dropping 15.6% to a single-month mortality rate of 0.40%. This was below the previous record of 0.48%, Andy Walden, VP of enterprise research and strategy at Black Knight, said.

Home sales tumbled more than 7% in November, marking 10 straight months of decline, according to the National Association of Realtors (NAR). Demand for refi was down a staggering 84.5% from a year ago, Mortgage Bankers Association‘s (MBA) data showed.

“Prepayment speeds will continue to run into season headwinds over the next two months with housing turnover related prepayments – which now make up a record 60% of all prepayments – typically falling by 25% from November through January,” Walden said.

Rate lock volume, which acts as a leading indicator for both origination and prepayment activity, also suggested a downward trend. Overall lock volume was down 21.5% in November compared to October — and down another 10-15% lower over the first three weeks of December, despite declines in recent interest rates.

The national delinquency rate rose another 3.5% in November to 3.01%, up 10 basis points from October. An increase in 30-day delinquencies, which jumped by 31,000 cases, and a rise in 60-day delinquencies, which escalated by 25,000, led the climb.

Improvement among seriously past-due loans by 90 or more days continued to stagnate, with the population of 90-day delinquencies ticking down -0.2% from the month prior.

Despite trending higher in recent months, the national delinquency rate of 3.01% in November is still more than a half-percent below its pre-pandemic level of 3.53% in November 2019.

“Mortgage delinquencies, which still remain historically low, have begun facing upward pressure from a number of factors including seasonal trends, the recent hurricane in Florida, shifting credit quality due to rising rates and tightening affordability, and broader macro-economic pressures,” Walden said.

Source link

Mortgage rates are falling. How low can they go in 2023?

Mortgage industry executives, analysts and economists have started to place their bets on where mortgage rates will settle in 2023 amid the Federal Reserve’s tightening monetary policy and the fears of an economic recession. Spoiler alert: don’t expect much, if any, relief for borrowers in the short term.

It’s true that after doubling over the course of a year, the 30-year fixed mortgage rate is trending downward at the close of 2022. On Thursday morning, a Freddie Mac survey showed this week’s rates at 6.27%, four basis points lower than the previous week. (Mortgage rates averaged 3.05% one year ago.) And Mortgage News Daily’s tracker clocked rates at 6.28% on Thursday, about 10 basis points lower than Wednesday.

Despite the small drop in mortgage rates in recent weeks, they won’t drop significantly any time soon, analysts and mortgage executives told HousingWire.

“Our baseline is not for the Federal Reserve to cut rates next year,” said Bose George, mortgage sector analyst at Keefe, Bruyette and Woods. “Spreads could tighten a little bit, and then maybe you get a mortgage rate that’s 5.75% to 6% something, which will be a slightly positive benefit to the market, but not much.”

“The Mortgage Bankers Association is assuming mortgage rates are down to the low fives in the next year. Their volume expectations are a little more positive than ours because that leads to an improvement in the back half of next year. But we’re not building that in at the moment,” he added.

The latest MBA mortgage finance forecast shows the 30-year fixed rate at 5.2% at the end of 2023.

“MBA expects the housing market and broader economy to remain volatile in early 2023, but with mortgage rates on a downward trajectory, prospective buyers could return to the market,” MBA president and CEO Bob Broeksmit said in a statement.

The lender outlook on mortgage rates

Those closer to the borrowers – the mortgage lenders – don’t expect rates to go significantly down either.

“I think we’ll be hovering around 6% to 8% for a little while. I don’t see any major items that would cause rates to drop in 2023,” said United Wholesale Mortgage’s chief strategy officer, Alex Elezaj.

“Nobody has the crystal ball to know, but we are making sure that as the next refi opportunity comes, our wholesale brokers have the tools in place to execute for their borrowers,” Elezaj added.

Sonu Mittal, head of mortgages at Citizens Bank, expects rates to stay where they are for at least the first half of 2023.

“Then we can see a downward trend, but nothing anywhere close to what we saw before,” he said. “I think rates will settle down somewhere in the middle 5s. But I’m sure you will see all the forecasts.”

According to Sam Khater, Freddie Mac’s chief economist, heading into the holidays, mortgage rates continued to decrease, which is helpful for potential homebuyers.

“But new data indicates homeowners are hesitant to list their homes,” Khater said in a statement. “Many of those homeowners are carefully weighing their options as more than two-thirds of current homeowners have a fixed mortgage rate of below 4%.”

Borrowers are hesitant because of a combination of high interest rates, a sense that a home price correction has to happen and that a recession is coming, according to David Battany, executive vice president of capital markets at Guild Mortgage.

“It’s the combination of the actual math of a higher payment or just the psychological effect of rates being really high and home prices probably softening,” Battany explained.

