Support the relief efforts for the Maui wildfires by donating to the organizations below or clicking here. Together, we can make a difference for those affected by this tragic event:

David:

This is the BiggerPockets podcast show 804.

Rob:

A lot of people get stuck mingling with the same person and it’s a little awkward to leave, and you’re just chatting with someone for like 15 minutes, but you know you have nothing else to talk about, in and out. “Do you have a deal? No. Great. Hey, nice to meet you, man. Have fun at this meetup.” Next.

David:

Yeah.

Rob:

Boom. “What do you do? Wholesaler? Great. That’s exactly what I’m looking for. You on Instagram? Let me get your Instagram.” Boom. Move on to the next one. If there are 200 people like there were last night, if you only met 20 of them, you didn’t do your job right. You need to meet all 200 as fast as possible and see who can serve you because you’re there for a purpose.

David:

What’s up, everyone? This is David Greene, your host of the BiggerPockets Real Estate podcast coming to you live. Well, not really live for you, but live for us.

Rob:

Yeah, live for us. Well, every podcast is live for us if you think about it.

David:

Yeah. Why do we always say coming to you live? What could you say instead? Coming to you previously recorded.

Rob:

We’re coming to you pre-recorded from live in Los Angeles.

David:

Downtown LA at Spotify Studios where we are recording, and we got an update today with three of our former guests. They were the mentees from previous episodes and we’re getting a little update. Rob, what should our listeners look for to help them with their investing journey in today’s show?

Rob:

Yeah, so it’s really fun to examine the journeys of our, I call them our little fish. They’re out there, they’re doing their thing and it’s really great to check in with them. But one of the things that I saw was that they had these big goals, but not necessarily steps or an action plan to achieve those goals. And so I think that is going to be huge because I basically gave them the advice to just make sure that you’re intentional with every single goal that you set. And so I think hopefully that opens up the eyes of some of the people at home that have realized that they’ve set these lofty goals, but they’re not actually giving themselves deliverables that will keep them accountable towards hitting those goals. You know?

David:

That’s a great point. Their motors were revving, but they didn’t know how to put it in gear.

Rob:

Yeah. [inaudible].

David:

In today’s show, we gave some practical steps that they can use to get their motor in gear. We also talked about the market, how maybe we’re being too picky, delaying gratification, the wrong mindset with real estate, how to make money in ways other people aren’t seeing and why house hacking could make people millionaires if they could just get over the stigma of thinking that they’re above it.

Rob:

I love it.

David:

All that and more on today’s show, so make sure you listen all the way to the end to hear about a sneak peek from a book that I have coming out in October that you won’t hear anywhere else. Very quickly, before we get to today’s show, our quick tip is going to be we tell you all the time to go to real estate meetups and you should, but how you go makes a difference. Rob gives some great advice to Philip today about how you should approach a meetup and a way to make sure you get the most value possible, and then I give some practical steps of how you can accomplish that. So your quick tip is to go to meetups, but don’t just show up and expect something to happen. Go there with a plan and work your magic. All right, let’s get to the show.

All right, welcome back to the show, Philip, Wendy and Danny. For those who didn’t know, Philip, Wendy and Danny were initially part of our first ever 90 day mentorship program earlier this year. You can catch updates on their progress from episodes 708, 719, 726 and 738. We’re here today in person, so nice to meet all of you guys and gals in person and talking about what’s been going on in your life. So let’s go around and get a quick update on what’s been happening since we’ve last heard from you. Give us the highlights. We’ll start with you Philip.

Philip:

All right. So my wife and I, we were on the hunt for land to build out a wellness retreat center for almost a year. And about a month and a half ago we got 20 acres outside of Santa Clarita and we’ve been in the mode of what is the build out going to be like. And it’s raw land, so how many things would you like to know about digging a well? I know a lot more than I used to. And yeah, financing that and the business plan for that. So that’s been super exciting.

And then I also, after 14 years in the classroom, I decided to leave teaching. It was, let’s say I’m not at the place where I had replaced my income, but I just felt like it’s time for me to go and to really give my focus and my attention to something that I think has no ceiling to it, which is these different projects that I’m in. And then, yeah, I’ve been raising money for flips. I have a active flip right now in East LA and then different partnerships where I’ve been raising money for long-term holds and pad split and some of these other kinds of ways where I can be parts of deals while the retreat center is in its baby steps, taking its baby steps.

David:

There you go. Thank you. Danny?

Danny:

Yeah, so when last we talked, I was on the hunt for a 10 to 20 unit multifamily in Sacramento to kind of beef up my portfolio and go to the next level. Since then, I had a lot of good momentum after the podcast, everything was recorded, a lot of folks reaching out and looking to get some stuff done, but work kind of took a really hard pivot. I don’t know if you’re familiar with the tech industry, there’s a lot of uncertainty, a lot of things going on, a lot of folks losing their jobs. I have in my company in particular, I just kind of said, “All right, let’s focus real hard on the job and preserving that because that’s the thing that still pays the bills.” We went through some layoffs and different changes and such.

So I had to really spend my time on there and that left very little time for real estate. And I was really dead set against not take carving out from the family time. So something had to give and the real estate time did do that or wound up suffering as a result. But what I learned from that is that I was able to even think of more ways that I can squeeze more time out. So I have all these properties that I’m currently own and running. I was digging deep into how do I figure out how to leverage my time better. Can I give more tasks to other folks?

I had one of my sweat equity partners, I had him take over the day-to-day operations of the property, so that way I’m not the first line of defense when property manager calls and says, “Hey, we need a repair” or “we need to fill this vacancy.” I’m now out of that loop, freeing me up for more time there. I started leveraging my virtual assistant even more, so freeing up more time in terms of making more phone calls, getting her to manage my schedule and my emails and kind of things that need to be done but didn’t necessarily need to be done by me. So that I look at as a positive. Keep thinking about ways to improve my business and to also elevate myself and take myself out of the business more and still have it run successfully.

David:

Awesome. Wendy?

Wendy:

I would say the last six months, four months maybe, for me have been about three things, stabilization, systemization and then prioritization. And I’ll start with stabilization because I came into this year with eight properties that I’d purchased since 2020, and a lot of them were in a state of just trying to still figure out were they rented, did we have good tenants in there, how was my property management company performing and were we making money. And as it came down to it, I had one property in Ohio that was a duplex and I had a very bad property manager there who was really not paying attention to me at all or to the properties, and so I had an almost eviction there. Luckily we got the person out before we had to go through the legal process because that’s always a challenge.

Then on the other side in Baltimore, I have four properties there. Three of them were humming along pretty well, but the fourth one, the property manager put a real loser in there unfortunately in January and he never paid rent. And I tried to get them out ever since January and I’m still to this moment trying to get him out. So we are in the eviction process. Baltimore, you have to take them to court five times.

Rob:

Wow.

Wendy:

Yeah. And the tenant has the ability to pay each time. And so you’re only going to ask them to pay for a portion of what they owe, like last month’s rent. And so each time if he just pays $1,400 he can stay, but he already owes like $3,000. And then to top it off, the property management company accepted a check which then bounced. So then we had to start over. Anyway, so stabilization, just making sure that I have enough funds in the bank to manage the issues that I’ve had.

I’ve had an HVAC that went south, I had to deal with that and that was a third property manager. And they don’t do the hard work that you would, or you or I would, on a property. You have to say, “Did you get three bids?” “Well, no. We use this vendor all the time.” “Well, I’m sorry, that’s not good enough. I’m not ready to just give you $6,000 for a new HVAC. Let’s please back up and get a couple more bids.” And in the end, that saved me. Now I only had to put out $1,200 and it’s going to last me for another eight or 10 years. So that’s stabilization of existing things. Firing two property management companies, getting two new ones in there, trying to get all of my properties humming along well.

Systemization is just squeezing the profits out of what I’ve got. And I’m doing a cost segregation right now on all of my units, which is going to save me 12 or $13,000 just in 2022 taxes. And then ongoing, I’ll have another a hundred thousand supposedly or so that I will be able to take off of my W-2 income going forward. So that’ll bring more profit into my life that I can use for more real estate of course.

