Ashley:

This is Real Estate Rookie, episode 301 niner.

Terry:

So for me as a developer, one of my deals actually, we bought the land for 25,000. We spent another 25 to pre-develop it and all in, that’s $50,000. We just got the plans approved. That is all that I needed for my construction loan.

Now my construction loan comes in and we’re able to build the whole house. And now the choice is mine of what I want to do after if I want to refinance it and keep it or if I want to sell it.

Ashley:

My name is Ashley Kehr and I am here with my co-host Tony J. Robinson.

Tony:

And welcome to the Real Estate Rookie podcast where every week, twice a week, we bring you the inspiration, motivation, and stories you need to hear to kickstart your investing journey. And I got to say, Ashley, I appreciate you throwing the J in between the Tony and the Robinson.

So for our rookie audience, there’s a reason why I like the J. First, there’s Tony Robbins who I get confused for all the time, and I’ve disappointed quite a few people because they’re like, “Oh my God, it gets me Tony Robbins.” When really it’s just me. And there’s also other guys in the real estate space named Tony Robinson. So I got to find a way to separate myself. That’s where the J comes from.

Terry shares a lot about his journey of going from a real estate wholesaler to a developer, and he shares some really interesting nuggets on what it costs to develop. I’m telling you guys, you’re not anticipating, you’re not going to believe what he says when he shares the price.

Ashley:

One of my favorite things about this episode is how we go so in depth about what you need before starting new development and who you need. Terry’s going to do a great job of outlining those first steps that you need to take.

He started out wholesaling, and he’s going to explain that pivot, that transition into new development, in case that’s something you are thinking about doing.

Tony:

So for all of our rookies that are listening, we promise you’re going to get a ton of value from hearing Terry’s story for a second time, and we can’t wait to share it with you.

But before we do, I want to share a review by someone of the username, ginalou. And Gina love to say, 5-star review on Apple podcast that says, “Wealth of real estate information. What a great podcast, full of excellent real estate investing nuggets. Thank you for sharing your journeys, finding inspiring guests, and providing a wealth of information for new real estate investors. When I was looking to get started in real estate investing, I came across BiggerPockets in the Real Estate Rookie podcast and it totally changed everything.”

So Gina, we appreciate you. Thank you so much for leaving that honest rating and review. And for all of our rookies that are listening, if you haven’t yet, it only takes a minute or two, please do leave us an honest rating and review on whatever podcast platform it’s you’re listening to. The more views we get, the more folks we’re able to reach and the more folks we can reach, the more folks we can help.

Ashley:

Terry, welcome back to the show. Thank you for joining us again on BiggerPockets Real Estate Rookie. Start off with telling us a little bit about yourself and maybe a little bit about your first episode with us.

Terry:

Yeah. So appreciate you guys always. It’s always great speaking to you guys. My name is Terry Harris. I started off playing professional basketball in the NBA G-League. From the NBA G-League, I got into real estate, just kind of found a passion with real estate and just started reading as much as I could about it, talking to as many people as I could and just got into it.

Was able to buy my first home on a FHA 3% down in Delaware where I was playing. And I believe our first interview was kind of me going over of how I got into real estate and the kind of niche that I was in currently, during that first episode, which was wholesaling real estate. And through wholesaling real estate, I was wholesaling land to land developers.

And the beauty about that was I was learning from developers as well, how they were buying land, what they were doing with the land and how they were developing it. And at the same time, I was also making a little assignment fee from the wholesale deal, so it was like a paid internship for me. So now I kind of switched the gears a little bit and got into developing real estate.

Tony:

Terry, how many wholesale deals would you say you completed and are you still actively wholesaling?

Terry:

I think I completed around about, I would say about 30 wholesale deals. 30 wholesale deals. It was a point where I was doing around three to four deals a month at my prime, you can say. But now, it’s to a point where I’m looking to wholesale deals for myself, my partners, to do land deals. So the wholesaling techniques and the marketing that I’ve used, I still implemented in my real estate strategies today.

Ashley:

Terry, how long did it take you to get that first deal and what did you have to do to get it?

Terry:

That first deal? I would say it took about four and a half months for that first deal. And that was kind of with learning and trial and error and everything. It took me a lot of calls and I didn’t really know how to do it. I didn’t know how to wholesale in efficient way.

I remember I just got PropStream, I bought a list of about 1500 names and numbers, and I would sit with three highlighters, red if they said no, yellow if they didn’t answer and green if it was a lead. And I would every day call 60 to a hundred. That was my goal. And I do that and get some appointments going, visit some property, see if I can get deals on the contract. And it took about four months to close something.

Ashley:

Can you just walk us through the process of pulling a list and what a list is and what PropStream is for maybe somebody who has no idea what that process looks like? Can you kind of break it down for us into steps real quick?

Terry:

For sure. So PropStream is just a software technique, where anybody can go on PropStream, you can see who the property owners are, of properties when they purchased it, if they have a mortgage or a loan on it, what it’s sold for. It gives you a lot of data on properties.

And I use PropStream, so I picked the area that I was actually, at the time I was playing basketball and I was training in, so I picked the area that was that specific area in California, and I bought a list of about a 1500 high equity vacant homeowners. And the reason I sought high equity vacant homeowners is because another wholesaler said this was a good list to target because one, they would probably be willing to sell at possibly a discount, and if it’s vacant, they’re probably not making money off of it.

So getting a deal like that under contract could be really enticing for an investor. So that was my initial target of what I was going to look for and I wasn’t going to stop until that list was complete or I got somebody who wanted, was willing to sell their property to me.

Tony:

Terry, you said you weren’t going to stop until that list was complete, just like ballpark, how many people or calls do you think you had to make before you got that first deal?

Terry:

That first deal was probably about 600 to 700 calls. 600, 700 calls, and I was doing that. I was doing a little bit of driving for dollars, so I would put your guys’ podcast on and I would just drive around the local neighborhoods and if I see a vacant house, I just put it on the list, probably about 600, 700 calls.

Tony:

Terry, I mean, kudos to you brother, because I think so many people listen to this podcast and naturally, hear the success stories of investors and sometimes they can gloss over the hard work that goes into being on this podcast. And a lot of people would’ve given up after 100 calls or 200 calls or 300 calls or 400 calls or 599 calls, but you push through, man. So I think there’s an important lesson to take away from that for our rookie audience.

One thing I want to ask, because you mentioned this a little bit earlier, but you said that you basically had an internship in land development by wholesaling first. So I’m curious, why exactly would these developers be willing to take one of their wing and give you free education, and what were some of those things that you learned by being kind of close in person with them as they were doing that?

Terry:

So it’s quite simple. I was providing them value. I was able to give them deals, off market deals that were below market value. So at the time I knew something, I was like, “I really want to develop, I really want to build something and create a cool looking home and I want to develop.” So my thing was like, “Let me wholesale land, let me wholesale something that I want to get into.” And that’s what I recommend, honestly to anyone to go and wholesale something that they’re looking to get into.

So land deals were my way of getting into real estate, and as I started wholesaling land to developers, they were like, “Keep them coming, keep them coming.” And it was just like a relationship and they were like, “Hey, we need something in this area.” And then at the same time, I was like, “So how’s that property that I just developed, that I just wholesale to you five months ago?” And they would say, “Oh, it’s good. We just took a loan for 400,000. We’re going to build this property for 400,000 and we’re going to look to sell it for 800K plus.”

And I’m over here thinking, “Wow, I made $8,000 off an assignment fee, but you’re going to develop this and make over a 300K profit.” I was like, “Hmm, this might be a better game that I can get into.” And that enticed me. Obviously the money, that was something enticing, but then again, it was just so cool to see something, see a developer’s plans, hit the paper, come to life, and then for them to do whatever they want to, keep it, sell it or make an Airbnb. So I was just like, “Man, that’s what I want to do.”