To illustrate the impact of higher mortgage rates, the monthly payment for a median-priced home is currently more than $2,000, a 64% increase from a year ago, according to Realtor.com‘s manager of economic research, George Ratiu. “First-time homebuyers are struggling with high consumer prices, property values and interest rates, which are pushing savings rates to very low levels and delaying their ability to gather a sufficient down payment,” Ratiu said in a statement.

At the same time, Ratiu said, current homeowners looking for their next home “are finding that the prospect of higher prices and, in many cases, double or triple their current interest rate, are causing them to rethink their decision to move.”

Source link

Pitfalls, Potential, and Passive Opportunities

This article is presented by Aloha Capital. Read our editorial guidelines for more information.

More and more real estate investors are exploring what it might look like to be on the other side of the closing table. I don’t mean being the seller, but rather being the lender. With interest rates on the rise, you can easily earn double-digit interest rates by funding or buying short-term notes.

Imagine investing in real estate where you don’t need to manage a rehab, sign a personal guarantee, or deal with tenants. And if things go wrong, someone other than you loses their money before you lose a dollar. Sounds pretty nice, right?

So, how exactly do you go about becoming a lender? How can you make money lending? How do people lose money lending? And finally, is there a way to be a passive lender so you can sit back and earn passive income from active real estate investors?

I have funded over $500 million in loans in the past five years as the leader of Aloha Capital, a nationwide lender focused on financing residential investment properties. At BPCON22 in San Diego, I had so many conversations with BiggerPockets community members where they mentioned sitting on significant cash reserves that were not getting reinvested into their next deal—why? Because their ideal profit or cash flow from their fix and flip, BRRRR, or turnkey rental strategy was no longer attainable in the markets they have been investing in. Not knowing when they would find their next deal, many were excited to learn how to put their capital to work as a passive private lender.

Can you make double-digit returns as a lender? Yes, of course. Can you lose money as a lender? You sure can! In this article, we will unpack what it takes to be a lender, including:

Let’s get started.

Passive vs. Active Lending

I can tell you firsthand that private lending is far from passive if you are doing it the right way.

You must find qualified borrowers and acceptable deals that meet your criteria, provide competitive terms, then underwrite the borrower’s experience, liquidity, and creditworthiness. You will also need to underwrite the as-is value (AIV) and after-repair value (ARV) along with the detailed rehab budget to ensure the project has the appropriate profit margin for the borrower to make money or if it is a rental exit, the likelihood that the property will cash flow with a rate/term refinance.

That’s just the beginning. Before you fund the loan, you need to ensure that the title insurance policy and property insurance mitigate risk to you as the lender and then produce loan documents that include all of the business terms and lender protections while staying within state-specific compliance requirements.

Now that the loan is funded, you should be ensuring that the rehab timeline is being met and likely send additional money to the borrower to cover costs. All along the way, you need to account for and collect interest from the borrower.

Alternatively, there are opportunities to lend passively by investing in real estate notes or in a real estate debt fund managed by a professional investment property lending business. This provides access to annual returns similar to those you would receive through direct private lending while gaining passive investing benefits by tapping into the lender’s operational infrastructure, expertise, and deal flow.

For example, Aloha Capital has 20+ full-time employees, all with backgrounds in real estate lending and investing, who are focused on finding, underwriting, originating, and servicing loans. Aloha offers investors access to 8 to 14% returns from real estate notes via the Aloha Passive Note Platform, where passive investors can select an already underwritten and originated note, purchase it, and relax while Aloha Capital services the loan.

In addition, investors can gain access to a diversified portfolio of short-term loans via the Aloha LTD Income Fund, which has an 8% annual return target, no lockup period, and a 7-year track record. In addition, there are other opportunities to gain exposure to note investing, such as crowdfunding platforms where you can own a fraction of a note and private lender matchmakers that broker borrowers needing a loan and private individuals interested in private lending.

How Lenders Make Money

If you have capital, lending is a great way to make high-yield returns. Lenders providing short-term loans on investment properties can earn interest ranging from 8%-15% annually, along with loan origination fees of 0%-3%. In addition, if the loan extends past maturity, you can charge an extension fee, and if the loan goes into default, you can charge default interest of 20% or more annually (the actual max rate depends on the state usury laws).

Although this is a large range, in the current real estate environment, a double-digit annual return in first position, with the borrower having equity in the deal, is pretty standard.

For clarity, a first position or lien is secured by the underlying collateral in the case of real estate lending the subject property. This means that if the borrower defaults on your loan, you, as the lender, can seize the collateral to recoup your capital and unpaid interest through foreclosure. If you are a junior lender, you are not able to foreclose, and the principal of your loan is only available upon the first position lender being paid in full. Although you may earn a slightly higher interest rate as a junior lender, you are increasing your risk of principal loss substantially if the borrower ever defaults.

How Lenders Lose Money

We’ve talked about making money as a lender. Now, let’s discuss how to not lose your money.

As the lender, ideally with a first position lien, you create a promissory note that is collateralized by a property through a security instrument (typically a mortgage or deed of trust), and ideally, this loan has a personal guarantee of payment from the guarantor(s).