And then prioritization. So that’s where we started with this podcast. And that is how do I select where I’m going to go next? I looked at Las Vegas, I didn’t find what I wanted there. I’m now looking at Long Beach. I maybe want to do a house hack somewhere. I was looking at Las Vegas and that didn’t really work out for me as far as midterm rentals or the long-term rental wasn’t working, but midterm rental did, but I just didn’t feel comfortable with that. So I’m still stuck at the stage right now where I’m looking for what’s next to invest my money effectively.

Rob:

Cool, cool. So Philip, can you tell us for old times sake, is there a hurdle that you’re currently facing that we could help you with?

Philip:

Yeah. A lot of the seeds that I end up planting are seeds that are long-term kind of seeds, that I feel really good about more and more as time goes on, but I definitely need to, the retreat center or some of the things that I’ve partnered on, there are things that we’re holding that even five years from now I’m going to feel really good about, but I definitely need to increase my now income so that I don’t have to feel like I’m in a rush with any sort of investments that I make or any sort of deals that I get involved in. And yeah, yeah, I think that’s a big one.

Rob:

Yeah. Okay, so let’s talk about that. So you said that right now you quit your job, you’re flipping homes, that’s how you’re making money, and then you’ve got this retreat that’s an iron in the fire, but not going to really come into fruition for a little while. Right?

Philip:

Totally.

Rob:

So if you’re already making money one way, and if I remember correctly, you’re pretty good at it, you’ve been successful, you’ve made money from flips, it sounds like we need to supercharge that to get you through the development. Right? So what is holding you back there?

Philip:

I think it’s been the consistency of reaching out to agents and building up my deal flow through agents and wholesalers, and that is something that I’ve been actively working on. Okay, every single day I’m reaching out to 10 potential lenders on deals. That’s one side, the money side. And then I think supercharging my agent reach out and my wholesale, networking with wholesalers to really get that deal flow. I actually had a great conversation with someone from the Greene Team yesterday that is right in my Goldilocks zone of the types of projects that my partner and I would be willing to take on. So I think I’m in the process of it, but that’s definitely, if I was going to say, do I feel great about the deal flow that I have right now for those kind of projects that we can go full cycle in a six-month period, I’m not happy with it. And that is an area of growth that I think will help my success a lot.

Rob:

Great. So for everyone at home that doesn’t know, deal flow is effectively the pipeline that you have built that effectively will lay deals out in front of you. How often are deals being sent to you from other investors, wholesalers, people in your network? You’ve been working on this. I am curious, because we did go to a meetup last night, how many meetups have you gone to in the last six months, would you say?

Philip:

I would say I usually go to one a week, but definitely that’s on my list. You need to be going to at least two or three a week because even just the one a week that I’ve been going to, I’ve met potential partners, I’ve gotten actually a deal that I’m going to be partnering on that we worked out the terms this morning. It was from a meetup, somebody that I met at a meetup and that I feel good about. We’ve had a few different meetings. And yeah, I know that your net worth is your network. That is definitely coming through for me. But there’s an aspect of okay, I need to make certain sacrifices with spending time at home, which in the evenings, that’s when I would be spending time with my family that I think it’s a sacrifice that is important for me to make right now.

Rob:

So do you have a clear goal or a clear deliverable that you expect leaving a meetup? When you go to a meetup, are you telling yourself if I don’t leave with this one thing, going to this meetup was a failure?

Philip:

Every single meetup that I go to, I’m looking for potential partners for a deal flow or for private lending, every single one.

Rob:

So that’s a good goal, but do you have an actual deliverable for that goal?

Philip:

I haven’t had a specific number attached to that and maybe that’s good advice. I’m going to connect with four awesome people and exchange contact, and I’ve been adding people to my CRM and even learning what a CRM is. And okay, what does my follow-up system look like? Those are all things that, those were just vague ideas in my head before I left teaching. “Oh yeah, I’ve heard about a CRM, a follow-up system,” but what does that actually look like? How many days until I meet someone, am I going to reach out to them? What is the conversation flow going to be looking like? And that’s definitely something I’ve been working on and developing.

Rob:

Yeah. So you just laid it out for me. So your goal is, “I need more deals.” Now you have to actually put steps in place. Going to a meetup is one step, but now the goal of the meetup is, “I want to get four leads.” Right?

Philip:

Yeah.

Rob:

That’s your deliverable. And if you don’t get four leads from it, you have failed. So you should have some kind of number or some kind of metric that you’re actually working towards. And so if you’re saying, “I want to leave with four contacts,” great. Then you need to make sure that you are being super intentional with the people that you meet when you go to a meetup and you’re not there just chatting, making small talk. If you’re not connecting with someone, if they don’t have a deal to give you, move on.

A lot of people get stuck mingling with the same person and it’s a little awkward to leave and you’re just chatting with someone for 15 minutes, but you know have nothing else to talk about, in and out. “Do you have a deal? No? Great. Hey, nice to meet you, man. Have fun at this meetup.” Next.

Philip:

Yeah.

Rob:

Boom. “What do you do? Wholesaler? Great. That’s exactly what I’m looking for. You on Instagram? Let me get your Instagram.” Boom. Move on to the next one. If there are 200 people, like there were last night, if you only met 20 of them, you didn’t do your job right. You need to meet all 200 as fast as possible and see who can serve you because you’re there for a purpose. David, what do you think?

David:

Perfect advice. I’ll give you some practical tips to help execute that better. You will get stuck in a conversation with someone and want to get out of it. This happens to me all the time. How many people were at the meetup last night? 150.

Rob:

150, 200 maybe.

David:

Right.

Rob:

A lot.

David:

And they’re all going to want to talk to me and I don’t want to be a jerk and not talk to them. But if I talk to everyone and answer every question, they’re just going to keep throwing them at me, then I can’t meet the next one. So you have to look like a jerk to one person to not be a jerk to the whole group. There’s no way around it. So what I’ve learned how to do is say, “I have to get out of this conversation, but message me on Instagram. Send me an email.” I give them some form of follow-up so that it doesn’t look like you’re not important to me, you can’t serve me, like what Rob said. Because you do need to see who can serve you, but you don’t want to come across a self-serving person. You have to balance that thing.

Rob:

Absolutely.

David:

So get their information and say, “Hey, I’m going to reach out after this is done and we have more time to talk. I’d like to help you with,” fill in the blank. That’s another thing I’ll do.

The last piece is you can say, “What do you do?” You’re looking for a wholesaler. They’re not a wholesaler, okay. They’re a construction person. You don’t need a construction person. I would say, “What would help you in your business?” And they’re going to say, “Leads, I’m here to find people that want construction work.” “Okay, let me get your contact information. I’ll pass that along to other investors I find that need that. I need a person that can find me deals in East LA. If you were me, where would you go?” Because they might not be the wholesaler, but they may know the wholesaler.

Rob:

They might know a wholesaler, exactly.

David:

They might walk you over to the wholesaler, they might tell you about their wholesaler, they might say, “Oh, this agent on the David Greene Team crushes it. They’re working on a flip for me. I can introduce you to them.” It’s good to ask what they do, but it’s also good to ask who they know that could help you.

Rob:

That’s a great, that’s a very good supplementary. It’s not just that person, they probably have a whole Rolodex of people. If they’re an investor, they know other investors, they know other contractors, they know other hard moneylenders, they know other operators in the area.

Philip:

Yeah, I think that’s great advice. I love the idea of, “Okay, how can I be of service to you in your business?”

David:

Start with that.

Philip:

“And if there’s a way that you know if there’s someone in your network that can help me with X, I’d love to connect with them.” I had this conversation with Amy Marjorie because I’m in her Mastermind.

Rob:

Yeah, love Amy.