Ashley:

Terry, a hard part of being a wholesaler is first finding deals, but the second part is finding buyers. So how did you create that buyer’s list of developers? I mean, it’s such a specific niche that you’re looking for. It’s not like you’re selling a single family home. That could be a rental or it could be a house that you’re flipping. So how did you find these developers to actually sell these lots to?

Terry:

I speak to a lot of people and they’re like, “Oh, but finding the buyers is hard, isn’t it?” I said, “It’s the easiest part. It’s the easiest part.” And it’s just the same way where I go and find the sellers or the property owners is the same way I found the buyer. So I would go on PropStream and pull a list of everyone who’s bought vacant land in the same area of where I was looking to wholesale, and probably in the last two, three years, because if you bought vacant land in the last two, three years, you’re probably buying it to develop or maybe to hold onto it to see if it appreciates over time.

So I pulled the list of all the people who’ve bought land in the last two, three years, and I would blast out a text to them of all my deals, and of course, some people wouldn’t answer. And the people who did answer, I would make sure I get on the call with them, see how they’re interested and see, “What are you looking for if you’re not interested in this land?” And that just starts to build up, slowly over time.

You start building your own buyer’s list and you start to know now specifically what they’re looking for. And now, you’re not just building a buyer’s list now, but you’re also building a developer’s eye for deals. Because now, like, “Oh, these three of the best developers in this area want properties that are this size this big and this much utilities, and they want this because of this.” So I started to get that developer’s eye as well. So it also, you build a buyer’s list and then you’re also learning how to be a developer. So it’s two full things that you can get.

Tony:

So Terry, I want to comment on that before I lose this thought. You talked earlier about why the developers were willing to give you all of this free information and it was because you provided value to them. And Ash and I have talked about this a lot on the podcast, where we oftentimes get messages from people in the rookie audience who want to pick our brain or offer to take us out to lunch or dinner, and unfortunately we are busy running businesses right now, so we don’t have a ton of free time.

But if someone came to us and said, “Hey, Tony, I know you invest in these three markets and I’ve got a deal that’s 50% discount on retail value and I want to give it to you.” That was a great way to build a relationship with someone. And I think you found that as a good path forward.

And just as a quick side story, someone actually reached out to me recently asking to partner with me on a deal. And they’re like, “Hey, Tony, I’ll do whatever you need me to, this, that and the other.” And I said, “Look, I’ve got my team in place, but if you find me a deal, I’d be happy to work with you on it.” And his response was something to the effect of, “Well, no, thanks. If I find a good deal, I’m going to keep it for myself.”

And I thought it was such a weird response because they had reached out to me asking to work with me, and I gave them a very clear like, “Hey, if you can do this thing, I’d be happy to work with you.” But their thought process was almost shortsighted in the sense they were focused on like, “Hey, if I get a good deal, I’m going to keep it for myself. Not work on this relationship lead me long-term.” Whereas for you, Terry, you now have been able to elevate your own real estate business because you were so focused on giving value to the people that were a few steps ahead of you.

Terry:

And what’s crazy is in the beginning, I was kind of the same way a little bit. Even when you say that, when you’re starting to get going, you want to establish yourself, and I was like, “I want to get my own properties. I want to be a hundred percent owner, a hundred percent owner.” And when I sat back and really thought about it, “Okay, if me doing my own properties.” I have the capacity at the time to do two at max on my own. That’s it.

But I had the same kind of thing as I find deals and I found an investor who was like, “Hey, if you can find us deals, we can make you a partner and you can oversee these builds.” And now it’s come to a point where we together have bought eight properties together. So now I get two on my own and eight with them. I’m able to do 10 projects now.

So, I’m now, it’s like, “The power of partnerships can help you grow astronomically.” And that’s something that I have to mature and grow from, but it’s just in order to grow, I believe working with other people, working with partners is just the right way to do it and it’s the more efficient way to do it. But it’s so funny that you say that, because I can definitely relate.

Tony:

And Ashley and I are both smiling right now, because you said partnerships twice in that last sentence. And Ash and I just recently released a book with BiggerPockets called Real Estate Partnerships. So if you guys head over to biggerpockets.com/partnerships, you can pick up that book and learn how Ashley and I have leveraged partnerships to scale our own real estate portfolio.

So thank you for that little tea up there, Terry. I appreciate that, man. But one thing I want to go back to, you talked about building your buyer’s list and you said you would pull a list of all the folks that had purchased land in the area that you were focusing on.

My question is, Terry, were you waiting until you had a deal to present to them before you reached out? Or were you just reaching out preemptively to say, “Hey, my name’s Terry, I saw you bought land here. If I have something in the future, can I share it with you?” Which approach were you taking?

Terry:

I got the deals under contract, and I would have about two to three of my own buyers in the beginning. And then every time of course, I’d blast out to the people who I knew, but I would do the blast of just, I mean, I would not have any type of communication with them. I would just give a little bit of details on myself and give mainly details about the land. I’d give the Google coordinates and then just talk about the deal just very, very briefly.

And the thing is that I would message thousands of buyers, and I always knew two to three would be interested and about probably 40 people would answer, “Ah, not what I’m looking for maybe.” And then I would go and get that conversation going.

So I would always get the deal under contract first. But now I, in today’s market where buyers are about a little more slim, I would try to find, I would today in today’s market, try to find the buyers to find the active investors in the areas and kind of know what they’re looking for and then go after that area.

Tony:

Terry, I want to ask, so at what point did you kind of feel the confidence to make the switch from wholesaling the land to actually developing it? What was that moment or that milestone where you said, “Okay, today’s the day that I’m ready to take that next step”?

Terry:

I would say when I submitted my plans for my third project, I believe I had one that broke ground, another one that was about to be broken ground on, and then it was the amount of time that I really wanted to pay really close attention to detail. And I knew I wanted to be a developer, I wanted to be a full-time developer, and I started building partnerships and I knew a lot of people wanted to build.

So I was like, “You know what? Let me lock in on this. I want to spend time, instead of spending a lot of time on wholesaling, I want to spend more time learning how to read plans efficiently, learning how to maneuver through planning departments the correct way, read more about developing, connect with more developers.” So I really just was like, “I want this to be my full-time thing. I don’t want to be known as a wholesaler, I want to be a developer.”

Tony:

But Terry, even that first one, because you said it was like that third one where you kind of mentally made the transition to do it full-time, but I mean, even going back to that first development deal, how did you know that you were ready for that one?

Because development is such a, it’s a big step beyond wholesaling. I’m sure a lot of the skills translate in terms of finding the deal, but like you said, there’s so much more nuance that goes into the development. So when you did that very first one, how did you know you were already in that moment?

Terry:

I didn’t. No, no, it was, it’s just you’re going to learn. And the way I look at real estate is you are always going to learn. If you hold an asset long enough, it’s going to make you money and you’re constantly just going to get better and better and better. I’m not going to be, you go into anything, I’m not going to be the best right away, but you’re going to learn, you’re going to get better. You’re going to grow.

So I knew the first one was just like, “Look, it’s going to be a crazy learning curve and I’m going to just learn new things. I’m going to become, get more efficient, learn how to develop quicker, faster, and more affordable prices.” But I knew I was like, “All right, this is something that I’m going to, this is new, but I’m ready for the challenge.” And I was just super excited to get into it, really.

Ashley:

Terry, who were the first people that you brought onto your team? So as a real estate investor that’s buying rental properties, you may seek out a property manager. So were you going after architects, engineers, what did that kind of look like? What’s different from already buying a building than doing new development?

Terry:

I think the first thing was finding a good architect. That’s probably the first person that you want to get on your team, that is after you purchased the land.

And what’s good about finding a good architect and some that didn’t know before in my first development deal is I hired anybody on the first one. And it was, the challenging part was that, I had to go and find the civil engineer, I had to go find the surveyor, I had to go find, do all the other resources.

But now once I found, now on my third one, I’m using a local architect now, somebody who’s been developing the area for 20 plus years, has good image and knows how to develop in the desert. But he knows great local civil engineers. He knows a good local surveyor or a good local, somebody who could do a perc test.