So how do you lose money as the lender? Here are the top three ways:

1. Not being in the first position

Occasionally, borrowers cannot execute their game plan to rehab, sell or rent a property. Or circumstances occur where they are no longer able to cover debt service, or their rehab budget is not sufficient. In this case, the lender in the first position will take action to ensure they recover all or a majority of their capital through foreclosure, a deed in lieu of foreclosure, forbearance, or another method.

If you are not the first-position lender in this scenario, you are the junior lender, and you have two options to choose from:

2. Lending to borrowers with limited experience, low credit, or insufficient liquidity

These are the three primary factors that I believe drive the risk of loan delinquency and default. You should seek out borrowers that meet your standards in two of three of these categories. If they only qualify in one category, you should require an additional guarantor that satisfies your requirements or pass on funding the deal!

3. Ignoring the borrower’s exit strategy

Ideally, as a lender, you understand the dynamics of the market you are lending in and the borrower’s exit strategy. If you are not adjusting your rate, fees, and leverage based on the loan exit options available to the borrower, then you may be setting yourself up to lose money. If the property needs to be rented instead of sold, does the property cash flow with your loan in place or will the borrower be able to refinance into another loan? If you don’t know, don’t fund it!

Conclusion

In conclusion, anyone can be a private lender if they have access to capital. But seeking out the returns from private lending without actively avoiding the pitfalls may lead to losses rather than gains.

Like most real estate strategies, you can be a passive or active lender. I hope that this provides some perspective on how passive lending with the right lending partner delivers a great combination of income and risk mitigation. If you go it alone, I hope you take into consideration the three ways to avoid losing money before you fund your first deal.

This article is presented by Aloha Capital

Aloha Capital provides residential real estate investors with access to competitive, transparent, and reliable loans to active real estate investors across the country. We offer short-term bridge loans for Fix & Flip, BRRRR, Short-Term Rental, and Multifamily investors, along with long-term interest only and amortizing loans on single-family, townhomes, condos, and small to mid-sized multifamily properties. We also provide vertical development loans on infill residential properties to spec builders and build-to-rent investors.

Through our accredited investor fund and direct note investment portal, investors seeking passive income can earn up to 12% annualized return through notes originated, underwritten, and serviced by Aloha Capital.

Note By BiggerPockets: These are opinions written by the author and do not necessarily represent the opinions of BiggerPockets.

Source link

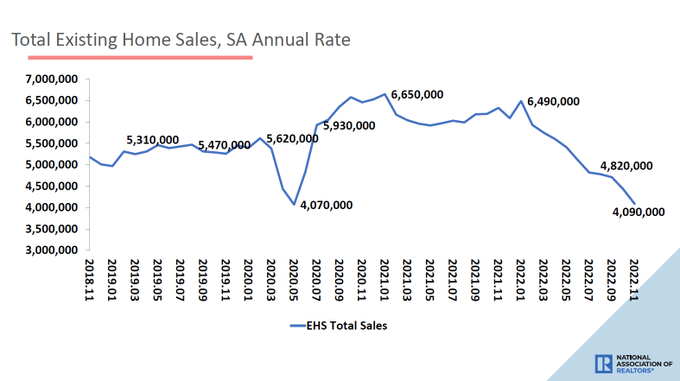

Have we found the bottom in existing home sales?

On Wednesday, existing home sales collapsed near the lows we saw during COVID-19 and back in 2007 when the housing bubble burst. In addition, this is the fourth straight month of inventory declining, while days on the market are growingl! Confused by this? I hear you; let’s dive deeper into today’s report.

From NAR: “In essence, the residential real estate market was frozen in November, resembling the sales activity seen during the COVID-19 economic lockdowns in 2020,” said NAR Chief Economist Lawrence Yun. “The principal factor was the rapid increase in mortgage rates, which hurt housing affordability and reduced incentives for homeowners to list their homes. Plus, available housing inventory remains near historic lows.”

One of the housing economic realities that I have been trying to stress this year is that a traditional seller of a home is typically a buyer as well. This explains why total active listing inventory data has been stable over the decades, with the exception of 2006-2011, when those forced distressed credit home sellers couldn’t buy.

Since the credit standards have improved post-2010, we shouldn’t see distressed sellers until a job loss recession happens, even if sales fall noticeably. This happened during the early months of COVID-19, and we have not seen the panic selling in 2022 like some people predicted.

Housing inventory

Today, inventory is almost 900,000 active listings below the lowest level of the four-decade average between 2 million and 2.5 million.

Inventory is now down again in the NAR report; this is the fourth month of inventory decline, now running at 1.14 million. The all-time lows were around 860,000 this year, and the all-time high was a tad over 4 million in 2007.

We have had two historic events that created a waterfall dive in demand recently; we now have precise data showing new listing data declining with those events, which shows how important that data line is to housing demand. This is the biggest story in housing.