Philip:

Yeah. And it was similar sort of thing where I was talking to her, I was like, “Yeah, I’ll have these meetings with people and then it’ll be like 45 minute meeting where I’m trying to become, I find myself thinking how can I become this person’s best friend so that we can partner and this is not the right relationship for that.” This is like, “Let’s find if there’s a way that we can be in alignment, and if not, I wish you the best and if there’s any way that I can be of service in the future, let’s talk.”

Rob:

Yeah.

David:

Yeah, start with that. What could I do that would help you? Some people, I’d say the majority of them, don’t even know what they want. They’re like, “I’m just nervous. I don’t know anyone here and I feel like everyone makes more money than me.” “All right, so you’re nervous. Okay, well hey, hang on my hip and you could just follow me around and I’ll go talk to people,” or “here’s all the other nervous people, I’ll go introduce you to them.” That’s okay, you’re not going to be solving high level problems for every single person there.

A lot of the time it’s everyone feels inferior. They’re all like, “I have one house” or “I haven’t bought my first house,” and they think all other 149 people are studs that just own tons of real estate and they’re the only one that doesn’t have it. And then you find when you talk to everybody, “Oh, hardly anybody here owns any real estate.” They’re all in the same boat. It’s hard as hell to find anything that cash flows. Everything’s getting multiple offers. It’s still too expensive. They’re all on the same level. So you can bond over a frustration too. It’s not always going to be a specific thing that’s going to help them in their business. Sometimes it’s an emotional thing, but you can’t, like Rob said, spend 35 minutes talking to that one person.

Philip:

Yeah.

David:

Because you finally got comfortable and built rapport and then you don’t talk to the other 149 people that might help you.

Rob:

Or if they are one of the links in that chain, be like, “Hey, let’s go meet other people. Come on, come with me.” That way they can add to the conversation too. I think you can even be more upfront, more direct. You seem like someone that can do this. Wear a shirt that says, “I’m looking for deals.”

Philip:

I actually have a shirt that says yeah, “I am offering double-digit returns for private investors. Are you down?”

David:

That’s from Amy, right?

Philip:

It’s from Amy, yeah, yeah.

David:

Somebody was wearing one of those at our meetup last night.

Philip:

Yeah, he’s a good friend of mine. Yeah, yeah.

Rob:

But see, that’s solving your money issue.

Philip:

Totally.

Rob:

But it’s not solving your wholesale, finding wholesale deals [inaudible]. Yeah, so switch it up. I’m looking for deals.

Philip:

Yeah, I like that.

Rob:

I mean, if I saw a guy that was doing, I’d be like, “Hey, if I have a deal, I’m going to go to the guy that says, ‘I’m looking for deals.’”

Philip:

Here’s my deal criteria.

Rob:

Yeah.

Philip:

Have my buy box on a shirt.

Rob:

Yeah, print out sheets. Here’s my buy box on this sheet. Give it out to people. I think just be intentional. Don’t just go to chat. If you’re going to chat, you’re not going to get what you need, but if you go with something that you really need, then you can form creative ways to get exactly what you need out of that meetup.

Philip:

That’s definitely with the land, there was something about sharing the buildout of the wellness retreats on the land where people would just start to, “Oh, I could help you with this. I could help you with this. Oh, these are the ways that, oh, do you need a contractor? Do you need somebody that builds platforms? Do you need a lender? Do you need a well person?” All of this stuff, people would really start opening up their network when they knew that I had a raw piece of land that I needed so much assistance with it and I could see the same thing being true for other kind of deals.

David:

[inaudible].

Philip:

Yeah.

David:

I mean, that’s advice for everyone in general. Right? What stops us from being direct is fear of rejection. If you can master your fear of rejection, you can get very far.

Rob:

We get rejected every day.

David:

Yeah, we do.

Rob:

But it doesn’t hurt anymore.

David:

Yeah. I’m still trying to be Rob’s friend, he rejects me, but I haven’t quit.

Rob:

On Facebook, I’m like, “Do not accept.”

Philip:

That was actually one of the things when I was, because we bought the land with private money, and I got at least 20 nos of people that are like, “Oh, I’d love to,” or “Let me get back to you,” or actually this, and it’s like I just started getting into a flow. Oh, I’m so much closer to a yes now, I’m getting closer to a yes. And eventually we raised the whole amount all with private investors, but I got so many nos. And yeah, this is a good learning experience.

David:

What can our audience do to help you with your problems?

Philip:

Yeah. If folks that are down to partner on deals that they want double-digit returns, hit me up, see if there’s a way that we can be in alignment together. I’m doing shorter deals like flips in LA and then I’m also building out this retreat center outside of LA and really excited about it. We’re doing a lot of natural building techniques for the build out, really trying to be mindful of our impact on the land and do this in a really sustainable way. So folks that are interested in natural building techniques for the land, we definitely want to grow our community. And yeah, for folks that just want a solid investment in LA, let’s talk. I’m down to work with people of good character.

Rob:

All right, so that was four or five things you asked for when you just told us that the thing you need are more wholesale deals.

Philip:

That’s what I also meant to say, actually I want more…

Rob:

If you’re a wholesaler in LA, send Philip your deals because he’s actively looking for a flip in Los Angeles, California.

Philip:

Rob said it perfect.

Rob:

Boom.

David:

Great coaching there.

Rob:

Thank you. Thank you.

David:

Abasolo.

Philip:

You’re live coaching.

Rob:

Love it, man. Thank you so much.

David:

Danny?

Rob:

You know I’m just giving you a hard time?

Philip:

No, no, I appreciate it.

David:

Pass the mic here. Danny, we’re moving on to you. Is there a hurdle that you’re facing that we can help with?

Danny:

For me, recently, as I’ve been revisiting my business plan and the environment, the real estate environment that I made this in several years ago is very different than the one we’re in today. So one of the foundations that I built that upon was this idea of a 10-year plan. So when I acquire property that needs some love, go and put in as much of the work as possible upfront, fix everything. Ideally, I want to cashflow it for 10 years without really much involvement for me and active participation. I don’t want toilets to be breaking and that kind of stuff as much as possible.

In this environment, that means it’s very hard because of the interest rates and the lack of deals to underwrite something like that where there’s a big upfront cost to doing something like that. I got to go deal with the roofs, I’m going to go change the toilets. Maybe they don’t need to be changed right now, but maybe in a couple of years they will be. So I’m going to go and do that upfront. I’m going to go change the blinds, go deal with the windows, all these different things.

David:

Is that because you’re doing that when you have time or because you just don’t like it hanging over your head that it’s going to come up later?

Danny:

It’s exactly I don’t want it hanging over my head. I want it set it and forget it type of deal. Which in this market, in this environment today, that makes a deal even harder to come by. So I guess my question for you both is around should I be revisiting that? Should I change my expectations? Is there a dial I can change? Do I just deal with the major systems? Maybe I look at the roof and a couple other things, but the smaller things I kind of step away from or let those happen as they do? [inaudible].

David:

Let me ask you a question. Do you think we’re too picky as real estate investors in today’s market?

Rob:

Yes, totally. Because well, picky on one particular metric, which is always cashflow. That’s what it feels like. So overall, I think the more experienced you get, sometimes it is, you get a little bit picky because you know what you’re good at, you know the deals that have worked for you and that’s always the kind of deal that you’re trying to start.

David:

What about your experience coming from a market that is different than the market you’re in? So there was a time where you’re like, “All right, I want cashflow. I want to buy below market value. I want to buy in a good market. I don’t want CapEx that’s going to pop up later. I don’t want a headache tenant.” We were really screening every property until we found one that hit four out of the five boxes that I just mentioned and we knew that was the deal. Well, in today’s market, what if you can’t even find one box? You’re like, “Oh, well I got one that has two, that looks great, but compared to what we used to buy, this is crap.” Do you think that might be playing into our analysis is that we are subconsciously comparing the deals in today’s market to the deals in yesteryear and they don’t look as good?

Rob:

Oh, absolutely. Yeah. I mean it was easy, or it was easier over the last 10 years. And now it’s harder and because it’s harder, you’re not finding deals that line up with the old deals, so it’s like, “Oh, I might as well sit and wait.” I think it’s kind of what we’re seeing a lot right now.