So it was just doing things like that, it makes it way more efficient, it makes it easier for you. He lives right near the planning department, so he drops the plans off instead of me dropping the plans off. So that first step was getting an architect, and I think that can also find the right architect can make or break your project too. So that is very huge.

Tony:

I just want to add something Terry, because you’re kind of alluding to this, but there there’s an incredible amount of value in hiring professionals that are local to the market that you’re investing in.

We’ve had issues in Joshua Tree where we both invest Terry, with appraisals where sometimes these out of town appraisers would come in and they wouldn’t really understand the nuances of that sitting in that market. And we get these super low appraisals and we’d have to challenge them, get them reappraised and someone who’s local who better understood the market could come in and knock it out quickly.

Same with general contracting crews. They don’t understand the nuances of building in Joshua Tree, so they run into delays, that GCs that are born and bred in the desert, they already know how to navigate those things. So I think for most people when they’re trying to build out that team, if you can go local to someone that understands those nuances, there’s a tremendous amount of value there.

Ashley:

Terry, you had mentioned that you found the architect after you purchased the land. So let’s go back a little bit. If you’re doing the land purchase first, tell us about what made the land a good value. What were you looking at as to like, “These are the things I need in this parcel to be able to develop on”? And even the location of it.

Terry:

Every market is a little bit different. So I’m developing two markets right now in Joshua Tree in Los Angeles. So one of the things that’s common in every market that you have to look for though is your zoning code.

So if you’re buying in Joshua Tree most of the time or developing in Joshua Tree, you’re probably trying to develop a luxury single family home to make it an Airbnb. So what we want to make sure is, “Okay, are Airbnbs allowed in this area? Are single family homes allowed to be developed in this area?” In Los Angeles we’re developed, we’re multifamily, so we want to make sure, “Can we develop these X amount of units? Can we develop to this height? Can we develop to this square footage?” Just simple zoning codes.

So you want to make sure, I know some people, they buy some stuff on some lot, they think they can build three different homes and make them Airbnbs, but the zoning code will tell you differently. The zoning code will say, “No, only one house can actually be on this lot.” That’s it. So I think knowing your zoning code is the number one thing you want to do while you’re in escrow or even before really, before you even make an offer for the land.

The next thing you want to do is also know utilities know, “Okay, I’m buying this land here, does this land have water? Does this land have power? Does this land have sewer? Or do I need to put a septic or do I need to do a perc test and get a septic tank here?” Knowing this prior, so you don’t have any of these big hiccups coming into the process.

And then Joshua Tree specifically also is you have to be 40 feet away from a Joshua tree. So you also want to look, we can look at the satellite image and kind of tell how many trees are on a lot. So that affects us if we want to build or how big we want to build. So there’s a lot of little things that you have to look at, but you can do a lot of your due diligence while you’re in escrow before you purchase the land.

Ashley:

Terry, where are you finding this information? Where can you suggest somebody’s just starting out, they want to look at the code and find out this information? What are some resources they can go to?

Terry:

Oh, for sure. Well, first I think whoever’s looking to develop, know what you want to develop first. So if it’s that single family home and you know that’s what you want to develop, and let’s just say it’s somewhere in Florida, Boca Raton, Florida, you can look up easily Boca Raton city zoning and the city, it’s all public information. The city zoning code should be right there.

And if it’s confusing, I mean it takes a little time to read it through, but if it’s confusing, another thing that somebody can do is easily, you can call up the local city building department, say, “Hey, I’m looking to develop or build a single family house in this location.” You can give them the address, they won’t shame you or anything. “I’m a new person I don’t really know developing. Can I develop a single family house here?” And they’ll tell you straight up, “Yeah, you can build something here.” Or “No, you can’t.” And even I do this till this day.

I just bought actually something in Los Angeles, I made an appointment with the Los Angeles building department. I came in with the paperwork, “Hey, this is the land I’m looking to buy. This is, I haven’t bought it yet, but I want to make sure, can I build what myself, what I think I can build?” And when my architect says, “We can build.” And that’s just extra due diligence just to make sure that we’re not going to buy something and come to find out we can’t build anything whatsoever.

Ashley:

Terry, I think one of the points you made too, will play value into this as far as figuring out the code is if you are hiring a local architect who knows the area, they’ll also know the codes, but they may also know the code enforcement officer.

What can actually be a huge advantage if they’ve already worked directly with this person, have a personal relationship with them too. I think has been, in my experience, a huge advantage of seeing those relationships play together as far as getting your project continued on.

Terry:

For sure. And to piggyback on what you just said, when I first went to a local architect, one of the things, what I had issues with with my first architect was all the time you get corrections from the city and when you get corrections from the city, the architect has to fix those corrections, then you have to resubmit them. And that can make the process a bit longer.

So when I went to the local architect, I said, “Well, how long are you going to take to actually do the corrections when the city gives you corrections?” And the first thing he said to me, “I’ve been doing this for over 20 years with the city, I don’t get corrections.” So I mean to hear that.

Ashley:

Love the confidence.

Terry:

Yeah, I loved it too. And he still got corrections to this day on my project, but needless to say though, it was like he knows the city, the city knows him. It’s always a little more comfortable when you’re in that process and when you have respect for somebody.

Tony:

Terry, I just want to comment on the whole corrections piece because I’m good friends with the builder out in Joshua area as well, and he’s third generation and he’s been building out there for decades now. So he knows the ins and outs of everyone at the county’s office and he’ll bill the same exact blueprint, the same exact property on multiple parcels at the same time.

So he’ll have three lots that he’s building on in different parts of the city. He’ll submit three sets of the same exact plans to the city for the same exact property, that’s getting built in just three different locations. Each set of plans will go to a different plan checker and he’ll get back three different types of revisions on the same set of plans. Makes no sense, right? So there’s a lot of, I think nuance and depends on who you get that determines on what kind of corrections you get back.

But Terry, I want to go back because, you talked about how to find the zoning code, but what about the utilities? If I’m looking at a parcel of land, how do I know if I have water, power, sewer or what it’ll cost to get that installed if it’s not there?

Terry:

Two ways. In my local market in Joshua Tree, you can actually go online to the water district and there’s a map that shows you the waterline on every single street. And for a newbie though, to kind of define that website and kind of get into that, that can be a little tricky.

But another thing they can do is you can call the local water district. You can call them up, say, “I have this parcel of land under contract and I want to make sure we’re connected to water.” And they’ll tell you straight up like, “No, you’re not connected to water. It’s going to cost you 50,000, it’ll cost you 5,000 or it might cost you…” I’ve heard water parcels coming up to 150 grand. So you can find that with a two-minute call easily in your water market.

Electricity, electricity is pretty easy. You can kind of see the electric pole on the parcel maps and if you’re unsure either like for SoCal, SoCal, Edison out here, you can call them up and just say, “Hey, just wanted to make sure this parcel has electricity or is it going to be a process to connect to the electricity here?” Simple as that. And those are the two main utilities that you have to look for and it’s really quite simple for the single family houses.

Tony:

Yeah, interesting. We’re working on some development right now as well, and we have to call the local electric utility to try and get some cost estimates for that as well. So glad to know I’m doing it the right way.

Ashley:

Tony, I have a follow-up to that too real quick, is sometimes on the tax record it will actually say if there is a well or public or if it’s public water or the well, or a septic or a public sewer system too. I haven’t seen that it says that there’s electric access to it or not. But another thing near us is gas.

So if there’s natural gas that may heat the house or if there’s propane. Where propane, you actually have to come and get propane delivered to your house too, which can actually be, first of all a huge inconvenience but also can play a part into the cost of having the propane versus having the natural gas supplied to your property too.

Tony:

Terry, I want to ask about the architect piece because you said that once you found this local architect, that person knew the civil engineer, they knew the surveyor, and that just kind of became your linchpin for the rest of your team and that market.

So the million-dollar question is how did you find that architect? Was this person on Yelp? Is there a resource or database of architects that build in markets? How did you find this person?