For a decade, the traditional view on housing has been that when demand collapses, inventory will spike higher, which is what we saw during the years when the housing bubble burst.

I have never believed in this concept because of how the housing market credit channels work. I have stressed that inventory can grow through a weakness in demand over time. This means what we saw in 2005-2008 with the inventory spike was a historic event that hasn’t been replicated at any time in recent U.S. economic history.

We have one data line that clearly shows the credit stress in the system, and it’s been my favorite chart at all my events (see below). Without significant credit stress in the system, we can’t ever assume we will see inventory scale spikes where sellers will not be able to buy homes because of a foreclosure or short sale.

We can believe in a forced equity seller premise, where someone loses their job and needs to sell their home to gain access to money. That is a real live talking point, but it will require a job loss recession. As we can see below, the U.S. housing market had high levels of credit stress in 2005 through 2008; then, after all that, we had the job loss recession. None of that has ever happened again since 2012.

Hopefully, this explains why total active listings are still low, and the NAR data has now shown four months of decline. We have a shot at having total active listings below 1 million over the next two months because demand is picking up during a seasonal inventory decline period.

Below, you can see the decline in sales data, which is not as sharp and short as we saw during COVID-19 but a waterfall dive in demand nonetheless. Mortgage rates spiked in March, and then the new listing data started to decline at the end of June. My line in the sand has always been 4 million on the monthly existing home sales prints because it’s been a rare event that sales go below that level post-1996.

We have broken under 4 million existing home sales only twice post-1996. First was the tail end of the housing bubble bursting in 2008, and second was in 2010 in the aftermath of the homebuyer tax credit when sales were pulled forward and then collapsed.

From NAR: Total existing-home sales waned 7.7% from October to a seasonally adjusted annual rate of 4.09 million in November.

One of the most encouraging signs I see in today’s report, which I also loved in the last report, is that the days on the market are growing.

I am not, nor will I ever be, a fan of a housing market with days on the market in the teens or lower. This means we don’t have enough active listings for buyers, forcing people to bid against each other. I consider this growth year over year from 18 days to 24 days as a plus and a step toward a more normalized housing market.

NAR: First-time buyers were responsible for 28% of sales in November; Individual investors purchased 14% of homes; All-cash sales accounted for 26% of transactions; Distressed sales represented 2% of sales; Properties typically remained on the market for 24 days.

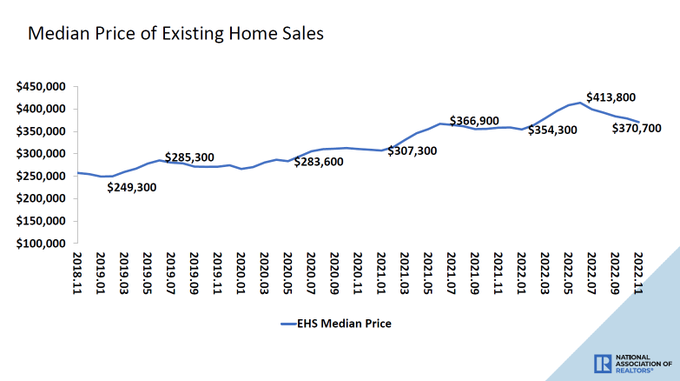

Home-price growth is cooling off dramatically, which is another awesome thing about housing this year. Yes, I know I am very biased here. Since February 2022, I have labeled the housing market savagely unhealthy as home prices have escalated well above my 23% home price growth model for 2020-2024 in less than two years.

This is why my rants of needing higher mortgage rates went into overdrive back then. However, now we are working our way back to a normal marketplace, which is good, not bad.

NAR: The median existing-home price for all housing types in November was $370,700, an increase of 3.5% from November 2021 ($358,200), as prices rose in all regions. This marks 129 consecutive months of year-over-year increases, the longest-running streak on record.

Purchase applications

The other housing news of the day, the forward-looking purchase application data, had another positive trend data line report. The week-to-week action saw a slight 0.1% decline, but now the year-over-year decline is 36%. As crazy as this sounds, that is 10% above the lows we had this year when this index was down 46% year over year.

Now, we need to add some context to this data line.

During the months of October 2021 to January 2022, we had a rare volume rise in the purchase application data, which took existing home sales toward 6.49 million in January of this year. This meant that all housing data, especially purchase application data, would have extremely hard comps to work with this year from October to January.

When I saw where trend sales data was going, I was anticipating that purchase application data would be down on average between 35%-45% year over year from October to January. So far this year, we have been down 36%-46% during this period. So, the data looks normal to me, as I was anticipating this.

What I didn’t anticipate was how well the market reacted to mortgage rates that went 1.25% lower in a short amount of time. This sent this data line positive for seven straight weeks, making us rise from the bottom decline of 46% year over year to now just 36%.

This means, for now, we have found a bottom in the data and bounced off the lows with positive trending data. This means in a few months, the existing home sales data should look better as this data line looks out 30-90 days.