David:

I’ve played this game with myself because I’m trying to play with my own head so that it doesn’t trick me into saying the market’s terrible because look it used to be better. What if I fast forwarded 30 years and we just never really built houses because of government regulations, restrictions, builders didn’t want to go build, people live in public housing type of a thing. And owning a house at all is a big sign of wealth. That you have real estate that you were able to get. The government could get rid of Fannie Mae, Freddie Mac loans, we could get rid of subsidized housing. Everybody’s got to go in there and put 20% down or more to get a house. We haven’t built any. People that own real estate over time become wealthy, but there isn’t any more FHA 3.5% down. Do you think in that scenario, the deals that we’re looking at right now don’t look so bad?

Rob:

Yeah, I’d say so.

David:

What do you guys think about that perspective? That it could be worse. If it got bad would I look back and say I had opportunities right now, but they didn’t look like opportunities or do you think that that’s dangerous to think that way?

Danny:

Yeah, I think one of the tenants things that keep coming up for me is it’s always better, was it’s best to buy real estate yesterday, it’s good to buy it today, it’s always going to be better than tomorrow. Something around those lines. So I think it’s always your advantage to buy something and keep things moving.

David:

So it’s about delayed gratification. We didn’t have to experience delayed gratification five years ago, 10 years ago.

Rob:

Yeah.

David:

You got immediate gratification and then you got a delayed benefit too.

Rob:

Well, to even put a little bit of context, three years ago, you could buy a short-term rental and get a 30, 40, 50, 60, some of my deals, 90% cash on cash return. And so now when you look at deals today that are at 10%, which is an outstanding return.

David:

Compared to everything else.

Rob:

Compared to everything else, it’s like, “Oh, I don’t really, I don’t know, 10%.” And I will also say that way too many investors are trying to get rich, but they’re not thinking about getting wealthy. And what I mean by that is they’re so focused on money, “I need the money now,” stop trying to get rich off of real estate.

David:

It’s the delayed gratification.

Rob:

Yeah, it’s delayed. I mean it’s like you always say this with CapEx and cashflow, especially on long-term rentals, if you take from your own cashflow, you’re sort of just borrowing money from yourself because in five years you’re going to replace that AC and it’s going to cost like 5,000 bucks. It’s going to be the $5,000 that you use to pay yourself. So you might as well just forfeit the idea in most cases. Right? I know your strategy is a little different, Philip, you’re flipping, you’re using money now. But in most cases from a rental perspective, forfeit the idea that you’re going to make money today, but 30 years from now, you’re going to be like, “Holy hell, I got that property for 20% of what it’s worth today.”

David:

And now it’s paid off and I had tax benefits. And cashflow does increase over time. We always forget about that. Think about properties you bought seven years ago. What’s the rent like now compared to what it was before? But it’s all delayed gratification and I think people are really struggling to swallow that pill right now. That it used to be an embarrassment of riches. We had all these deals we could look at, they all cash flowed. It was what’s the best of the best. And now it’s man, if you compare real estate to anything else, it’s still better, but it ain’t as good as what it used to be. And it is going to be work. It’s not passive anymore. You want to be a short-term rental operator, a midterm rental operator, you really got to put some effort into running this project, which people got used to thinking that it should just be like mailbox money, just shows up.

And now there’s an adjustment, I think people are having a hard time accepting it. But I’ve seen that pattern before. Long distance real estate investing was a hard pill to swallow for a long time. I had a bad reputation as the guy telling people to, it was heresy to say buy in another area instead of buy in your own backyard because it was risky. Now, we will do that all the time. What’s the next emerging market? Where do I go? Rob’s got properties all over the country. You don’t even think of yourself as a long distance investor. You’re just a real estate investor and you go to where the deal is.

Rob:

Yeah.

David:

But there was a time that was tough to accept. I think right now, people are struggling with the dream of I could buy cashflow and quit my job in two years is not very likely. I know I kind of took us off that path there.

Rob:

No, but it’s a good thing. I think we need that refresher every so often, that it’s like wait, just wait. The wealth and the money will come, but the first five, 10 years, you’re just going to school.

David:

And that’s like everything else, man. You start a business, no one expects to crush in a business when they first start it. They tell you that you’re going to build a five, 10 year period of time. You want to go start a dry cleaning business, you’re going to be building a customer base, you’re going to be working on systems, you’re going to suck at hiring, you’re going to have all these problems and then eventually you’re going to figure it out and your business is going to be profitable. I think we have to look at real estate the same way. So with that in mind, is there any other hurdles that are popping up as you’re thinking that we can help you with?

Danny:

Yeah. I’ve been thinking also when I set the goal during the mentorship, it was 10 to 20 units, I was very focused on that. And I still think that’s my main focus, but I’m thinking just based on the type of lending and mixing it up a little bit and my experience, it might be good to get some base hits. So maybe some four units, which are definitely a lot more plentiful in the Sacramento area. Should I divert some of my energy and my time to getting some of those under my belt? And just I want to keep things moving and make sure that I keep moving forward.

David:

Let me give you some advice before we move on to Wendy, what you could do. I’ve mentioned about this framework that I’m working on on a book that’s the 10 ways you make money in real estate. We’re talking about one of them, which is called natural cashflow. Everyone’s used to analyzing for that. If you can’t get it, which right now is very tough to get, make up for it in some other way. Don’t just buy real estate just to buy it. So if you can’t get cashflow, it doesn’t make sense to buy a breakeven property in Gary, Indiana that it’s never going to go up in value, the cashflow is never going to increase. Maybe it makes sense to do that if you’re getting cashflow right out the gate. If you take that away, you got to make up for it somewhere else. So if you’re buying in Sac, I would look for something you could buy under market value, that’s called buying equity. I’d look for something you could force equity to, cosmetic upgrades, adding square footage to make it worth more.

I’d look for a way to force cashflow. So this is a method where we buy a property, we build an ADU, we convert something into an ADU, you take a basement, develop it, rent that out. It didn’t cashflow as it was, you added value to it and now it forces cashflow. Now, maybe it does. And then market appreciation equity and market appreciation cashflow. Is Sacramento market that you believe will go up over time faster than other options? Do you believe rents will increase faster than other options? Do you see businesses moving there? Do you see higher paying jobs moving into that area? Fast-forward five years, that’s a really big chunk of money that you can make versus if you bought in, I’m using Gary, Indiana as a stereotypical, please, all the Gary people don’t email me with anger. Maybe it’s a great market, but in my mind, a market that isn’t going anywhere, just kind of stuck in time. If it is a market like that, you can buy there and it looks like a boring deal and in five years it looks like a great deal, in 10 years it looks like a home run.

Rob:

Yeah. I do want to add just your question specifically, and I feel like I’m channeling my inner David Greene metaphors here, but if you go to the gym every single day, every single day, two months from now, three months from now, let’s say you did it every day for six months. By the end of the six months, you’re going to be in shape, your endurance is going to be up, you’re going to be lifting heavy weights. And then let’s say that you stop going to the gym for a year. Can you go back and do what you did before? No, you have to work your way back up. And so to me it sounds like you’ve lost your momentum a little bit. Life gets in the way. That’s fine. That’s a very real thing that happens in real estate. Nothing wrong with it. Life holds me up all the time.

Your momentum, the train has stopped and so now you’re trying to get back to this huge goal that you set for yourself. But it feels so difficult to do that because you haven’t been in it. You haven’t been in the nuts and bolts. You’re a little rusty. So the answer is I do think a base hit is fine. I do think a four unit is fine. Because then you get into this deal, you negotiate with the agent, you get it accepted, you go through the inspections, you close and you’re like, “Oh, that’s all right. It’s not that hard.” Then you can go for the big one. That’s my advice to you. Base hits, totally fine. One of those days, the base hits, all the bases are going to be loaded, you’re going to hit a home run and you’re going to be so happy that you did.

Danny:

I love it. Thank you.

David:

You guys want a little sneak peek from my book, “Pillars,” before it comes out in October?