Terry:

Referral for this one. Now, when I find architects though, what I do now is if I see a home or I see a building that I like, I really like, I’ll do research, I’ll go put the address in, I’ll go and find that architect. I’ll figure it out some way somehow. But the reason I do that is because if that’s the style of build that I like, and that’s kind of the vision, more than likely me talking to that architect will help to encapsulate that vision or what they’re trying to create.

And most of the time for somebody, if they’re trying to develop in Joshua Tree, go drive around, find the houses that you really like. Just a quick little pie, 30 minutes of some investigating. I’m sure people do more investigating with their partners or whatever, but if they just do a little bit of investigation, they’ll be able to find out, they’ll be able to find out who that architect is. But for mine, definitely it was a referral for one, but now I like to find an architect whose vision is very similar to my vision.

Tony:

So I just want to pull that thread on the investigation piece. So say, I find 123 main street in the city that I’m looking at, am I then going to the county and saying, “Hey, who is the architect that submitted these drawings?” Or what is that? Is that the right next step?

Terry:

You could that. I think you could do that. So Los Angeles, the data’s public, so if there’s an address or a building that I like, usually if you look it up on, there’s this website website called Urbanize. Urbanize writes to article about every building that’s being proposed, who the architect is, who the developer is, and I’ll go and gather.

I’ll say, “Okay, that’s the architect. All right, let me call him. Let figure out. Let me try to work with this guy, see what he is saying.” And most of the time they’re willing to work with you.

Tony:

One other follow-up question on the architect piece, are you finding the architect developing the plans and then looking for the land? Or do you find the land and say, “Okay, what can I build that matches this land?”

Terry:

I would say depends on the market, but I’ll find the land first. I’ll find the land first. And then for instance, if somebody put me in Tony’s lap, a beautiful land in South Joshua Tree right near the park, let’s say two acres, Tony. We’re going to need a very, very sophisticated architect that can do a magnificent build, because we want to maximize the opportunity of that lot.

Now, if it’s another lot that’s let’s say way up north in Joshua Tree and a bit of an okay area, not that many views, we’ll use a good architect, probably a smaller build, but it’d be a different architect than the one over there by a greater area. So I feel like there’s an architect for every project or there could be an architect for every project. So I like to find the land first.

Ashley:

Yeah. So let’s talk about pivoting into development. For somebody who’s listening to this and now has shiny object syndrome and how they want to go into development, what are some things that somebody can actually do to switch these roles, get into this strategy?

Terry:

I think the first thing really, is I think a lot of people think that developing is a lot of money out of pocket. And actually I’m developing some single family houses that have been less money out of pocket for me, less investment than some of the rehabs and flips that I’ve done. And at the end of the day, I’m putting a better product on the market.

So I think that one thing I want let a lot of listeners know, I remember I was speaking to somebody they told me, “Don’t develop unless…” Somebody said, “Don’t develop unless you have a million dollars cash.” And that was complete absurd to me. And then I found out that person didn’t develop, but it is just absurd.

So for me as a developer, one of my deals actually, we bought the land for 25,000. We spent another 25, let’s just concise number, 25 to pre-develop it and all in, that’s $50,000. We just got the plans approved. That is all that I needed for my construction loan.

Now my construction loan comes in and we’re able to build the whole house. And now I get to build the whole house. And now the choice is mine of what I want to do after if I want to refinance it and keep it or if I want to sell it.

Does it happen all the time like this? Maybe, it can, but my initial investment was about close to $50,000 just for one development deal.

Tony:

Terry, can we talk about the debt that you’re using? You said construction loan, what is that? What are the terms? How are you only able to allow the land costs in your pre-development costs to be all you have to put in, walk through the terms of that debt?

Terry:

So, I work with a couple construction lenders, but I found a new construction lender that works at 60% loan to value. So what they’re going to do is once you get your plans approved, then they can come in and the way that they come in at 60% loan to value, is that they’ll take your plans or your renderings of what the house is going to look like when it’s all said and done, and you will pay for a local appraiser to appraise those plans as if the home was built today.

So when they do that, so one of my homes for example, got appraised for a million dollars and at a million dollars the lender’s able to give me 60% loan to value. So they’re able to fund me $600,000. The contractor bidded the home to be built for 500K. So now what I’m allowed to do that, what I’m also allowed is I’m allowed to put the fees of the loan in the loan as well. And on top of that, the interest, obviously the interest will probably be six to eight months.

I also prepay those interests inside the loan as well. So now my initial investment is just the land and the pre-development costs, and if we build it on time, we don’t have to expect to being incurring other months of interest. And personally, I like the 60% loan to value because it gives me two options.

It gives me an option to refinance at 70 or 75% LTV. Now, I know I can pay the first back and then I get a little bit of money, cash out, refinance for myself. And then option number two is to sell it. And I always want to have two options when I’m doing development deals because I don’t want to bank on a sale, especially with high interest rates while I’m paying on these construction loans, things can get out of whack. So I just like to have two options to know I’m safe in these deals.

Ashley:

Terry, how many have you kept and how many have you sold?

Terry:

I’m keeping all of them. I plan on keeping all of them, and I like the strategy. I like the strategy to keep it because it also, a lot of times when you have to sell, you put it at a price where you have to sell it for. When I hold these properties with an intent to keep them, some of them I just throw on the market. I’m like, “Hey, if it goes at this price, it goes, if not, it’s the Airbnb and it’s still going to be cash flow for me.”

Ashley:

Do you want to walk us through the numbers on one of your deals and your experience of it? Doing a new development? Okay. Yeah. You got a deal in mind?

Terry:

Yeah. Similar to the one I did, but I’ll be more precise on the numbers.

Ashley:

Yeah. Yeah. We want to hear the numbers’ breakdown.

Terry:

Okay. Actually I want to show this. I want to really, really go deep into it with how I was able to develop this with no money out of pocket for me.

Ashley:

Okay. Yeah. Cool.

Terry:

So I found a deal, I got a deal under contract. I wanted to wholesale this deal for $22,000.

Tony:

A land deal.

Terry:

Land deal, correct. I blasted it out, I blasted out and I thought it was such a good deal. I blasted out. It was such a good deal. These two investors, never met them before. They were like, “Hey, come show us the land.” And usually I virtually wholesale land so I just like, “I don’t need to go out there.” But they were really adamant like, “Hey, show us the land.”

So I drive out there, I show them the land and I was looking to make, on this one, I was looking to make about 15, $20,000 assignment fee from wholesaling it. So they come out, they check out the land and they’re like, “Ah, what do you think you can do with this land?” I’m like, “Ah, this is a really good lot. I think you can get a nice single family home here. You can put it on Airbnb. If it’s a three bedroom with a pool, you can do upwards of high hundred thousands a year.” And they’re like, “What? You could do all that?” I said, “Yeah, for sure.”

And then I started showing them numbers of my Airbnbs performing and then I started showing them, what I was looking to CALCAP on my new constructions. And they, at first they didn’t want the deal, so they were like, “Huh?” They were like, “You know what? How about this? What do you have the property for under contract?” And I was just completely open. I said, “I have it under contract for $22,000.” They said, “How about this? We buy it at the price that you have it under contract for, but we bring you in as an equal partner and you run the show, you bring in the construction loans, you run the Airbnb and you’re an equal partner.” And I’m like, “Man, I don’t got the capital right now. This is everything I wanted.” There was a no-brainer for me, no-brainer, no-brainer for me.

Although, I haven’t really met these guys for a long time. The partnership just worked out so perfect and I was so grateful for it. So we go, we buy the land for $22,000. We spend about $25,000 for plans, permits. Plans and permits and all the pre-development fees. And we’re all in about 47. So you can say, let’s just say 50 for these numbers. And we bring in the construction lender. The construction lender comes in, and our property appraises for 1.05 million, so $1,050,000 and they give us the construction loan for 660.