The big takeaway in today’s existing home sales report is that we need to see new listing data grow in 2023 to get more home sales. Some people might believe that new listing data being negative is good for the housing market because it means inventory is stable. I believe this is the wrong way to look at the housing market. We want to see people list their homes and move when they want to. That is just a function of life; not everyone sits in the same home for 18 years like me.

Hopefully, in 2023, when we see the traditional inventory rise, this will come with new listing data growth, and we can get the total national inventory levels back to 2019 levels, which I will be very happy to see.

The housing market couldn’t take the shock of mortgage rates moving from 3% to 7.375% in one year, and this forced some people to change their minds about selling their home since they will have to buy another one. Hopefully, a more stable mortgage rate market means new listing data can grow in 2023.

Source link

Lower mortgage rates, higher demand lead to optimism for late 2023

Lower mortgage rates helped to increase borrowers’ demand for home loans last week, which in turn drummed up optimism for the mortgage industry at the end of 2022. Economists believe that if the trend continues, the market will be able to improve in the second half of 2023.

“The latest data on the housing market show that homebuilders are pulling back the pace of new construction in response to low levels of traffic, and we expect this weakness in demand will persist in 2023, as the U.S. is likely to enter a recession,” Mike Fratantoni, Mortgage Bankers Association’s senior vice president and chief economist, said in a statement.

“If mortgage rates continue to trend down, as we are forecasting, more buyers are likely to return to the market later in the year, as affordability improves with both lower rates and slower home-price growth,” Fratantoni added.

Last week, the Federal Reserve raised the federal funds rate by 50 basis points to 4.25%-4.50%. This was a smaller hike than the 75 bps per meeting the policymakers have stuck to since June and was due to inflation slowing more rapidly than expected in November.

Consequently, mortgage rates started a downward trend.

The latest MBA survey shows that the average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) decreased to 6.34% last week, down from the previous week’s 6.42%. Rates for jumbo loan balances (greater than $647,200) went from 6.14% to 5.97% in the same period.

The average 30-year fixed rate mortgage, according to Mortgage News Daily, was 6.38% on Tuesday.

According to Mark Fleming, chief economist at First American, the housing market potential in 2023 will remain largely dependent on the path of mortgage rates.

“If inflation decelerates toward the Fed’s target range in the second half of 2023, as is currently expected, then it’s possible that mortgage rates may decline modestly in the latter half of the year,” said Fleming. “While mortgage rates will remain high compared with pandemic-era lows, stable and potentially modestly lower mortgage rates will elevate housing market potential in 2023.”

Uptick in applications

Borrowers’ demand for home loans quickly reacted to lower mortgage rates. The MBA survey shows that the mortgage composite index for the week ending Dec. 16 increased 0.85% from the prior week, but was down 64% compared to the same period in 2021.

The refinance index increased 6% from the week prior and was 84.5% lower than the same week one year ago. Meanwhile, the seasonally adjusted purchase index held steady from one week earlier — and was down 36.5% from this time last year.

The survey, conducted weekly since 1990, covers 75% of all U.S. retail residential mortgage applications.

“The Federal Reserve raised its short-term rate target last week, but longer-term rates, including mortgage rates, declined for the week, with the 30-year conforming rate reaching– its lowest level since September,” Fratantoni said. “This is a particularly slow time of year for home buying, so it is not surprising that purchase applications did not move much in response to lower mortgage rates.”

The MBA survey also shows that refinancing’s share of mortgage activity increased to 31.3% last week from 29.4% of total applications in the prior week. The FHA share of total applications decreased slightly to 13% from 13.1% the week prior. The VA share rose from 11.5% to 11.9%. Meanwhile, the USDA share remained unchanged during the same period.

Due to long-run interest rates pulling back over the past month, Fannie Mae‘s latest forecast projects total home sales to be 5.72 million units in 2022, up from 5.67 million in the prior forecast. However, total home sales for next year are expected to decrease to 4.57 million – up from 4.42 million previously projected by the economists.

Total mortgage origination activity is expected to be at $2.35 trillion in 2022 and $1.70 trillion in 2023, unchanged from the previous forecasts.

Source link

How top LO Thuan Nguyen plans to grow his business in 2023

When the refi market dried up in 2022, business took a drastic turn for Thuan Nguyen, CEO of Loan Factory and the top loan originator on the Scotsman Guide for the last two years. Prior to the downturn, more than 90% of Nguyen’s business came from refinances.

Nguyen says he has originated $467 million in origination volume this year, closing 1311 units by the end of November. This falls well below the landmark $1 billion he reached in 2020 and 2021.

Forecasting another purchase market in 2023, Nguyen started using his proprietary software for something new – to pursue relationships with realtors.

“I never had to work with realtors, but now I spend a lot of time working with realtors – supporting them and partnering with them,” Nguyen said in an interview with HousingWire.