Wendy:

Sure.

Danny:

Yes, please.

David:

All right. So I have an example in the book that we’re actually in a very highly inflationary environment. So our money is losing value even though we are not losing money. If food costs 15% more every year than it did the year before and you get a 3% raise at work, that’s the same as a 12% pay cut. Right? If our boss came to us and said, “I’m taking away 12% of your money,” we would have a cow. Teachers would be on strike, people would be rioting, there’s no way you’re going to take away my money. But if it comes through inflation, we don’t even know what’s happening. So I use this example that we were all walking upstairs to wealth at one point, now it’s an escalator that’s actually going backwards. And if people are standing in place, working in their job, not investing in money, not growing their wealth, they think that they’re standing in place, they’re actually going backwards. We’ve had a big run of money where the escalator was going up for the last eight years, making money was easier than it’s ever been, and we got used to that. Now we have the downside of all the money we printed, which is inflation and escalators going back.

So if you are trying to make progress, you’re now running up an escalator going down. And I had to do that a few times as a police officer. It was not the most fun thing to ever do to chase somebody going up an escalator when you’re wearing all that gear. You’re burning a lot of energy and you don’t feel like you’re getting results. That can be very discouraging. I think a lot of us are experiencing that. I’m working so damn hard and I can’t get the deals that I want. I can’t make the money. I’m not getting anywhere. But if you compare yourself to the rest of the population that’s not running, they’re all just moving backwards. They’re losing wealth, they’re losing the ability to provide in the future, they’re losing the ability to buy real estate. So sometimes we can feel like we’re not making progress, but you’re actually making a lot more progress than everyone else who’s not running at all.

Rob:

That’s really good. That’s really good. That’s in your new book coming out?

David:

Yes, it is. Thank you very much.

Rob:

When is that going to be available?

David:

Be a game changer. October 17th, “Pillars of Wealth.”

Rob:

Love it.

David:

It’s going to be…

Rob:

Promo code BiggerPockets77. Our producer’s like, “Stop doing that.”

David:

You could probably use the code David to get a code on that book. Yeah.

Rob:

Or Rob.

David:

Not available to order yet. This is going to be a book I think that changes the entire approach that we take to building wealth. Everybody’s here to learn about real estate investing, that’s what you guys are doing, that’s what we do. That alone is not enough to make it when the market’s working against you. Now you have to focus on budgeting your money, actually living within a budget, living beneath your means, which is defense and making more money. You have to approach your business like a business. You have to approach your wealth building opportunities like a business. Offense matters now. It’s not just pure buy properties and makes sense. So that book sort of shows that three pillared approach.

Rob:

Awesome. Awesome.

David:

You want to move us along?

Rob:

Yeah. Last one, Wendy, for old time’s sake. Is there a hurdle that you are facing right now that we can help with?

Wendy:

Yes, absolutely. So I feel like my real estate venture has been like a bag of marbles and I gave away a lot of marbles early on and now I’m just staring at a few last marbles that I have and my decision is difficult to make. Whereas I was very easily buying rental properties here, rental properties there.

David:

Yep.

Wendy:

Now I’m like I’ve got to really make these last ones work because I want to scale up through that process. And I know, David, you were really adamant, and rightly so, that I should look at house hacking and I want to look at house hacking desperately. So my challenge though is identifying this buy box as to where I should do this house hack. I know the things that I do want. I want it to be a multifamily or available to be some kind of a multifamily, an ADU. I would like to do either a house hack within the house or house hack in a quad somewhere. And I’ve just been struggling to pick the right market and that’s really where I’m stuck. And yeah.

David:

How many markets are you looking at?

Wendy:

Well, let’s see. I looked at Vegas and now I’m thinking maybe Reno, but I haven’t looked at all in Reno. Kansas City has got some hospitals going to it. I looked in Long Beach. I live in Long Beach, I thought let’s try to make that happen. But I couldn’t find anything under a million dollars that was next to the freeway, just was never going to be anything any better. So I would love to invest in California again, but I just think that’s not maybe the right approach.

David:

What’s the reason you think it’s not the right approach?

Wendy:

Well, I don’t know. You do all your work here in California, so I know you love it here. I just feel like the taxes are so terrible.

David:

Okay.

Wendy:

It’s a terrible place to retire. I’m an old bird now. I don’t want to…

David:

So you see house hacking like you’re going to have to live in it and you don’t know if you want to live in California.

Wendy:

Oh, well, I would love to live in California temporarily as a house hack, but I don’t want to have that be my primary residence because for tax purposes, I guess, really. Tampa is one I’m looking at, San Antonio, but I don’t really know those markets very well. Or yeah, so that’s my challenge I guess I just can’t figure out.

David:

Do you think mentally you’re looking at house hacking and your primary residence as sort of like an anchor that’s tying you to a place that you don’t want to live?

Wendy:

Maybe.

David:

Could you live in California for a year?

Wendy:

Yes.

David:

Could you live in California for two months?

Wendy:

I do.

David:

So what if you lived in California, you bought a house hack, you lived in it and you decided, “I hate this place. I don’t like the smell. I’m too close to Rob Abasolo. He’s got this glow that makes me feel bad about myself because he’s just like in a glow up stage.” You realize that you can leave a primary residence after you’ve bought the house if just something came up, the lenders can’t force you to live in the house if there’s unforeseen changes.

Wendy:

Yes.

David:

So I think there may be a mental block where you’re thinking, “I don’t want to stay in California. I may not want to live here longterm, so I can’t house hack.” I would advise you buy a house hack that works for you, that would also work as a rental if you left. So maybe you love a home that has three bedrooms, but there’s another home that has five bedrooms with a dining room that could be turned into six.

Wendy:

Yeah.

David:

It’s got three bathrooms, so two people can share a bathroom. That’s a great house hack. Buy that thing with three and a half percent down, 5% down, live in it. If you don’t love it…

Wendy:

Move.

David:

Yeah. They can’t force you to live in a house that you hate. Now, don’t buy it with the intention of never living in it.

Rob:

Right.

David:

That would be breaking the law.

Wendy:

Right.

Rob:

Big mistake, for sure.

David:

Right. But if you intend to live in it and then something happens, the neighbor’s dog barks too loud, it could be anything, work wants you to move somewhere, you just feel the call of the sea like Moana and you just want to go somewhere else, you don’t have to stay inside that property. So that’s probably not as much commitment as you’re thinking. And I feel like house hacking, I know I never wrote a book on house hacking, but I’m constantly telling everyone this is what you should do. Because if you commit 20% down to a house in Vegas, like you were looking at, that’s a hundred grand on a $500,000 house. You commit 5% down to a house in Southern California in Long Beach, that’s $40,000 down on an $800,000 house. You keep way more of your capital that you can go buy something else if you don’t like it. When you’re shooting a 25% down, you have to hit your target. If you mess up, it takes forever to get that money back. House hacking really gives you a wider target to shoot at. Does that make sense?

Wendy:

Yes. But then is it better to buy in an expensive market here or somewhere where I don’t have to put as much down and I can still live there? I’m also not tied to freedom.

David:

You’ll put more down living, oh you mean house hack in a different market, right?

Wendy:

Yeah.

David:

Which one’s going to be worth more in 10 years?

Wendy:

Well, I think you guys are saying California is a winner.

Rob:

[inaudible].

David:

I’m not trying to be a home rep for California, but in general, if you have two different markets to look at, which one will be worth more? Right?

Wendy:

Well, California does tend to…

David:

Which one’s going to have higher rents?

Wendy:

California for sure. That’s the problem.

David:

Okay, so we’re saying California, but what we really mean is a more expensive market. Right? So if you can rent out bedrooms in California for what do you think you get in Long Beach per room?

Wendy:

Oh, $1,800 or more.

David:

All right. And what would you get in, let’s say Vegas per room?

Wendy:

A thousand max.