So we had so much extra cushion in there. We packaged six months of construction loan interest in there. So really that’s all we’ve invested so far in the project. Can we go a little bit, can we splurge and probably do a little extra stuff here and there maybe and come out and be a little bit more money out of pocket? Yeah, we could, but that’s just the power shift of understanding how to use debt and understanding how to work with partners and to bring value to other people.

And these were older gentlemen, so a lot of the older generation, they don’t really understand the Airbnb game and they don’t understand short-term rentals. So it’s like a lot of us, like the newbies, rookies in this game, this is what we understand and this is real value that we can bring to other people. And for me it’s a deal that I’m $0 out of pocket for. So it’s a win-win in my opinion.

Ashley:

And that’s a super great point at the end that they put on the older generation as to, they didn’t have BiggerPockets when they were just starting out. They started building, they were just doing real estate investing and now that there’s BiggerPockets and you can reach out to people and find out all these different things that are going on, especially if they’re not on social media either, then it’s a lot harder to learn about all these different things that you can actually do with real estate investing.

So I think that is a huge advantage of knowing of all these new creative strategies that come out. Even midterm rentals, 30-day stays for traveling nurses, how that has exploded in the last couple years too. And that’s something someone may not have even have heard of or thought of that you could do. Or there’s somebody that has been doing that forever and they don’t know that you can put it on Airbnb. They’ve always just rented it to somebody else and all these things. But I think that’s definitely an advantage.

And Tony even and I have been talking about that a lot as to how not just the capital that you’re bringing to the table is the biggest benefit. There are so many other things you can bring as a rookie investor and knowledge is one of those for sure.

Tony:

And the only other thing I’ll add to that is that, I think that there’s, it just goes to show that a reinforce our point earlier about when you can provide value to people, they’re more willing to give you value in return. You bought these guys not only an amazing deal, but you brought them a skillset that they didn’t have. And that’s a big part of any successful partnership is that there has to be puzzle pieces that fit.

The second thing, Terry, was that you kind of had the courage, I guess, to partner with people that you didn’t know all that well. And I think sometimes people have this hesitation around, “Okay, I just met this person. Is this the right person to work with?”

Honestly, typically Ash and I would probably say like, “Maybe date them a little bit first.” But if you get a good vibe from them and it all works out, it just goes to show what happens when you kind of take that leap of faith. So just kudos to you man, for what turned out to be a really, really awesome deal. I guess last question on that piece, do you plan to continue working with them?

Terry:

Yeah. It’s actually a great partnership. It’s just like, “Look, we’re retiring, we’re trying to lay by the beach. You handle it.” And they come in obviously, and they put their input in here and there, but it’s one of those good partnerships where they see value in what I bring to the table from bringing in the construction financing to bringing in the Airbnb knowledge, all the data analytics that I put together for them. So they see a lot of value and a lot of upside to it. And I definitely see myself work with them.

Ashley:

Yeah. What a huge advantage, especially if somebody who’s looking to retire, they don’t want to go and take the time to learn and do research on everything you need to know to do this, when you can just partner with someone.

And I think a lot of people that have already become successful in one thing, that’s their next step is they go and partner with other people in other things that are successful at what they’re doing. So they don’t have to go and become an expert at a whole different business. So I think that definitely adds a lot of value.

So one last point I want to touch on here is what environment did you need to succeed? And do you think there were transferable skills that you gained from wholesaling?

Terry:

Mm-hmm. I think the environment in developing, there’s always obstacles. There’s always little hiccups here and there. It’s just part of the game and it’s really part of it. And just like wholesaling, there would be obstacles, things, but you’re constantly problem solving. You’re really constantly problem solving.

And I think I made sure I kept the circle of developers and if they needed value about the market or anything, I was always super adamant, I was going to give it to them, just be on the phone talking to them. But at the same time I knew that, “Hey, this is my first one. I need a little help here. Do you mind checking it out for me or going by?” And I made some really good friends from it.

And I remember one of my buddies, he’s a GC, he would just come by and check on the project, because he had some projects nearby and some days I’d be like, “Oh my gosh, these guys are doing this wrong. The inspector’s not passing this. What’s the deal?” And he’s like, “Brother, relax. It is developing. It’s supposed to be fun.” And sometimes it’s just in life in general about anything that we’re doing, it’s like, “Yeah, you’re right. Just have some fun. We’re developing. It’s fun.”

So I think being able to just do that is probably one of the most important skillset that you can have. And I would say developer, just anything, just to enjoy it. So that’s the skillset I’m working on the most of this day. It’s, once you get past that learning curve, you can really just say, “All right, cool. Now this is fun.” So that’s what I’m kind of veering to, but.

Tony:

Just one comment on that piece. I think it’s a super important point because it is easy to get overwhelmed. But I was reading some book recently, I can’t remember which book it was, but it was talking about how the version of you 10 years ago would probably be excited to deal with the stress that you’re dealing with today.

Because it’s, think about the ways you had to grow and evolve as a person to even be in a position to deal with that kind of stress. And when you can kind of frame it that way where, “Hey, the things that are kind of on my plate today are a result of the progress and growth that I’ve had as a person, as an entrepreneur, as a real estate investor.” It kind of reframes a situation. So yeah, man. Just a thought that came to mind.

Terry, dude, so much good conversation, but I’m so glad that we were able to get you back on the show. Before we let you go we got a couple more segments here.

All right, so Terry, our question today comes from Voltaire Gannet and Voltaire says, “Can you 1031 exchange into new construction homes?” So have you ever had any experience doing a 1031 exchange? And if so, do you know if you’re able to do that with new construction? I

Terry:

I keep most of my properties to be honest. So I haven’t had that experience yet. But I do hear that with 1031s, Tony, you would know probably better, but you have to kind of 1030 worth up into a property that’s worth more. Correct?

Tony:

Yeah. To an extent, right? So I’ve done one 1031. Ash, have you done any 1031s yet, also?

Ashley:

Not for myself, but for another investor, I did.

Tony:

Yeah. So there’s some limitations on what you can do. It has to be a kind exchange. So I couldn’t sell my single family home and go buy a car wash. So it has to be a single family home for another type of real estate. And I’m not a 1031 exchange expert either, but you can’t necessarily go, there are limitations on the value of what you’re selling versus what you’re actually acquiring.

I think based on what I’m looking at here, I think you should be able to 1031 into new construction as long as you’re able to check those boxes of kind exchange. So the biggest thing Voltaire is that, if you are thinking about doing a 1031, you need to use a qualified intermediary. So you can’t just go out there and sell your property and then tell the IRS, “Hey, I didn’t touch it, it’s just sitting in my savings account.” You have to hire a qualified intermediary to hold those funds for you, and there’s a bunch of paperwork they fill out to make sure that you executed the right way.

So if you’re thinking about doing a 1031, Voltaire, my first piece of advice would be go find a 1031 exchange intermediary who can help you facilitate that process.

Ashley:

Yeah. One 1031 exchange I did with another investor, I helped him with is he sold, I think it was a 20-unit apartment complex, and he ended up buying two commercial buildings and a vacant piece of land. And then he actually ended up keeping, I think $50,000 in cash that he ended up paying tax on that.

So he didn’t even 1031 exchange the whole amount. He did keep some of that, and that was just because he couldn’t find anything else and he was hitting his deadlines. But he ended up getting those, which a 20-unit apartment complex, which is a residential commercial property to two other commercial properties that were retail stores and then also vacant land.

So I mean, those weren’t exactly the same type of property, but they still fit into that model of kind exchange.

Tony:

I’ve also heard, and actually this is from a mutual fund of ours, Ashley Taro, but he told me about a reverse 1031 exchange where you can, there’s a way to do it backwards. So if you’ve already sold and bought the new property, there is a way to kind of go backwards and retroactively apply at 1031 as well, which I didn’t know about. But anyway, Voltaire, go talk to a professional. Ash and I are just podcast host, who knows if you can trust us.

Anyway, moving on to the next piece. It’s the rookie exam. So the three questions we ask every single guest. Terry, are you ready for question number one?