He built features that cater to realtors’ needs – such as weekly updates on the housing market, daily alerts of mortgage rates and keeping real estate agents informed of borrowers’ pre-approval status.

While Nguyen had to cut his workforce to about half this year, he plans to scale his company in 2023 by hiring 1,000 LOs and targeting the purchase market in Loan Factory’s 44 licensed states.

“I think I built a very good system – good process and good technology. But then it’s been underutilized,” Nguyen said. “If I can open it up and share that with a thousand of LOs (…) instead of having a one to one win, now I can have a 1,000 to one win doing the same thing.”

Read on for Nguyen’s new business strategies for 2023, how he plans to scale his business and prospects for the housing market.

This interview has been condensed and lightly edited for clarity.

Connie Kim: Thuan, you hit a record $2.47 billion in origination volume last year, making you the loan originator with the most origination volume for two consecutive years on the Scotsman Guide. However, with your volume mostly coming from refis, how badly has it affected your business?

Thuan Nguyen: Not good. If you look at that (Scotsman guide) number, about 94% of my business was from refinance. Right now, there’s no more refinance, so it’s a big change.

Earlier this year was much better, but now it’s not good. I close about 60 loans a month only. For sure I won’t be able to make $1 billion [in origination volume] this year. My production until the end of November is 1311 units or $467 million. That is about one-fifth of the previous year. I don’t even know if I’ll be on top anymore.

It’s affecting everyone, but for me, it’s harder because most of my business comes from refinances.

CK: Are you doing all these productions by yourself? How is business delegated among team members?

Nguyen: I do have a team that works for me and supports me. There’s no way I can close that many transactions by myself. I cut [my team] down a lot. I have about five loan officers helping me, and I have more than 30 processors and assistants helping me.

CK: Has there been layoffs at Loan Factory as well?

Nguyen: I would say more than 100 layoffs at Loan Factory, and many of them also left voluntarily. Last year we had more than 200 employees, including LOs, processors, and assistants.

CK: With the market drastically shifting to a purchase market from refinances this year, how have you changed your business strategy, which was refi-dependant?

Nguyen: I changed my strategy a lot. In the past, I never had to work with realtors, but now I spend a lot of time working with realtors – supporting them and partnering with them.

Secondly, I did not recruit LOs, but now I have opened up. My company had only a few LOs, but now I want to grow full speed and focus on recruiting and supporting LOs.

My plan is to open up my platform, my resources, [and] my technology to help LOs who join me. Instead of focusing on myself, I’ll focus on recruiting LOs, training and supporting them and building a great platform so that they can make money easily. We have about two to three dozen independent LOs, but the goal is to have 1,000 LOs in 2023.

CK: The software you built for Loan Factory – Moso Software – automated a lot of the mortgage business model, whereas other lenders require loan originators to talk to borrowers. How has your software helped build relationships in a purchase mortgage-dependent market?

Nguyen: We built some features to support realtors. For example, we have subscriptions that go out to realtors weekly. Out of the 27,000 transactions, we have about 8,000 realtors that closed transactions with us. So the system will put them into a database and email them every week with market updates.

We also have another subscription sending daily alerts to realtors because a lot of them want to know the rates today, especially when rates keep on changing so fast. We also help realtors follow up with their clients.

A lot of agents send us loan pre-approval requests. Our system would monitor and update the realtor of the process of the borrower’s application. The software helps us monitor the production, the referrals they send to us, the referrals they send to them.

We track the referrals both ways, and that would allow us to improve their relationship. We send them a report every month showing how many transactions they sent us, how many clients we sent to them, and what their status is. So, with technology, we can do a lot of things and we can scale.

We build relationships with existing clients, too. For example, whenever we have a new client, we ask them how they found out about us and then we track that. We reach out to the referral and say thank you.

For example, if our client is happy with us, he refers his friends and family to us. We track that. We know who referred a new client to us; we say thank you. We show our appreciation. And I don’t think anyone out there does this. So we focus a lot on customer service.

CK: With the mortgage origination volume expected to shrink further next year, how do you plan on managing cost-cutting when you plan on hiring more LOs?

Nguyen: We have a great system in place. Everything is pretty much automated, highly automated, so we don’t have to cut costs anymore. Actually, if we have 1,000 LOs joining, we probably have to hire more people in the support system. I don’t expect to cut more, but we expect to hire more people.

I think I built a very good system – good process and good technology. But then it’s been underutilized. If I can open it up and share that with a thousand of LOs, those LOs can use those as a tool to go out and help consumers. Instead of having a one-to-one win, now I can have a 1,000-to-one win doing the same thing.

I’ve been selling subscriptions to my software, but the LO who joins my company can use my software free of charge. When they join, they can take advantage of everything I have – from technology, process, marketing, pricing, support, and even mentorship.

CK: Retail lenders gave out hefty signing bonuses to top producing LOs during the pandemic boom. Is this something you plan on doing to recruit top producers?