David:

Okay, so let’s make Vegas 900 just so the math is easier. Vegas is 50% of what California is. Okay, if rents went up evenly percentage wise, which they won’t, they’ll go up disproportionately more in areas that people make more money. In five years, no, let’s not even say in five years, if rents go up times 10 over a 30-year period or something, you end up with $18,000 rooms in California, you end up with, what would the, we said $900, $9,000 rooms. So you have a $9,000 difference per room times five rooms in a property. What’s nine times five? It’s 45,000?

Rob:

45,000.

David:

I’m a little tired right now. $45,000 per month.

Rob:

Per year.

David:

Per year. Thank you. That one property. Multiply that times 10 properties you bought, that’s the difference of almost half a million dollars. And that’s how the math sort of scales. So when you’re trying to figure out, do I want to go here or there, if you lean towards where rents are going to go up more and you lean towards where property values are going to go up more and then you don’t tie yourself to the property, you keep the freedom to move where you want to move, you could buy great property in California and then just live in Las Vegas. You could rent a room from someone else. You could rent a house from someone else so that you’re not tied to it. You don’t have to own the house you live in. I did that for a long time. I owned nine properties as rentals and rented a room from someone else before I ever bought a house.

Wendy:

Yeah.

David:

What do you think, Rob? You think I’m giving her bad advice?

Rob:

I don’t disagree with it. I think personally, this actually works out for you. I used to live in Kansas City. I lived there for three years and I love it and I think it’s a really great city. I think it is exploding.

Wendy:

Yeah.

Rob:

I think the values are going up, certainly not in the same way as California. I think you’d actually have an easier time making the numbers work there because you can get a house in Kansas City for two, three, 400,000 bucks. In LA, you’re going to be looking at a minimum of 700k. I mean, I guess in LA there’s other cities and stuff like that. So I think…

David:

Why couldn’t you do both?

Wendy:

I could. There’s no reason not.

David:

If you get an awesome house in Kansas City for 400 grand, you put 5% down, $20,000 plus closing costs, get the seller to pay those, maybe give them 410 for the house and have them pay $10,000 towards your closing costs so you’re just coming out of pocket 40 grand. Figure out a rent by the room scenario, then do the same thing in Long Beach. The downside to you is just a little bit more work managing the rooms of two different properties.

Wendy:

Sure.

David:

The upside is…

Wendy:

That’s fine. I’m trying to get to the point where real estate becomes my job as opposed to the job I’m in.

David:

Yeah.

Wendy:

And I might have to do it slowly.

David:

I think you could do both. Especially if you’re using primary residence loans. People underestimate how slow it is to build a portfolio putting 25% down. You can literally buy five houses for every one house if you put 5% down on a primary. You could scale five times faster.

Wendy:

Wow. I mean that’s amazing. And that’s what I haven’t done till now. I’ve got these little, my little crockpots stewing all around the country of 20% down, 20% down, 20% downs of those turnkey houses that I bought. And those can stay and do those things. And maybe I also will, on another vein, turn some of those into some more midterm rentals or house hack some of those in the future. But right now they’re working, I’m just going to let them stew.

Rob:

I think it’s quite a gift that you’re willing to house hack and willing to move. You’ve got the most flexibility ever.

Wendy:

Right.

Rob:

So exploit that. Try it. Experiment. I think my advice to you is if you have a little bit of money to invest here, plan a six-week trip across the country, stay in Tampa for two weeks, stay in Kansas City for two weeks, stay in Long Beach for two weeks and understand the city before you’re there. LA is a very glamorous place on postcards, but the reality here, it’s tough. I lived here for five years. It’s not an easy city to live in. It can be a pretty lonely city.

David:

If you can make it here, you can make it anywhere.

Rob:

That’s true. But as long as I’m here, you’ll always be second best. You hear? But yeah, I think travel around and live in the city, stay at couple of Airbnbs, and then decide.

Wendy:

Yeah.

Rob:

Because ultimately, your happiness in the city matters too.

Wendy:

Right. Okay. That’s great. I love it.

David:

What can our listeners do to help you?

Wendy:

Well, gee, I guess if you have any great, I need a great realtor. This is something I learned at the meetup last night. Boy, I talked to this guy from Bakersfield and he has got 13 rentals and all this, and he just couldn’t say enough great things about his realtor who connected him to all these things. And here, I’ve got my contractor and I’ve got this, and I know all the realtors say they do that, but I just haven’t had that kind of a rockstar realtor. So I need a really good realtor.

David:

Where?

Wendy:

Oh, Kansas City, Tampa and either San Diego or Long Beach.

Rob:

Perfect.

David:

You’d have a much easier time finding a rockstar realtor if you had one city that you were committed to buying in.

Rob:

Because you’re about to get hounded by 50 realtors.

Wendy:

Uh oh, uh oh.

David:

Right? If I said, “I really want a knockout wife,” and I said, “but I’m dating these six other girls at the same time,” right, the knockout wife’s probably like, “Yeah, I’m not interested in that.” You’re going to get the same thing from the agent. So if you can narrow it down, you’ll have a much easier time getting the attention of the best talent out there.

Wendy:

Okay, great.

David:

All right, last question. We’re going to get through this pretty quickly, so thank you guys all for being here. But very quickly, Phillip, we’ll start with you. What’s the one thing that you learned that may help someone else listening?

Philip:

Focus, the nail down your deal criteria and due diligence. Money is made in due diligence.

David:

There we go. Beautiful. Danny?

Danny:

For me, delegate as early as possible. Treat your business as a business. Don’t become an employee. It’s really easy to get sucked into that.

David:

Bro, you really hate anyone bugging you with questions about toilets and light bulbs. I can see this has come up like five times.

Danny:

Yep.

David:

Has that deterred you from wanting to go deeper in on real estate investing, all the little paper cuts of annoying things that need to be done?

Danny:

Not at all. What it has forced me to do is use property management upfront. Actually haven’t honestly experienced much of that. Toilets, I have some stories from my condo, self-managing it for a little while, which is terrible.

David:

Yes.

Danny:

But really, when I started this education, where I overeducated myself, I said, “You know what? This really needs to be a business upfront.” So just kind of frontloading and having that mindset even before I got those cuts and just actively avoiding them because that’s what I’ve learned.

David:

Awesome. Wendy?

Wendy:

I think I’ve learned that I need to do some better networking. I don’t go out to meetups enough. I stay at home and I read my books and I surf online and I look at Zillow and I feel like I’m making progress, but sometimes it’s just talking to people that’s part of the value. And I heard you say some things, Rob, about when you go to the meetup, make sure that you have a goal in mind of what you want to get out of it and work the room with that prospect in mind. Because I’m just like a Labrador, I’ll go to a meetup and I want to talk to everybody, “Oh, it’s nice to meet you. Oh, you’re fun. Oh, I like your hair,” but I never really thought about having a purpose when I show up there.

David:

What’s one thing you learned from watching me at the meetup interacting with people?

Wendy:

Well, you were always very quick with your advice and your networking and you definitely, I mean, you didn’t have to work the room. The room came up to you. There was a line to come to talk to you all night. So what I learned is that you get in quickly, you have your conversation with them and then you find a way to delicately exit and move on. And I think I heard you say earlier that you try to give something back to them as an exit strategy.

David:

Did you see me connecting them with Lindsay or Christian or any of the other agents on my team?

Wendy:

Yes.

David:

Why do you think I was doing that?

Wendy:

Because then you gave them a next step.

David:

Yes, that’s exactly right. I was also being intentional. So like Rob said, you’re going there for a purpose, you’re going there to find people that are going to help you. I’m going there to find people that need a loan from the one brokerage, people that need an agent for Southern California. That’s why we put this whole event on, was we’re going to look for clients. We’re not just going to get my ego boosted because everybody wants to come talk to me.

So I showed up with a purpose and I had a plan. Find the person, make a connection, connect them with them. And then when someone does close a house with us, you might’ve heard me say, “You’re in the family now. Whatever you need, I’m here for you,” because I really value the people that are supporting me and the things that I have, now I want to support them. I think that same energy can be used at any meetup or in any situation. So thank you, guys. This has been fantastic. It’s nice to see you all again and I’m glad, I know that you mentioned that you tried to come talk to me at the meetup a few times and you’re like, “Every time I tried, somebody else was cutting me off,” and it [inaudible].