Terry:

Yes. Ready.

Tony:

All right. Now that you’re a developer, what’s one tool, software app or system that you use in your business?

Terry:

As a developer? I still use PropStream a lot. I still use PropStream. I like to look at the satellite images of all the properties. I like to know the comps. I want to know what new developments are selling for. I’m always constantly looking at what new developments are trading at or what’s going on. So definitely still PropStream, still PropStream.

Ashley:

What is one actionable thing that rookies should do after listening to this episode?

Terry:

I would connect with developers. I would connect with developers in your local market that you’re looking to develop in, and I would just talk to them and say, “Hey.” Whether it be starting to wholesale or, “Hey, is there any way that I can find you some land or anything? I have a marketing vehicle that gets me great off market listings and deals. So you guys are looking for anything?”

And then reel them in a little bit and then say, “What are you working on now?” See what they’re doing, and so now you’re able to start building that developer’s eye yourself. So that’s what I would definitely say. Just start connecting with them.

Tony:

All right. And question number three, Terry, where do you plan on being five years from now?

Terry:

Five years from now, I want to be building skyscrapers in New York City.

Tony:

Dang. I love that. That’s a good one, man.

Terry:

Yeah. Five years. I need my first skyscraper in the city. Yeah.

Tony:

Harris Tower.

Terry:

That’s a good name. We’ll go back to this podcast in five years and see that.

Ashley:

Well, it’s not quite five years ago, but a couple years ago. You can go back and listen to Terry’s episode on biggerpockets.com/rookie153. And I don’t think we had this segment then, but it’d be interesting to know how, if we did, what you’d be on track for that five years. So we’ll definitely have to have you back in five years to talk about that skyscraper development.

Terry, where can everyone reach out to you and find out some more information?

Terry:

I think the most responsive on Instagram. Instagram is terryharris15. I kind of did a little pause on Instagram, because I was learning a lot of developing and in the ground, but I’m starting going to get back on YouTube and putting more content out there as well.

So YouTube page is TCash, T-C-A-S-H, and those are the two, I, where on the YouTube page, I teach a lot about wholesaling, really go in depth of every software and everything I use in wholesaling. So if anyone wants to get into wholesaling, I think that’s a good little, check that out. And then Instagram if you want to reach out and just ask questions on developing in general, I’m there for that.

Ashley:

And for today’s social media, shout-out. I want to give a shout-out on Instagram to account I found, and this one is ladygina_real_estate_investing. And here we have Lady Gina shares her investment journey. She is a full-time real estate investor and she specializes in apartment buildings. So go give her a follow and see her story.

I love that we do these social media shares because sometimes it’s people that we see that are sharing value, they’re sharing their tips, and then other times it’s just literally telling you what they’re doing day-to-day or as what they’re doing as an investor. And I think both of those aspects are so valuable to keep you motivated, keep you inspired. So clear your feed of meme accounts and start following more real estate investors.

I’ll tell you a funny story real quick. So our partnership book came out, Real Estate Partnerships, and my mom was telling her friends about it. My mom was telling her friends about it, and she texted me and she’s like, “Oh my God, so-and-so was freaking out that you co-authored a book with Tony.” Blah, blah, blah. And I knew right away. I knew because I was like, “There’s no way my mom knows. My mom’s friend knows who Tony is. There’s no way.”

And so I was just like, “Oh yeah, how?” And she’s like, “Oh, she’s read his books, listens to his podcast, all this stuff.” I’m like, “Does she mean Tony Robbins?” And she’s like, “No, no, no. I’m sure I said Tony Robinson.” And I was like, “Okay, well Tony’s podcast is my podcast. So she listened to my podcast?” And she’s like, “Oh yeah, it was Tony Robbins.” She thought, but her friend was ecstatic. “Oh my God! Ashley’s associated with Tony Robbins? That’s amazing!”

Tony:

Add another name to the disappointment.

Ashley:

Yeah. Maybe it will sell more books because people will keep making that confusion. Maybe we should have left the J off the book title. A slight blur off the ending there.

Tony:

That’s funny. Yeah, I should lean into that more often. That’s true.

Ashley:

Thank you so much for joining us on the Real Estate Rookie Podcast. I’m Ashley, @wealthfromrentals, and he’s Tony J. Robinson, @tonyjrobinson on Instagram. And we will be back on Saturday with a Rookie Reply.

Help us reach new listeners on iTunes by leaving us a rating and review! It takes just 30 seconds and instructions can be found here. Thanks! We really appreciate it!

:215-447-7209

:215-447-7209 : deals(at)frankbuysphilly.com

: deals(at)frankbuysphilly.com

Realtor.com tool shows what your home could get on Airbnb

Homeowners can now see potential short-term rental income estimates on Realtor.com thanks to an integration with Airbnb.

Short-term rental earnings estimates for hosting one room or the entire house will be available to homeowners via Realtor.com’s My Home dashboard, according to an announcement on Thursday.

The estimated earnings for a seven-day rental are based on Airbnb data from similar listings in the ZIP code.

A recent survey from Realtor.com and CensusWide found that 39% of homeowners have or would consider renting out part of their primary home, with 23% having rented out their home previously or are planning on doing so in the future and 16% reporting that they are considering renting out part or some of their home in the future.

Financial reasons are the primary motivator for homeowners to rent out their home, as 34% who have rented or plan to rent out their home are doing so in order to save money for a home purchase with a higher mortgage rate, while 29% are doing it prepare for potential upswings in a variable mortgage and 21% are doing it to help pay their current mortgage.

According to Realtor.com, the integration will also enable homeowners to see if it is a good idea to rent out their current home as an alternative to selling it. Of the homeowners surveyed, 60% reported they would consider renting out their current home rather than selling, if they look to buy or rent elsewhere, with 21% citing extra income from a renter and 19% citing the ability to maintain the home equity they have built as primary motivators.

“Short-term rentals are a great way to help with some of the costs of homeownership – renting out their house for a couple days or weeks out of the year when it’s not in use could generate extra income that can be put toward the mortgage, maintenance, or even help cover the cost of a vacation,” Mausam Bhatt, the chief product officer of Realtor.com, said in a statement. “By arming homeowners with information about how much they could potentially make by renting a room or their whole home on Airbnb, Realtor.com is helping them better understand their options and in turn make more informed decisions about their home.”

Realtor.com’s integration with Airbnb comes as many metro areas are looking to crackdown on short term rentals. Earlier this month, thousands of New York City Airbnb listings vanished from the market as the city introduces some of the strictest regulations in the U.S. for short-term rentals. City councils in Dallas, Philadelphia and New Orleans have passed their own restrictions on short-term rentals.

Source link

Affordability slows home sales, hints at future home price declines

Mortgage rates peaked at 7.5% a couple weeks ago and are staying stubbornly high. Rising mortgage rates mean rising inventory as home buyer demand slows quickly. But home prices are staying pretty stable even though we can measure a slowdown in the number of homes getting offers.

Most years, available inventory of unsold homes on the market peaks in August. This year inventory is still climbing. Last year at this time, mortgage rates began to spike dramatically from under 6% to 7.5% in a few weeks. This caused inventory to rise dramatically late into October. The change in rates this year isn’t as dramatic as the change last year, so the change in inventory isn’t as dramatic either. Last year, the change in mortgage rates was rapid enough to drive home sales prices down.

There’s no getting around the fact that sales are slow, demand is held back because the cost of money is so much higher than it has been recently. It’s notable that home sales prices are not yet declining rapidly like they did last fall. But there are some new hints of weakness in future home sales prices.