Nguyen: We want to recruit high production LOs, but at the same time, I see that some LOs have a lot of potential, so I’m open to everyone. Most of the signing bonus came from retail lenders. They charge super high interest rates. I don’t think that model will last.

The bottom line is how can they (LOs) attract a lot of clients, how can they close a lot of transactions. When LOs join a company, they’ll be looking for how much they will get paid per transaction, what kind of support do I need, what kind of pricing can I provide to my clients? Those are more important than the signing bonus.

CK: In addition to hiring more LOs in 2023, are you planning office expansions like you did in 2020?

Nguyen: Actually, I already expanded so fast. Right now, we are already in 44 states. So we cover almost the entire nation. License-wise, we are almost everywhere. The next step would be having 1000 LOs in the company – that’s how we’ll expand.

CK: There has been a lot of talk about retail LOs moving over to the wholesale channel amid the mortgage downmarket. Have you seen this trend as well?

Nguyen: Yes, for sure. Retail rates are so high, and I see that being a broker has so many advantages, especially the pricing. I think that trend will continue for sure. I don’t see any advantages in retail LOs.

In the past, many retail loan officers chose to work with lenders because they had a good process, a good system to support them. But now the broker system is improving a lot. Some brokers provide all kinds of support, or even the same level of support. So working with a mortgage broker that has a good support system, good process, [and] good pricing is way better than working for a retail lender.

CK: Who are your major wholesale partners, and what about them makes it easier for you to work with them?

Nguyen: Rocket Mortgage. We receive a lot of support from them – good pricing always, they have no early payoff penalty fee, underwriting support, no extension costs. There are a lot of perks they give us, and it’s in the contract. They have Pinnacle partners – I believe the top 15% of brokers would get better pricing.

CK: What kinds of products will gain traction in 2023?

Nguyen: I think right now, non-QMs are pretty popular. The newly released Freddie Mac’s Home Possible mortgage and Fannie Mae’s HomeReady mortgage to help first-time homebuyers and low income borrowers will become popular. Fannie Mae and Freddie Mac are helping people with low income, so I think that will become popular, as it will benefit a lot of people.

CK: Mortgage rates are expected to go down, but expected home sales numbers aren’t encouraging. Are you still hopeful about seeing an uptick in housing activity?

Nguyen: I think we are already starting to see that with rates starting to decline [as of] two, three weeks ago. I think we already hit the bottom. That’s why I feel optimistic. A lot of people can still afford and qualify. They’ve been waiting, so early next year they’ll jump into the market.

CK: With mortgage rates expected to drop to 5% levels, some LOs expect refi activity to go from homeowners who locked in rates at 7% levels. Is this in line with your expectations for next year?

Nguyen: No, because not many people took out loans at that rate. There weren’t a lot of transactions during that period, either. Plus, if their loan amount is small, what’s in it for them to refinance? So I don’t see a lot of support for that. It has to be purchase-heavy for sure next year.

CK: For those LOs that will be sticking with the industry, what strategies should they be deploying?

Nguyen: It’s all about relationships with family members, friends, [and] realtors, so focus on that and social media. There are so many loan officers, but only some will be successful. LOs will have to spend a lot of time on marketing on social media. Loan officers have to let the public know who they are and why they are good. They have to educate the public.

It takes a lot of effort, and it’s important to choose a good partner. If you don’t have a good system, good pricing, [and a] good process in place, how can you compete? It’s all about technology and pricing. Consumers got hit with high rates. They want to shop around. So if you work for a retail lender with high rates, how can you win? How can you get the customers? That’s why I say in the next year, you will see more consolidation, more retail LOs joining the broker channel.

Source link

UWM’s Mat Ishbia is reportedly purchasing the Phoenix Suns

Ownership of the Phoenix Suns basketball team will soon be switching hands. Billionaire mortgage executive Mat Ishbia is finalizing a purchase of the Phoenix Suns franchise in the near future, according to ESPN reporter Adrian Wojnarowski.

Ishbia is chairman and CEO of Michigan-based mortgage lender United Wholesale Mortgage (UWM). He purchasing the franchise, which includes the Phoenix Suns and the Phoenix Mercury WNBA team, from Robert Sarver.

The Suns franchise was put up for sale by Sarver earlier this year after a tumultuous year for the current owner. Sarver was fined $10 million and suspended for one year following the NBA’s investigation into the owner’s workplace conduct — which stemmed from allegations of a culture of intolerance, harassment, discrimination.

The total purchase price has not been made public yet, but is likely to be one of the largest NBA team purchase prices in recent history. Per Wojnarowski, the Suns deal is expected to close in the “near future,” and he said was priced in the neighborhood of $4 billion.

Ishbia joined UWM in 2003 after graduating from Michigan State University, where he was a walk-on player for the men’s basketball program under Head Coach Tom Izzo. The UWM CEO was backup point guard from 1998-2002 and won a national championship.