Rob:

Got to be assertive.

Wendy:

He’s super popular.

David:

Yeah. So thank you guys for being here. Rob, do you have any last words before we get out of here?

Rob:

No, I love it. I love to see the journey and it doesn’t always go the way you plan, but as long as you keep going, then you’re going to be happy that you stuck to it. So keep rocking and rolling and I can’t wait to check in again.

David:

Philip, for people that want to find out more about you or bring help for the wholesale deals that you’re looking for, how can they do so?

Philip:

Yeah, on Instagram, educatedinvest is my Instagram handle and my website is educatedinvest.com.

David:

Also, make sure I connect you with Charles because he’ll help you find some flip opportunities in East LA if that’s what you’re looking for. He’s kind of our specialist of finding those.

Philip:

Oh, cool. Let’s get it.

David:

Danny, where can people find out more about you?

Rob:

And help you?

Danny:

Yes, on BiggerPockets, Daniel Zapata. And Instagram, investoronfire.

David:

And did we ever ask you if you have any relation to Emiliano?

Rob:

Relation to, yeah.

Danny:

I think we’ve broached that subject and some shoes came up and some stuff I still get crap about.

Rob:

What’s one thing that you’d like for someone to reach out to help you with?

Danny:

For me, I think deals. This 10 to 20 unit market is actually not as big as I would’ve thought as I dig into it. So I’m thinking I’m going to have to start digging deeper into off-market deals.

Rob:

In Sacramento?

Danny:

In Sacramento.

Rob:

Okay.

Danny:

So if you have those, please bring them to me.

Rob:

Wonderful.

Wendy:

I’m Wendy St. Clair on BiggerPockets and I’m also on Instagram at wendysc_invests.

David:

And how can people help you?

Rob:

Yeah.

Wendy:

How can people help me? I am looking for a triplex or quad in Kansas City or Los Angeles.

Rob:

There you go.

David:

I love it.

Rob:

Long Beach.

David:

Rob’s selling the Kansas City market.

Rob:

I love it.

Wendy:

Or Tampa.

David:

That’s an emerging market.

Wendy:

Yeah.

David:

I think that that is a market that’s going to grow to be perfectly fair. Over the next five, 10 years, I think you’re going to see rents increase and values increase in Kansas City. People migrate to where housing is more affordable.

Rob:

It’s true.

David:

There’s no way around it.

Rob:

Where can people will find you?

David:

They can check out my newly revamped social media that is now shiny and awesome at davidgreene24. I’m putting out a lot more content there as well as all the other different socials. Davidgreene24.com is the website and YouTube is at DavidGreene24. Rob, how about you?

Rob:

You can find me over on Instagram at robuilt or on YouTube at Robuilt. I put out a lot of free content. Most of my content is free where I teach you all how to do the whole short-term rental real estate thing.

David:

Awesome. This is David Greene for Rob. If you can make it here, you can make it anywhere, kid. Abasolo, signing off.

Help us reach new listeners on iTunes by leaving us a rating and review! It takes just 30 seconds and instructions can be found here. Thanks! We really appreciate it!

Recorded at Spotify Studios LA.

:215-447-7209

:215-447-7209 : deals(at)frankbuysphilly.com

: deals(at)frankbuysphilly.com

Rate lock activity declined sharply in July as rates exceeded 7%

Rate lock activity fell for the second month in July as mortgage rates topped 7% for the first time since November 2022.

Overall rate lock volume was down 7% month over month, with purchase lending accounting for 88% of total lock activity, according to Black Knight‘s originations market monitor report.

Even so, purchase lock counts were down 27% year over year and 35% compared to 2019 pre-pandemic levels, as high-interest rates and persisting low inventories dampened demand.

The 30-year conforming rates crossed 7% for the first time in eight months, before falling sharply and then rebounding to 6.88%, according to Black Knight’s Optimal Blue mortgage market indices.

“Purchase loans continue to dominate the origination pipeline, but current housing market dynamics are just not conducive to boosting homebuyer origination volumes,” Andy Walden, vice president of enterprise research and strategy at Black Knight, said.

Credit scores for conforming (754) and FHA (669) borrowers remained flat in July while VA dropped one point to 712 from June.

Black Knight’s recent mortgage monitor report pointed to signs of credit tightening — attributed falling loan-to-value ratios and rising down payments.

Adjustable-rate mortgages (ARMs) fell to 6.79% of July’s rate lock activity, as rates for such products became less competitive against fixed products.

Cash-out refinances also declined 5.4% and are hovering close to 60% below where they were in July 2022 when interest rates averaged in the mid- to high 5% range.

Rate/term refis increased by a modest 1.9% in July, but remained down more than 31% year over year from an extremely low ceiling.

Locks on such products – including cash-out refis and rate/term refis will likely remain constrained for some time to come, Black Knight noted. Just 3% of existing mortgage holders have first-lien rates at or above today’s levels.

The average loan amount fell about $2,000 in July while the average purchase price on locked loans fell to $456,000, according to Black Knight’s report.

Normally, June typically marks the calendar peak of home prices on a non-adjusted basis.

Home prices would decrease through the end of the year and into February in normal times, but this trend does not apply in this market and this year, Walden noted.

“Rising rates may be tamping demand for homes at such record high prices, as evidenced by rate lock activity, but they’ve still yet to overcome an even greater deficit of supply. As a result, the purchase market is in a stalemate,” Walden said.

Source link

Fannie Mae scraps title waiver pilot program

The American Land Title Association (ALTA) is celebrating a huge win in its ongoing war against title insurance alternatives. Fannie Mae is no longer considering a pilot program that would bypass traditional title insurance by granting certain mortgage lenders a waiver on title insurance requirements for loans sold to Fannie, according to an announcement earlier this month.

This is a major victory for the trade group, which felt that Fannie Mae was “moving beyond its charter” with this pilot program.

News of the rumored pilot program came in March, roughly a year after Fannie Mae first announced that it would be accepting attorney opinion letters (AOLs) in lieu of title insurance in limited circumstances.

The pilot program was said to have been a component of the government sponsored entities’ (GSEs) Equitable Housing Finance Plans, which are required by their regulator Federal Housing Finance Agency (FHFA).

The initial version of the GSE’s Equitable Housing Finance Plans were approved in the summer of 2022 by the FHFA.

“The intent was to promote affordable and sustainable housing opportunities for more households nationwide,” Diane Tomb, the CEO of ALTA, told HousingWire late last year. “One of the goals they outlined in those plans is a push to reduce closing costs, especially for low-income borrowers. Based on those plans, both GSEs are pushing pilot programs promoting the use of attorney opinion letters, reportedly as an alternative to reduce closing costs.”

According to an email Tomb sent to ALTA members earlier this month, obtained by HousingWire, more than 200 trade organization members shared their concerns about the title waiver pilot program with members of Congress.

“This is a significant achievement to protect consumers, lenders and the housing finance system, and showcases the benefits of our products, industry and your business. The success of challenging this pilot underscores the value of advocacy and making your voice heard,” Tomb wrote in the email. “Importantly, we will continue to work with the FHFA and policymakers to thoughtfully address housing affordability and opportunity. We will also continue to collaborate with Fannie Mae and Freddie Mac to deliver innovative and cost-effective title insurance products and solutions that best protect lenders and consumers.”

Despite scrapping this pilot program, Fannie Mae said it will continue to look for ways to improve housing affordability.

“Housing affordability is key to Fannie Mae’s mission, and we remain committed to our ongoing engagement with industry partners and providers to explore ways to make the homebuying process more affordable and accessible in a manner that does not increase risk for borrowers, lenders, and the marketplace,” a Fannie Mae spokesperson wrote in an email.

For its part, ALTA said it is working on lowering closing costs where it can, and it believes the increase in automation and improved technological capabilities within the title industry will lower costs over the next few years.