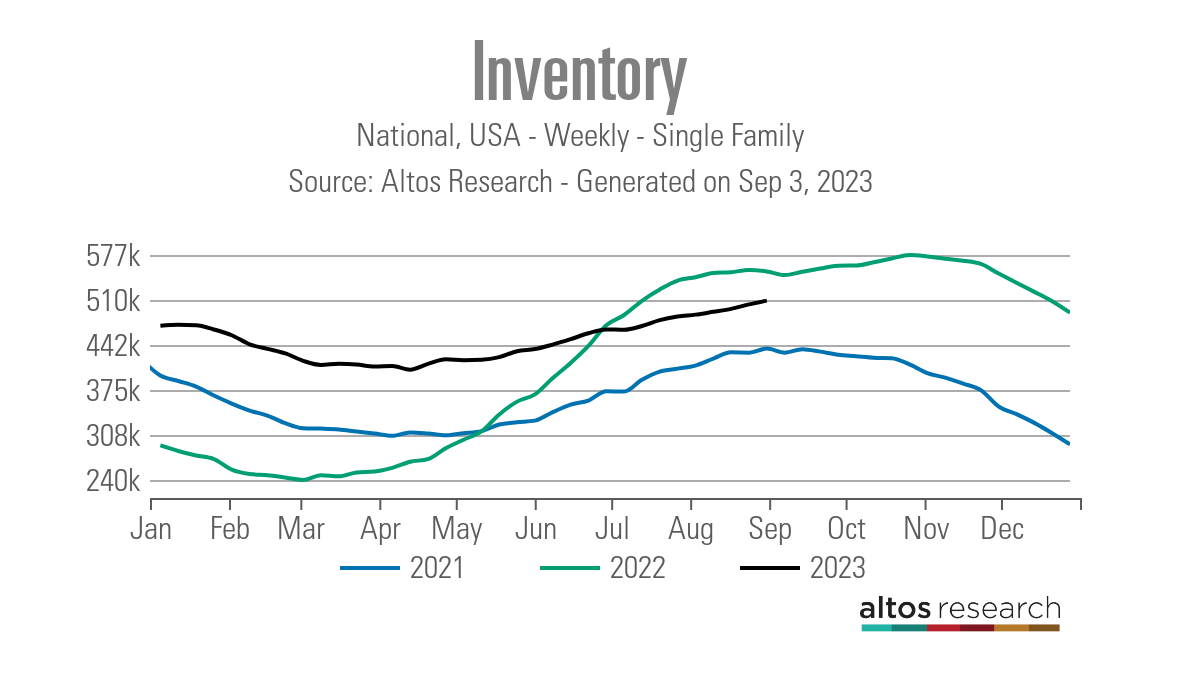

Available inventory rose

Available inventory of unsold single family homes rose more than 1% again this week to 509,000 homes. Supply of homes on the market does not appear to have reached the peak for 2023. Last year at this time, inventory appeared to have already peaked, but the number of homes on the market jumped again along with mortgage rates later in September.

In this chart (above) you can see the comparison. The dark red line is on a steady climb each week. That’s this year. Mortgage rates have been rising, making homes more expensive to buyers and obviously slowing demand. Less demand means fewer purchases and inventory builds. There are 8% fewer homes on the market now than last year at this time. My guess is that later in September, mortgage rates ease down — maybe even under 7% — and inventory starts declining for the end of the year. Contrast that to last year, the light red line, when inventory kept climbing until rates finally peaked in November 2022.

In this chart (above) each line is a year’s curve of available inventory of unsold homes. Notice how each year inventory generally peaks in August. This is an effective illustration of the impact this year’s higher mortgage rates are having on home buyer demand. Inventory could still keep building for two more months if mortgage rates jump again.

There are only 358,000 single family homes in contract pending now. That’s 11% fewer than last year. The rate of sales picked up a bit last week before the Labor Day holiday. Though home sales are still running 7-10% lower than last year. This moment last year was right at the cusp of a dramatic slowdown both in prices and in purchase volume.

It could be that we finish September with home sales at a faster pace than last year. However, I’ve been looking for that change for several months and it’s been elusive. For a while this year it seemed like home sales would finish 2023 with more than 2022, and that hasn’t materialized.

We saw 64,000 newly pending contracts last week for single family home sales which is 7% fewer than last year. This week is a holiday week so new sales will tick down win next week’s data. So we have 11% fewer total contracts but only 7% fewer new contracts. Just slightly closing the gap from last year.

In the chart above, each bar is the total number of home sales in contract. The taller the bar the more sales are in process in a given week. The light portion of the bar are the new contracts that week. Last year the sales rate slowed dramatically after mid September. See how the light portion of the bar shrinks each week. This week the slowdown is much more gradual, much more like normal seasonality.

Price cuts climb

Meanwhile this autumn’s slowing home buyer demand is showing up in price reductions too. The percent of the homes on the market that have taken a price cut climbed again this week to 36.2%. You can see how we now have more price reductions than any recent year except last year at this time.

Think about price reductions as a leading indicator of future home sales prices. Tracking price reductions now is an excellent indicator or the organic levels of demand in the market. We can really see how buyer demand is sensitive to the rise over 7% mortgage interest. A home on the market now, doesn’t get offers, does a price reduction in September, gets an offer in October, which closes in November or December. We can see now the sales prices weakening several months in the future. This trend could change like it did the the first half of this year when rates were falling.

Consumers seem to react to changes in mortgage rates more specifically than to the absolute levels. When mortgage rates went from 7 to 7.5% last month, that’s why we have more inventory and more price cuts right now. When rates jump, fewer buyers make offers and therefore more sellers take a price cut to stimulate demand. That’s what we’re seeing now.

Last year, almost 40% of the homes had taken a price cut and that was showing us greater weakness in sales prices than we see now.

Home prices slightly ahead of last year at this time

In fact, home prices are running just slightly above last year at this time. The median price of single family homes in the US is $448,000 this week. Last year, homes were priced at $440,000 and adjusting down very quickly in the second half of the year. We saw that in the last slide with price reductions too.

The median price of the newly listed homes is $395,000 now. The price of the newly listed cohort each week is also a leading indicator of future sales prices. Each week, sellers and listing agents have to price the new listings at a price point where they’ll sell. Last year when demand was dropping so quickly, so was the price of the new listings. That’s the light red line here. At the far right end of the light red line you can see that home prices are ticking down as happens in the third quarter each year, but prices are not falling as quickly as they did last year.

The median price of the homes in contract is $379,900. That’s unchanged from last week and about 1% higher than last year at this time. Over the last few weeks, homes prices have been ticking down. This is what you’d expect for late summer. Even though we can see the rate of transactions slowing and we can see the percent of homes with price reductions ticking up, the price of those getting offers isn’t not dropping dramatically like it did at several points last year. This illustrates my point that home buyers are more sensitive to the changes in rats than they are to the absolute levels of rates.

This year, at the far right end of the chart, the dark red line you can see that home sales prices peaked a couple months ago just before mortgage rates started climbing for the summer. See the gradual decline in the dark red line now. The median price of the homes newly in contract is $370,000. That’s basically unchanged from last week and from last year at this time.

Obviously, home buyers are sensitive to affordability, they’re also sensitive to weekly changes in affordability. Last year, the changes in mortgage interest rates were huge. In a few short weeks mortgage interest went from under 6% to 7.5%. That translated into a big drop in the median price of the newly contracted sales. Buyers that still chose to buy would only do so at significantly lower home price points. You can seem that drop in the middle of this chart. This year’s mortgage rates increase has been much more gradual and the subsequent price decline is much more gradual.

Home sales are in the contract stage for 30-45 days commonly so each week where the new sales prices tick down that adds up to the over all market in a few weeks.

There is so much signal in the active market that looking at the lagging closed sales prices don’t tell you.

Mike Simonsen is founder and president of Altos Research.

Source link

Risk and compliance expert Jeffrey Flory is QC Ally’s new CEO

Loan quality and audit services company QC Ally has appointed Jeffrey Flory as its new chief executive officer, the company said Thursday.

The news comes eight months after the appointment of Nicole Booth as as company CEO. She left in August.

“I am humbled to take on this role and help bring the company’s vision to fruition,” Flory said in a statement. “QC Ally is invested in providing high-quality outcomes in both the service and the proprietary technology it offers to clients. The combination of flexibility and world-class service are a legacy I look forward to expanding on in the years to come.”

Prior to QC Ally, Flory held several leadership positions in the risk and compliance segment. He was SVP of “Risk and Compliance Solutions” at Interthinx/First American, and then became a partner in the mortgage advisory practice at Baker Tilly. Overall, he brings 30 years of mortgage lending and servicing experience to the company.

“Since investing in QC Ally last year, we have been entirely focused on enhancing the Company’s offerings through continued investment in innovation and strategic M&A,” Adam Doctoroff, a partner at Narrow Gauge Capital, said in a statement. “We welcome Jeff to our management team and believe that his industry contacts and knowledge make him perfectly suited to spearhead those efforts.”

Earlier this year, QC Ally named Melissa Peregord as the company’s new chief growth officer. Its president and COO Donna Gibson was named a 2022 HousingWire Vanguard.

Source link

Ishbia urges FHFA to step in on GSE loan buyback issue

Mat Ishbia, president and CEO of United Wholesale Mortgage, has echoed the frustration of mortgage industry experts and leaders with the increased volume of loan buybacks from the government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac.

In a recorded video distributed on Tuesday, Ishbia claimed the Federal Housing Finance Agency (FHFA), which oversees the GSEs, “is going to have to step in again because it’s becoming a big issue.”

FHFA did not immediately respond to a request for comments.

According to Ishbia, the FHFA years ago took action so Freddie Mac and Fannie Mae would not push back loans for “illogical reasons, small reasons left and right or after a 36-month window.” However, it doesn’t seem to be working, Ishbia said.

“They are making billions, and lenders are barely scraping by, but they continue to make them buy back loans for small reasons here, little things that happened on a loan that maybe are not impacting the borrower’s success in that loan,” Ishbia said.

At the end of August, HousingWire reported on a new report by mergers-and-acquisitions consulting firm Sterling Point Advisors showing that loan-repurchase rates have been on the rise in recent quarters when many IMBs are struggling to stay in business.

In 2020, Fannie Mae reported $1.1 billion in repurchases on $1.4 trillion of single-family loan-acquisition volume (loans originated by lenders and purchased by Fannie Mae), or an eight basis-point repurchase rate. In Q1 2023, the GSE had $459 million in repurchases on about $68 billion in loan-acquisition volume or a 68 basis-point repurchase rate, the report shows.

“The industry is up in arms and is very frustrated with the amount of repurchases Fannie Mae and particularly Freddie Mac are pushing back on lenders,” Ishbia said. “A lot of trade groups, a lot of people are talking about it, and it’s impacting lenders, impacting mortgage people, and impacting consumers at the end of the day as well.”

The GSEs showed a different approach to buybacks in May during the Mortgage Bankers Association (MBA) Secondary and Capital Markets Conference and Expo in New York. Fannie Mae’s position was that the loan-repurchase increases are an economic problem, not an underwriting process issue. Meanwhile, Freddie Mac said it’s in talks with lenders to address the problem through a more customer-focused approach.

Amid mounting concerns that loan-repurchase rates in upcoming quarters are likely to continue to trend upward, Freddie Mac told HousingWire last week that, “We’re seeing a positive trend in loan quality and materially fewer repurchase letters as a result of the progress we’ve made by working collaboratively with our industry partners in the past year. We will continue to look for opportunities to build on this progress.”

Freddie Mac also said they are “always looking for ways to improve our quality control processes, and we will continue to engage in open and productive dialogue with lenders to find ways to further improve loan quality while fostering sustainable homeownership.”

Source link

Opinion: Real estate agents can flourish in an AI-flooded market

Generative artificial intellegence, such as ChatGPT, is changing everything—a statement that comes as little surprise to anyone these days, and least of all to the many real estate agents whose markets are being saturated by artificial intelligence (AI)-empowered buyers. With the advent of proptech services entering the real estate industry, buyers are becoming more thoroughly informed every day, long before they even speak to an agent.

Here is just one example among many: Proportunity helps would-be property owners to get a fair and up-to-date valuation of residential real estate. Their model gathers property data, real estate market data, crime rates, and similar inputs to provide automated property evaluation.

To fear that redundancy lies on the horizon is only natural in light of such dramatic change. But, fortunately, those fears are misplaced. The world yet has much use for real estate agents, and indeed the advent of realty-focused AI presents more opportunities than threats for those who are willing to change with the times. Below are detailed three ways to do exactly that.

1. Keep Up

AI is making buyers smarter. That means that agents need to become smarter, too. Agents should be continually furthering their education and research to ensure that their expertise remains relevant and, ultimately, invaluable to buyers. This translates to consistently being the first authority on the local market, and keeping a careful pulse on its fluctuations and trends. An understanding of the information that will be available to buyers before enlisting an agent’s services is also vital here, as it offers insight into the areas in which agents can contribute the most value.

Agents must not fall behind the very same technological advancements that buyers are using to their advantage. Just as AI empowers the buyer, it can be a game-changing instrument for agents who are apt enough to use it. Agents should therefore follow suit and maintain a watchful eye over developing technologies, being quick to spot new AI-assisted tools that could help maintain their usefulness to buyers and keep them one step ahead of the competition.

2. Think of Buyers—and AI—as Teammates

It is useful to think of the agent and buyer as members of a team with a common goal. The agent provides leadership and expertise, while the buyer—the final authority on what he or she actually wants—provides direction. Either party relies on the other to succeed, and what benefits one party benefits the other; they are a team, that is. So when buyers are empowered by an AI that assists in elucidating what exactly they are looking for, it works in favor of the agent by progressing the team toward a more efficient resolution. For instance, HomeByte, an AI assistant designed for the home-buying journey, not only makes it easy to pinpoint the exact homes you’re interested in buying, but it also helps you decide if you’ll like your new neighborhood.

That makes AI a part of the team as well, and it ought to be embraced as such. Instead of waiting for the buyer to bring new tools to the table, agents should proactively seek out technologies that will make the process easier and faster for the buyer—and, by extension, for the agent as well.

3. Realize Your Value

What, then, if it becomes too easy for the buyer? Will it become so easy that they no longer require the services of a real estate agent? The agent still has a unique place within the team; they need merely to realize the value they offer, and then aim to fill that role as well as possible.

Good agents are still the most experienced, relevant source of information for any buyer. While most AIs are necessarily trained on historical data, the agent is constantly immersed in their present market and has been for years. Agents are therefore far better equipped to make real-time judgments and offer expertise tailored to the precise time and place. Even the best AI tools are only just that, and most buyers who are serious about making wise investments are willing to bypass the cheap alternative of doing it all themselves for the assurance of an expert who is more than likely to save them money in the long run.

Whenever the market takes a drastic turn it is easy to assume the worst. And, to be fair, change never does come without risk. But for those who are willing to grow with the business, risk is always accompanied by opportunity. It is plain to see that artificial intelligence is altering the face of real estate, and will continue to do so into the future.

Curtis Williams is a land investment professional with National Land Realty.

This column does not necessarily reflect the opinion of HousingWire’s editorial department and its owners.

To contact the author of this story:

Curtis Williams at ethan@razorsharppr.com

To contact the editor responsible for this story:

Tracey Velt at tracey@hwmedia.com

Source link

Don’t take borrower credit at face value

If there was a chance that a new loan application was sitting in a corner of your office right now, would you look for it? Of course you would. This is not a market where any lender can afford to lose a prospective mortgage deal — every loan matters. That’s why looking closer at each borrower to gauge their closing potential is so important.

In the past, lenders would underwrite a new loan and expect that the emerging details were pretty much set in stone. The applicant’s capacity to repay was visible in existing assets, bank accounts and payroll records, the appraisal report provides a view into the value of the collateral and the credit report illuminates any risk in the consumer’s credit history.

Capacity, Collateral, Credit. The 3 Cs of lending. We all know them. We’re suggesting you look at the final C, credit, in a new way.