This isn’t Ishbia’s first attempt at purchasing a professional sports team, nor is it UWM’s first ties to college or professional sports. The UWM executive has pursued the purchase of a number of NBA and NFL teams in recent years, although none of his prior attempts were successful.

In June 2022, Mat Ishbia and his brother, Justin Ishbia, who owns 22% of UWM, were among four finalists in a bid to purchase of the Denver Broncos, which had been up for grabs since February 2022. Other finalists included Josh Harris, owner of NBA Philadelphia 76ers and NHL New Jersey Devils; Rob Walton, son of Sam Walton, the founder of Walmart; and Jose Feliciano, co-owner of Clearlake Capital.

The Broncos were ultimately sold to the Walton-Penner family ownership group for $4.65 billion in August 2022.

Justin, a founding partner in Shore Capital, will make a significant investment and serve as alternate governor, Wojnorawski reported.

In 2021, UWM was announced as the jersey sponsor for the Detroit Pistons basketball team. The financial terms of that deal were not disclosed to the public.

UWM is also a frequent sponsor of Ishbia’s alma mater. In 2021, Ishbia made a $32 million donation to Michigan State for a new football building. Later that year, the CEO announced that UWM would sponsor all men’s basketball and football players with $500 dollar monthly stipends in return for the players advertising UWM on their social media pages.

The majority of Ishbia’s wealth is tied up in UWM, which as of Tuesday afternoon had a market cap of about $6.44 billion.

A spokesperson for the lender did not immediately respond to a request for comment.

Source link

Homebuilders are leaving the cupboard bare for tomorrow

Single-family homebuilders are pulling back in a major way. The downward trend overall in new housing starts continued in November, dropping 0.5% from October to a seasonally adjusted annual rate of 1.427 million, according to a report released Tuesday by U.S. Census Bureau and the U.S. Department of Housing and Urban Development.

November’s annual housing start rate was down 16.4% on a yearly basis, reflecting the continued decline in homebuilder confidence and middling sales activity.

“November continued to see a slip in home construction activity, despite inflation cooling off and mortgage rates falling,” Nicole Bachaud, Zillow’s economist, said in a statement. “Even though the cost of borrowing is lower than it was a month ago, affordability is still a major concern causing many potential home buyers to stay out of the housing market.”

A sizable decrease in single family starts was the main culprit in the overall slower pace of homebuilding. In November, the single-family sector posted a 4.1% monthly decline and 32.1% yearly drop to a pace of 828,000 units. The multifamily sector, on the other hand, had a strong month with starts increasing 4.8% from the month prior and 24.5% compared to a year ago, to a rate of 584,000 units.

Regionally, housing starts were down month over month in the Northeast (-18.6%) and Midwest (-16.5%), but were up 0.1% and 8.3% in the South and West, respectively. On a yearly basis, housing starts were down in all four regions, with the largest annual drop coming from the Northeast at 27.2%.

While housing starts mostly held steady on a national basis, the number of building permits issued to homebuilders represented one of the largest monthly drops in the past decade. In November, the number of building permits posted an 11.2% monthly decline and 22.4% year-over-year drop to a pace of 1.342 million. Large declines in both the single-family and multifamily sectors contributed to this drop, with single-family falling 29.7% and multifamily dropping 10.7% year over year, to annual rates of 781,000 and 509,000, respectively.

“It’s not easy for builders to balance the short-term pullback in demand with the long-term need for more housing nationwide, but on the surface it seems a more reasonable strategy would be to pull back on short-term starts and keep the longer-term permit pipeline as full as possible,” Neda Navab, the president of U.S. regional operations at Compass, said in a statement. “That homebuilders have instead taken the opposite path – clearing out those homes already permitted, but leaving the cupboard more bare for tomorrow – does not bode well for a nation that remains under-built after an anemic decade following the 2008-era housing crash.”

“While it may only take a few months to complete a home once work on it has begun, in many areas the permitting process that precedes any actual construction work is an exceedingly complicated and expensive process that can take years to play out. Securing permits today may enable many builders to then begin work tomorrow when conditions are more favorable, and any reasonable policy improvements designed to make the permitting process smoother should be welcomed,” Navab continued.

On a most positive note, completions by homebuilders were up 10.8% month over month and 6.0% year over year, with the single-family sector reporting a 9.9% yearly increase to a rate of 1.047 million. The multifamily sector, however, was down 3.2% compared to a year ago, to a rate of 430,000.

“Homebuilder activity from months past is finally paying off, an increase in the number of completions in November, and an increase in single family completions specifically, will help to boost the inventory starved market this winter,” Bachaud said.

Odeta Kushi, deputy chief economist at First American, said the housing market remains structurally undersupplied, “but we’re at a point in the housing cycle where demand has pulled back swiftly and inventory may rise as homes sit on the market longer. Increasing new-home completions will be beneficial to the market in the long-run.”

Source link