“Over the last 10 years, rates have gone down 6% across the industry and that is important for homeowners and it’s because of the investment the industry has put into things around automation and using machine learning and AI to search title and come to a faster decision about the title,” Steve Gottheim, ALTA’s general counsel, told HousingWire last November. “These technologies come with a cost at the front end, but over time, they bring that efficiency and bring the price down.”

During the first quarter of 2023, title insurers brought in $3.37 billion in title insurance premiums, while paying out just $162.7 million in claims during that same time period, according to data from ALTA.

Source link

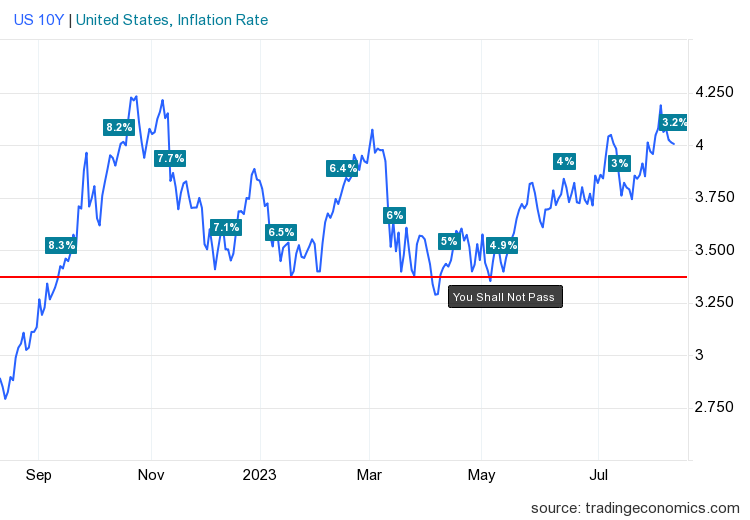

Where are mortgage rates headed?

Last week ended with a wild ride for mortgage rates. We anticipated the two inflation reports could help mortgage rates, however, we had a bad bond auction last Thursday, and the 10-year yield rose sharply. Weekly active inventory grew slowly again and purchase apps were down week to week again.

Mortgage rates and bond yields

Last week we started with lower bond yields as we anticipated inflation reports to continue the trend of slower year-over-year inflation data. This happened as expected, except we had a lousy bond auction, which meant too much debt supply came online with insufficient buyers. This pushed yields higher Thursday and Friday to move mortgage rates to 7.19%.

A valid case for higher mortgage rates in the short term is that we are simply going to be in an environment where we don’t have a lot of bond buyers versus the supply coming in, thus making it harder for mortgage rates to go lower. We saw an example of that last week.

For my 2023 forecast, my range on the 10-year yield has been between 3.21%-4.25%, emphasizing that the bond yields can go lower than 3.21% only if the labor market breaks. The labor market breaking to me is if jobless claims on a four-week moving average go over 323,000; currently, that data is 231,000. As the economy has stayed firm, bond yields are at a higher level of my range for 2023.

Weekly housing inventory

The painful housing inventory story of 2023 continues as we had yet another week of slow inventory growth. Last year when mortgage rates spiked higher, inventory growth was much faster, but we were also working from the lowest levels recorded in history in March of 2022. This year, it’s been a much different story.

As we can see in the chart below, inventory growth has been so slow that active listings have been negative year over year for some time now. For those calling for a massive inventory spike since 2008, the last few years have not gone as planned.

New listings data has been trending at the lowest levels recorded in history for more than 12 months. However, even with higher mortgage rates in the last few months, we haven’t seen a new leg lower in this data line, which means we might be forming a workable bottom in 2023. As you can see in the chart below, 2023 has had a clear divergence versus 2021 and 2022 data, which were already at all-time lows before last year.

Here’s how new listings this week compare to the same week in past years:

Purchase application data

Purchase application data was down again by 3% last week, making the count year-to-date at 14 positive and 16 negative prints. If we start from Nov. 9, 2022, it’s been 21 positive prints versus 16 negative prints. Mortgage rates near or above 7% are simply too high to promote real growth in this data line, which is working from a historical bottom.

So, when rates fall, moving the needle higher for purchase apps won’t take much. However, for now, rates this high have facilitated more negative week-to-week data than positive, leading to lower sales as this data line looks out 30-90 days. While we aren’t seeing sales collapse like last year, we aren’t growing sales meaningfully from the recent lows.

The week ahead: Tons of economic data

This week, we have various economic data reports that can move mortgage rates and give us a sense of where the housing market is going. Retail sales and the Leading Economic Index are out this week. Also, we get two key data lines for housing this week: the homebuilders survey by NAHB/Wells Fargo and housing starts!

What I am looking for in housing data is what the builder survey indicates for the next six months. In last month’s report, we saw a slight decline in this data line. For this week, I want to see how mortgage rates react to the batch of new economic data.

Source link

What to Do TODAY to Instantly Find More Real Estate Deals

Real estate investing isn’t what it used to be. Back in 2010, in a post-crash housing market, almost any property in any area could cash flow easily. Back then, the question wasn’t “Where are the deals?” It was “Which deal should I buy?” But things have changed, and now in 2023, homes are hard to purchase, let alone cash flow, and more and more real estate investors are giving up simply because they don’t know the new rules of the game. So, here’s what you NEED to know.

Before we unlock every wealth-building secret in the book, let’s welcome back Danny Zapata, Philip Hernandez, and Wendy St. Clair, our recent mentees of the ninety-day mentorship! We brought them back on the show to talk about deals they’ve done, the progress they’ve made, and where they’ve fallen off track. One mentee left their job, another is handling headache evictions, and one had to put a pause on real estate. But now, they’re ALL ready to expand their empires, but they’ll need some advice first.

In this episode, David and Rob show you how to get more real estate deals TODAY, why you’re doing meetups all wrong, the reality of cash flow and why “mailbox money” isn’t what it used to be, and what to do when you CAN’T find the momentum to keep growing your wealth.

Support the relief efforts for the Maui wildfires by donating to the organizations below or clicking here. Together, we can make a difference for those affected by this tragic event:

David:

This is the BiggerPockets podcast show 804.

Rob:

A lot of people get stuck mingling with the same person and it’s a little awkward to leave, and you’re just chatting with someone for like 15 minutes, but you know you have nothing else to talk about, in and out. “Do you have a deal? No. Great. Hey, nice to meet you, man. Have fun at this meetup.” Next.

David:

Yeah.

Rob:

Boom. “What do you do? Wholesaler? Great. That’s exactly what I’m looking for. You on Instagram? Let me get your Instagram.” Boom. Move on to the next one. If there are 200 people like there were last night, if you only met 20 of them, you didn’t do your job right. You need to meet all 200 as fast as possible and see who can serve you because you’re there for a purpose.

David:

What’s up, everyone? This is David Greene, your host of the BiggerPockets Real Estate podcast coming to you live. Well, not really live for you, but live for us.

Rob:

Yeah, live for us. Well, every podcast is live for us if you think about it.

David:

Yeah. Why do we always say coming to you live? What could you say instead? Coming to you previously recorded.

Rob:

We’re coming to you pre-recorded from live in Los Angeles.

David:

Downtown LA at Spotify Studios where we are recording, and we got an update today with three of our former guests. They were the mentees from previous episodes and we’re getting a little update. Rob, what should our listeners look for to help them with their investing journey in today’s show?

Rob:

Yeah, so it’s really fun to examine the journeys of our, I call them our little fish. They’re out there, they’re doing their thing and it’s really great to check in with them. But one of the things that I saw was that they had these big goals, but not necessarily steps or an action plan to achieve those goals. And so I think that is going to be huge because I basically gave them the advice to just make sure that you’re intentional with every single goal that you set. And so I think hopefully that opens up the eyes of some of the people at home that have realized that they’ve set these lofty goals, but they’re not actually giving themselves deliverables that will keep them accountable towards hitting those goals. You know?

David:

That’s a great point. Their motors were revving, but they didn’t know how to put it in gear.

Rob:

Yeah. [inaudible].

David: